Other recent earnings reviews:

Table of Contents

a. Key Points

- Fastest quarterly revenue growth rate in 5 years.

- Raised annual CapEx guidance by $10 billion.

- Daily user growth was held back by 2 geopolitical items.

- Upgraded Meta AI is performing very well.

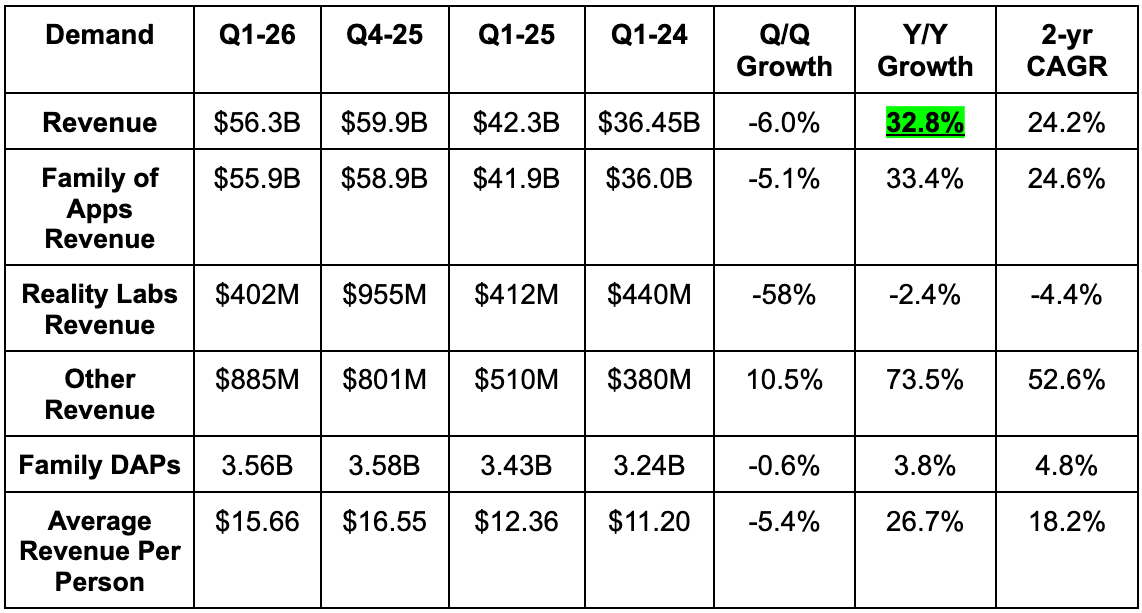

b. Demand

- Beat revenue estimate by 1.4% & beat guide by 2.4%. The 4 point foreign exchange (FX) tailwind was as expected. That was not the source of the beat.

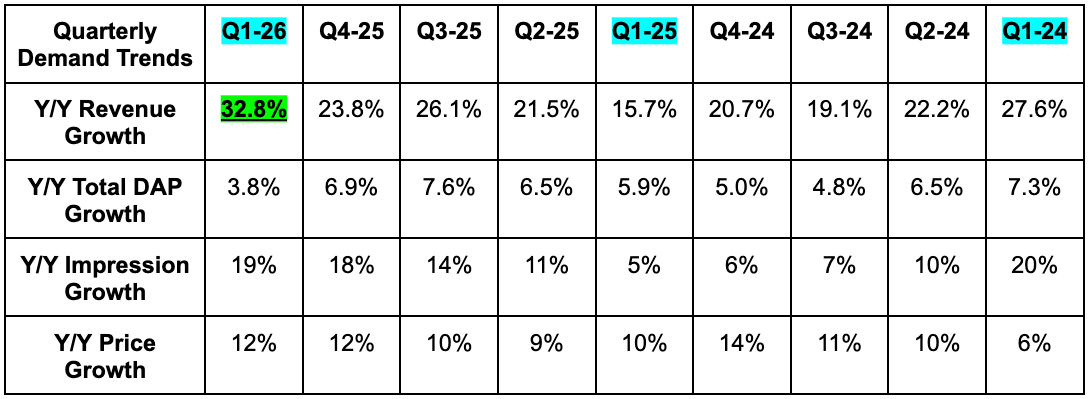

- This was its fastest overall revenue growth rate since the pandemic surge.

- By geography:

- UCAN revenue missed estimates by 4.2%.

- Europe revenue beat estimates by 4%.

- Asia-Pacific revenue missed estimates by 3.6%.

- Rest of World revenue beat estimates by 4.5%.

- By revenue bucket:

- Overall Family of Apps (FOA) revenue beat estimates by 1.7%. Within this, other FOA revenue rose 74% Y/Y due to strong WhatsApp paid messaging and subscriptions like Meta Verified.

- Reality Labs (FRL) revenue missed estimates by 21%.

- Ad impressions rose 19% Y/Y compared to 16% growth expectations. The beat was due to ad load optimization and strong engagement.

- Ad pricing rose 12% Y/Y, which met expectations. This was due to a better macro backdrop vs. last year. This was offset by faster growth in lower revenue per user regions.

- Missed daily active people (DAP) estimate by 1.4%.

The small decline in sequential DAPs and the DAP miss vs. consensus was related to two things: Iran and Russia restricting WhatsApp access. Growth was positive across every app excluding these items while engagement reached new highs.

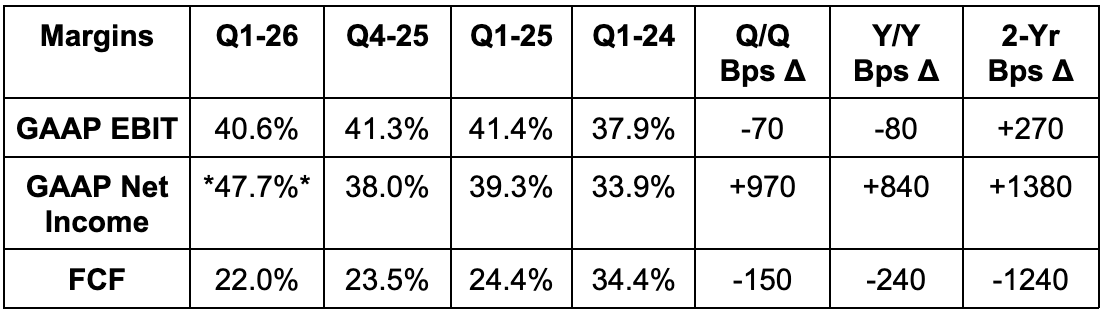

c. Profits

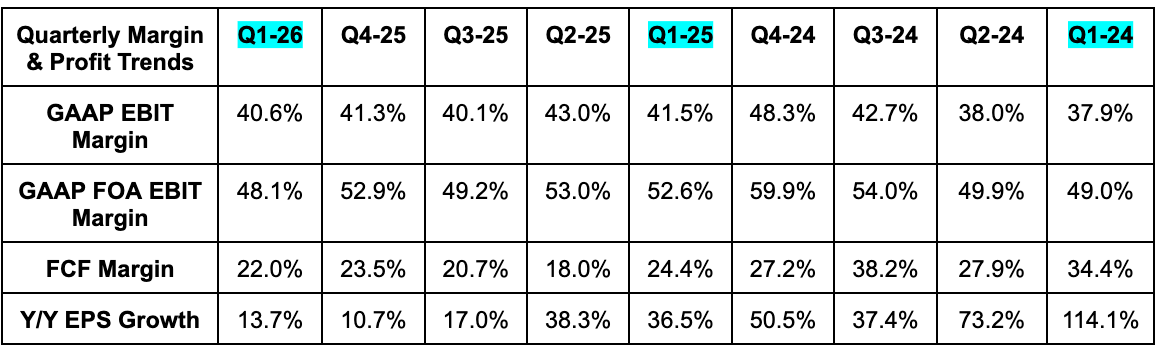

- Beat EBIT estimate by 17.3%.

- OpEx rose by 35% Y/Y mainly due to higher infrastructure-related depreciation and employee compensation.

- Headcount fell by 1% Y/Y (but expensive hiring for the AI team)

- Beat $6.82 GAAP EPS estimate by $0.49 ex-tax benefit. This is despite a -$1.1B equity investment loss during the quarter.

- Sharply beat FCF estimate due to a large tax benefit. For context, its tax rate was -23% due to a $8B benefit related to changing U.S. tax policy.

d. Balance Sheet

SPONSORED

Subscribe below for a review of Meta's balance sheet, guidance, valuation, conference call and earnings presentation, as well as my take on the quarter. Also enjoy access to 40+ other earnings review from this season and so much more.