Click here for a quick SoFi 101 overview and here for my SoFi deep dive.

Other reviews from this season:

Table of Contents

a. Key Points

- The new SoFi Plus program is performing very well.

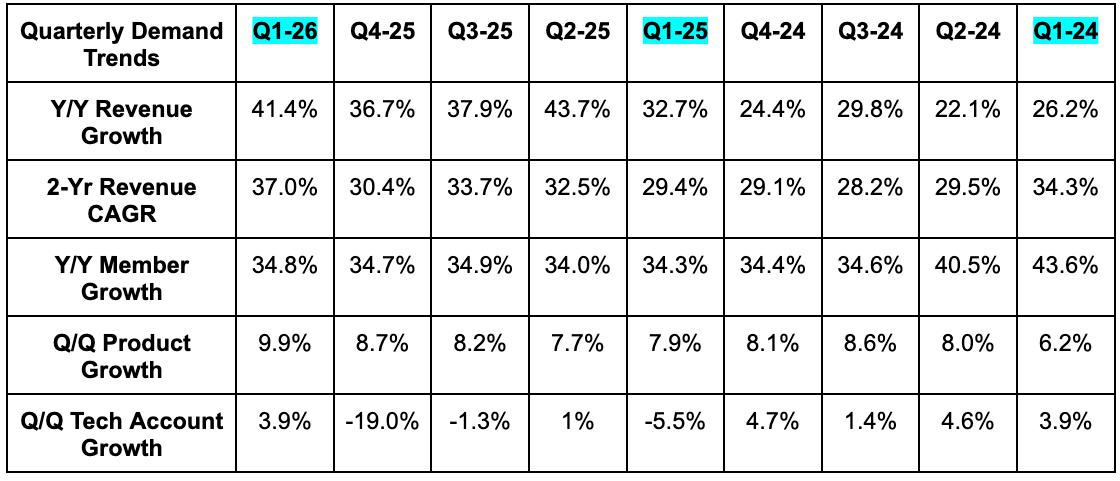

- Chime migration led to sharply negative Y/Y tech platform growth.

- SoFi now expects 0 rate cuts vs. 2 previously.

- Credit health remains strong.

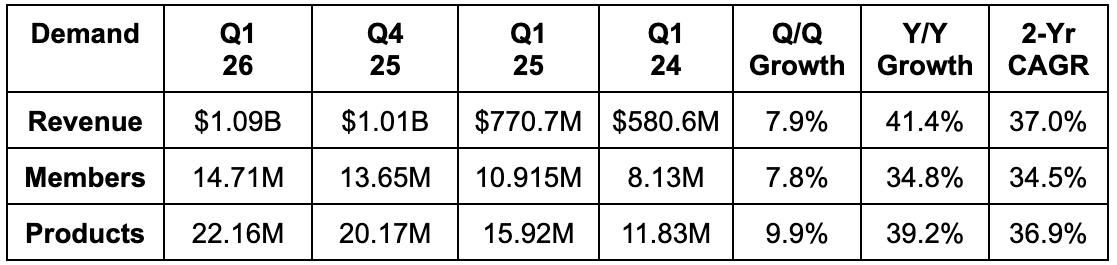

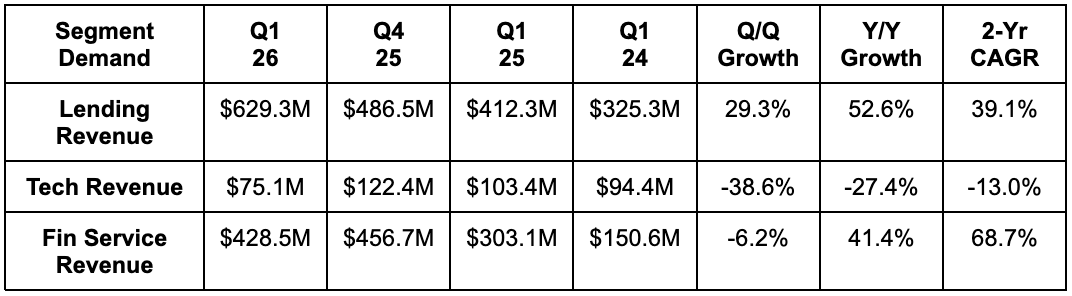

b. Demand

- Beat revenue estimates by 3.5% & beat guidance by 4.5%.

- Lending revenue beat estimates by 22%.

- Financial services revenue missed estimates by 9%.

- Tech platform revenue missed estimates by 27%.

- Beat net interest income estimates by 6.6%.

- Slightly beat non-net interest income estimates.

- Beat member estimates by 2.8%.

- Beat product estimates by 3.2%.

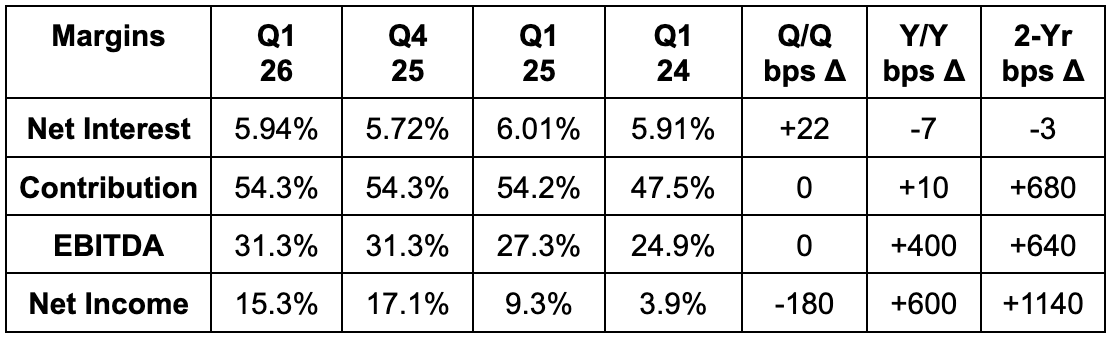

c. Profits & Margins

- Beat EBITDA estimates by 7.6% & beat guidance by 13.3%.

- EBITDA rose by 62% Y/Y.

- Met $0.12 EPS estimates & guidance. EPS would have been $0.13 without negative stock price action during the quarter that diminished expected tax benefits.

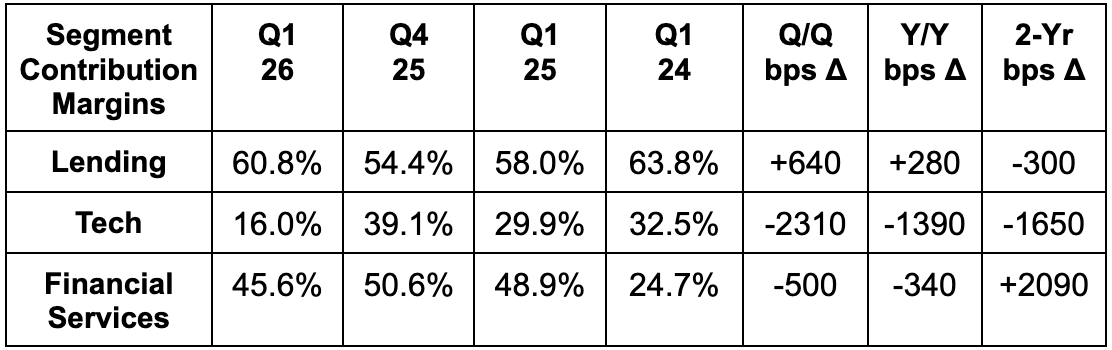

- Beat 56% lending contribution margin estimate by 480 basis points (bps; 1 basis point = 0.01%).

- Missed 51% financial services contribution margin estimate by 540 bps.

- Missed 30% tech platform contribution margin estimate by 1400 bps.

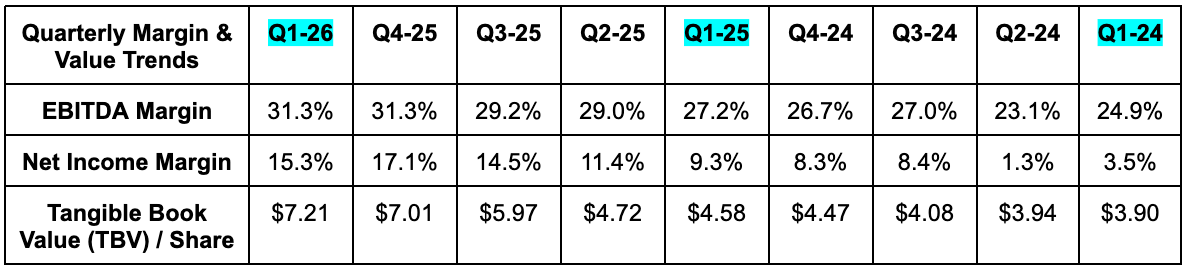

- Tangible Book Value (TBV) growth was aided by capital raises from last year.

d. Balance Sheet, Credit Health & Capital Market Access

Upgrade below for a detailed overview of SoFi's balance sheet, credit health, capital market activity, earnings remarks and my take on the company and investment.