Other reviews to read from this season:

Table of Contents

a. Key Points

- Maven continues to be deployed across more parts of the US government.

- A change in deal classification during the quarter altered segment-level results vs. expectations.

- Rule of 40 Score rose to 145.

- Artificial Intelligence Platform (AIP) can't meet all of its currently elevated demand.

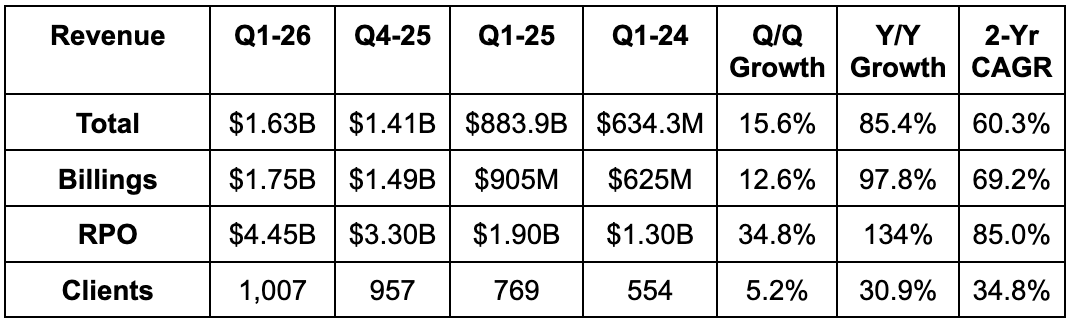

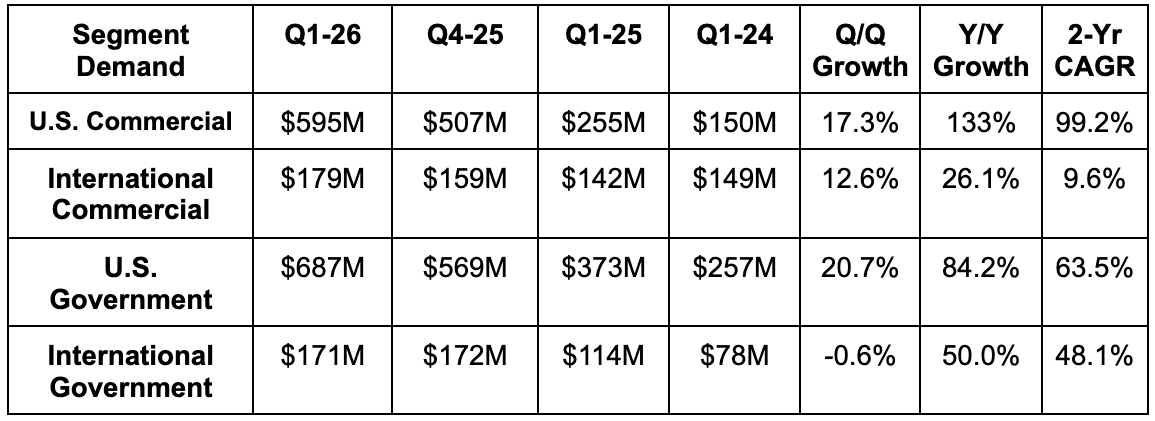

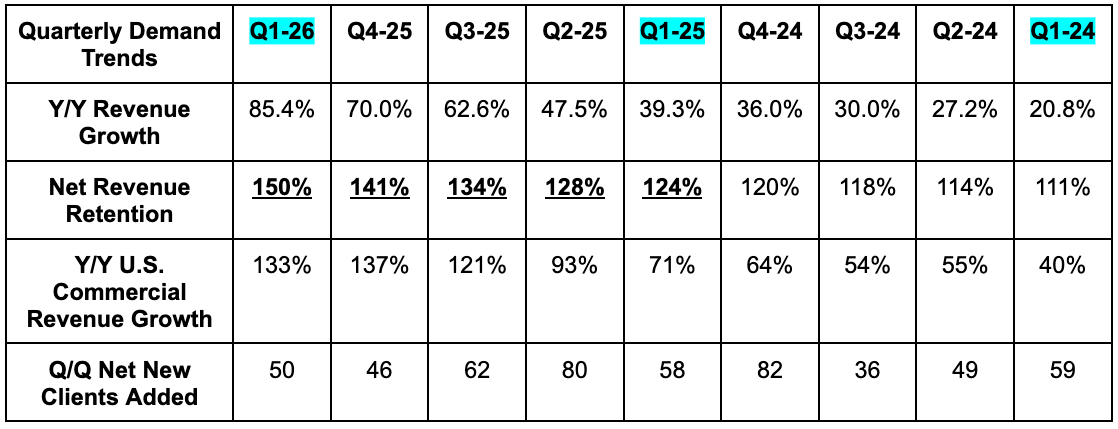

b. Demand

- Beat revenue estimates by 5.8% & beat guidance by 6.3%.

- U.S. commercial revenue missed estimates by 1.3%. More on why later in the piece.

- U.S. government revenue beat estimates by 12.5%.

- International commercial revenue beat estimates by 13.7%.

- International government revenue beat estimates by 5%.

- Billings beat estimates by 10%.

- Revenue growth from its top 20 customers rose 55% Y/Y, as it posted an incredible 150% (NRR).

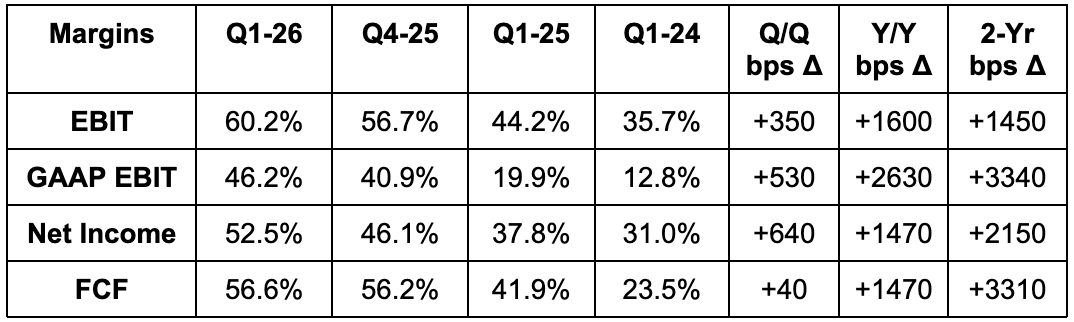

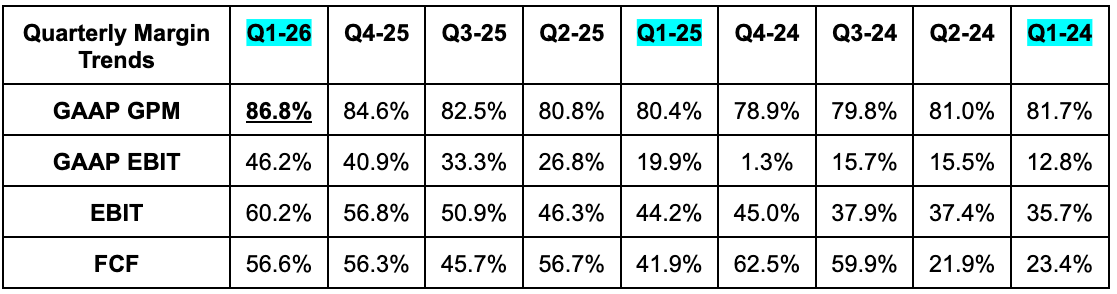

c. Profits & Margins

- Beat 84.8% GPM estimates by 310 basis point (bps; 1 basis point = 0.01%.).

- Beat EBIT estimates by 12.3% & beat guidance by 12.7%.

- Beat $0.28 GAAP EPS estimates by $0.06.

- Beat FCF estimates by 5%.

- Palantir's rule of 40 score is an astoundingly amazing 145.

- Revenue per employee continues to briskly rise as they don't grow headcount despite rapid growth.

d. Balance Sheet

Subscribe below to read about Palantir's Balance Sheet, guidance, valuation, the details of its investor materials published tonight and my take on the quarter and company.

Earnings season discounts are ongoing and wrap up soon. Read the newsletter actually sorting software winners from losers and showing you which players are fundamentally healthy.

Reviews already sent:

Upcoming reviews include AMD, Shopify, Mercado Libre and so many others.

This is where investors (including Fortune 500 executives) come for signal over noise and to invest with good reason.