Duolingo is a gamified language learning app attempting to become the standard for expressing proficiency. It’s quickly expanding into other categories like chess, music, math and literature.

Other reviews to read from this season:

- Palantir

- SoFi

- Amazon

- Meta

- Lemonade

- Robinhood

- Alphabet

- ServiceNow

- Apple

- Spotify

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

a. Key Points

- Nice margin upside driven by AI-related efficiencies.

- Third-party data shared throughout the quarter looks to be spot on.

- Investing in building out performance marketing capabilities to help growth.

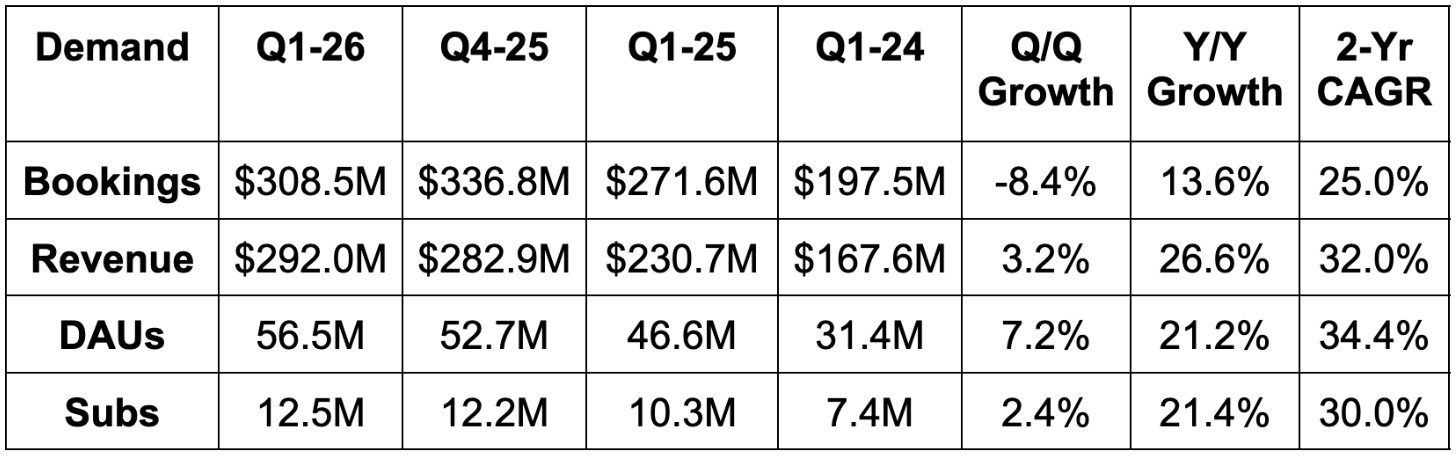

b. Demand

- Beat bookings estimates by 2.5% & beat guidance by 2.3%.

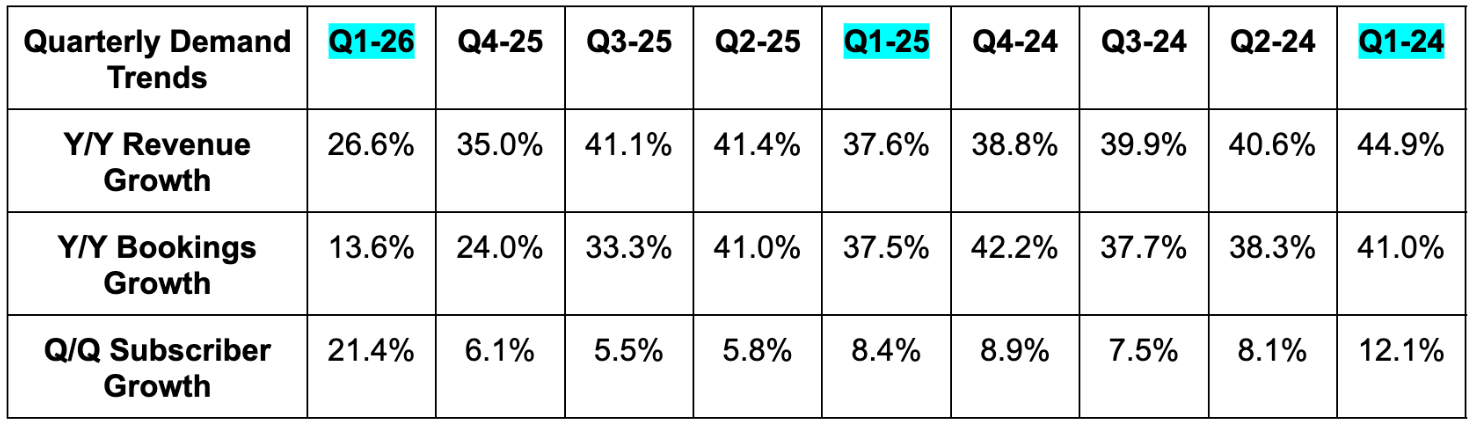

- 14% Y/Y bookings growth was 9% on a constant currency basis. This company was growing bookings at a 40%+ constant currency clip just a handful of quarters ago.

- Beat revenue estimates by 2.4% & beat guidance by 2.2%.

- Beat daily active user (DAU) estimates by 1.4%.

- Monthly active users (MAUs) rose by less than 6% Y/Y.

- Missed subscriber estimates by 1.6%.

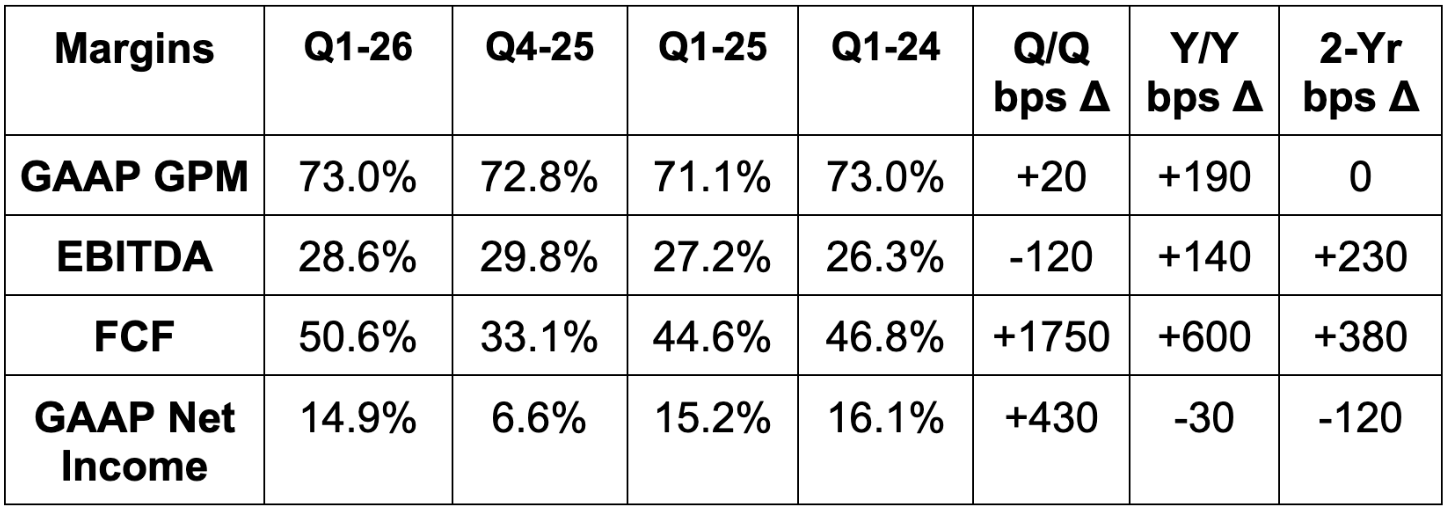

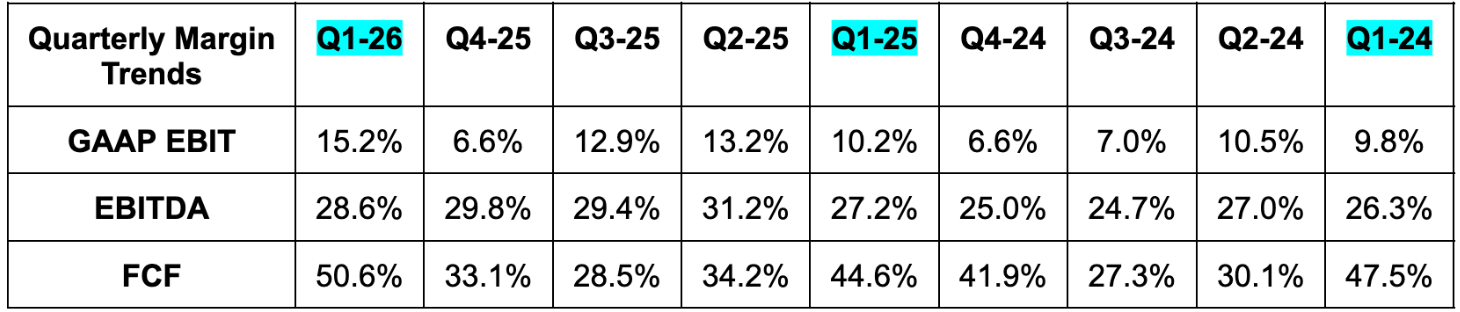

c. Profits & Margins

- Beat 71.2% gross profit margin (GPM) estimates by 180 basis points (bps; 1 basis point = 0.01%).

- Gross margin expansion was driven by reductions in per-unit AI costs and timing of AI spend growth?

- Beat EBITDA estimates by 14.2% & beat guidance by 13.6%.

- Beat $0.75 GAAP EPS estimate by $0.14.

- Beat FCF estimate by 32%.

d. Balance Sheet

Subscribe below to read about Duolingo's Balance Sheet, guidance, valuation, the details of its investor materials published tonight and my take on the quarter and company.

Earnings season discounts are ongoing and wrap up soon. Read the newsletter actually sorting software winners from losers and showing you which players are fundamentally healthy.

Reviews already sent:

- Palantir

- SoFi

- Amazon

- Meta

- Lemonade

- Robinhood

- Alphabet

- ServiceNow

- Apple

- Spotify

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

Upcoming reviews include AMD, Shopify, Mercado Libre and so many others.

This is where investors (including Fortune 500 executives) come for signal over noise and to invest with good reason.