Other reviews from this season to read:

- AMD & Uber

- Axon

- SoFi

- Amazon

- Duolingo

- Meta

- Lemonade

- Robinhood

- Alphabet

- Shopify & Coupang

- ServiceNow

- Apple

- Spotify

- Palantir

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

Table of Contents

1. Datadog (DDOG) – Q1 2026 Earnings Review

Our Datadog 101 can be found here. It offers a condensed overview of the product suite, how they provide value and how they make money. We will be referencing products throughout the piece that are defined in this article.

a. Key Points

- Added two more large AI model players as customers.

- Non-AI revenue growth continues to accelerate.

- Several new AI products were fully launched during the quarter.

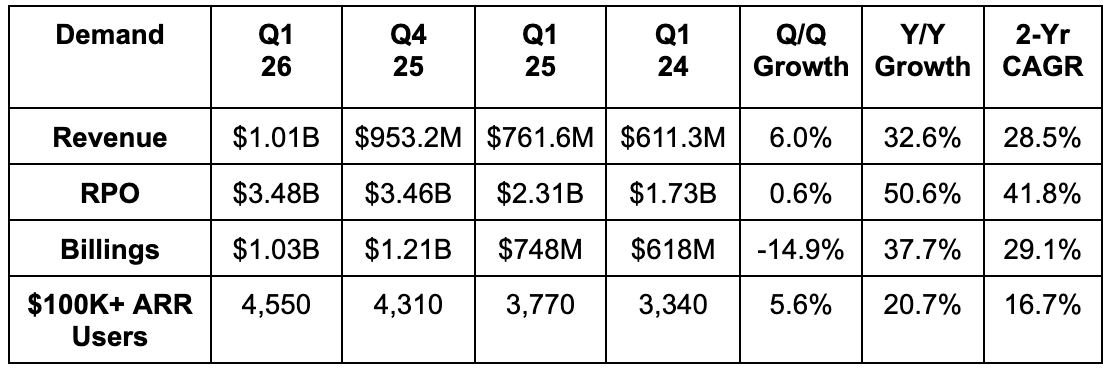

b. Demand

- Beat revenue estimate by 5% & beat guidance by 5.2%.

- Beat billings estimate by 9%.

- Beat net revenue retention estimate (NRR) by 2 points.

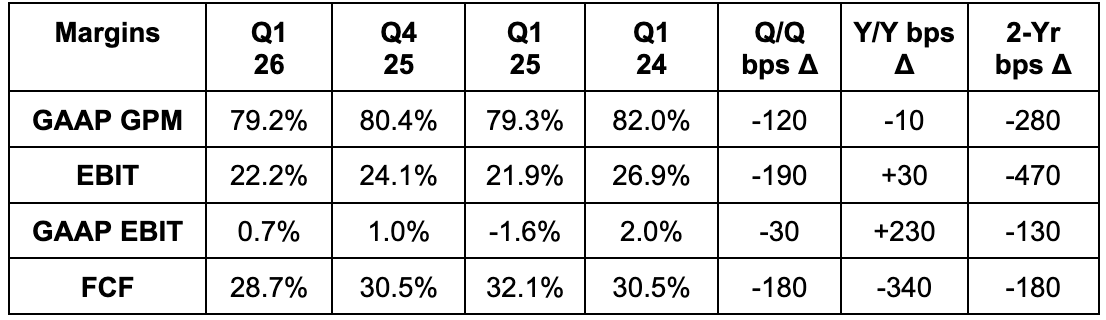

c. Profits

- Missed 80.7% GPM estimate by 50 basis points (bps; 1 basis point = 0.01%).

- Successful ramping of their new and lower-margin products is modestly weighing on GPM at the moment.

- Beat EBIT estimate by 9.6% & beat guide by 11.5%.

- Most of Datadog's AI-related spend is OpEx, not CapEx. For this reason, I found it encouraging to see EBIT margin rise Y/Y.

- OpEx rose by 31% Y/Y, compared to 29% Y/Y growth last year.

- Areas of investment include AI and “Bring Your Own Cloud” products to more easily run DDOG software in public clouds.

- Beat $0.52 EPS estimate by $0.08 & beat guide by $0.10.

- Beat FCF estimate by 89%.

d. Balance Sheet

- $4.8B cash & equivalents.

- $1B on convertible senior notes.

- 0.4% Y/Y dilution.

e. Guidance & Valuation

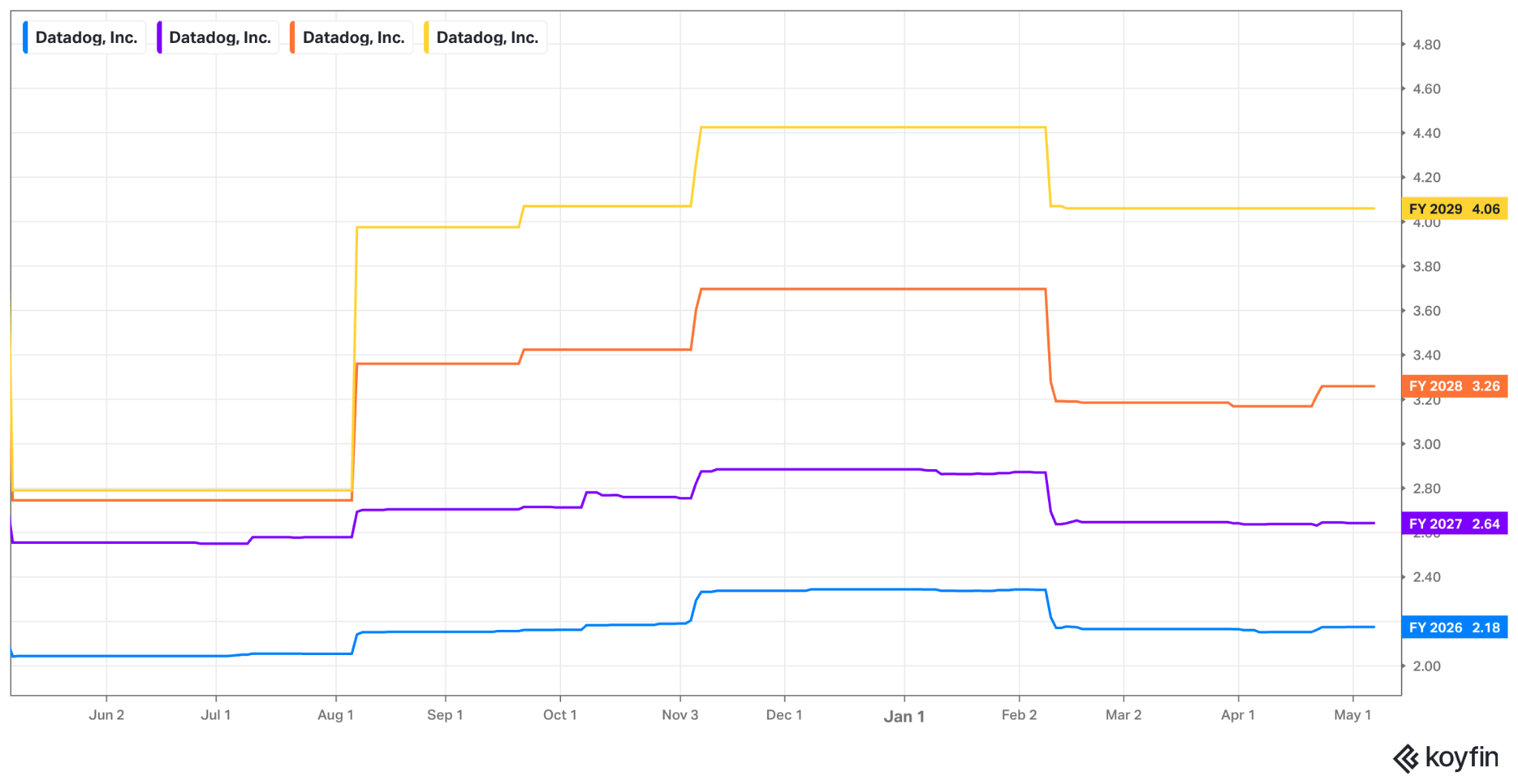

- Raised annual guide by 5.9%, which beat by 5.6%. Just like last quarter, guidance includes usage of their observed trends, while applying a degree of prudence, and an even larger degree of prudence for OpenAI contribution.

- Raised annual EBIT guide by 11.6%, which beat by 8.7%.

- Raised annual EPS guide by $0.28, which beat by $0.17.

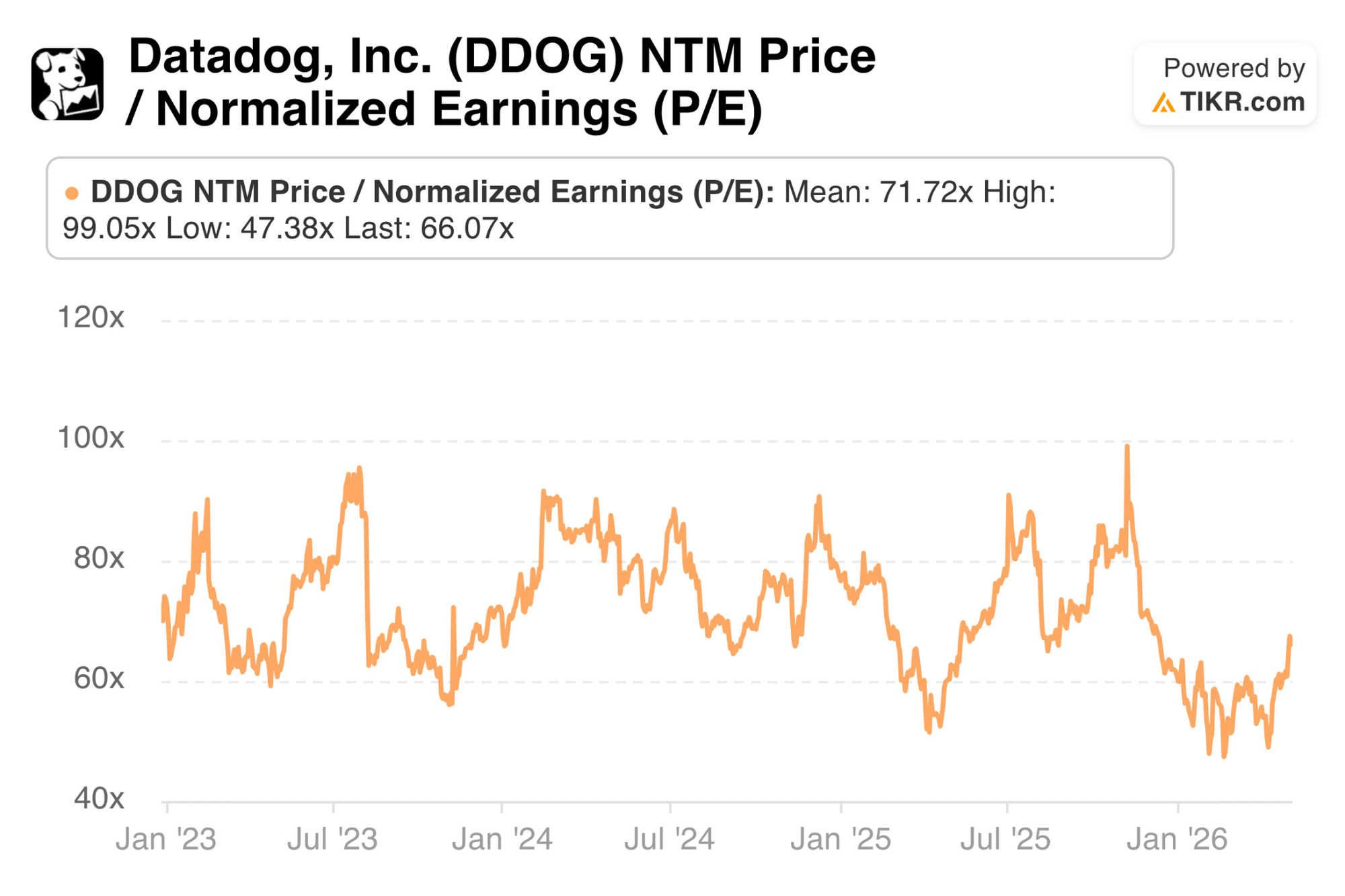

DDOG trades for 66x forward EPS and 48x forward FCF. EPS is expected to grow by 6% this year before resuming low-20% compounding over the next two years. FCF is expected to grow by 17% this year and by 23% next year. Estimates will rise in the coming days following this stellar report.

f. Call & Investor Materials

AI Positioning:

In a world where everyone is terrified about seat-based compression and licensing headwinds stemming from AI disruption, Datadog's business model is ideally positioned. Consumption is nearly 100% of their business model, with a very small contribution from seat-based licensing. They also do not care if this traffic comes from human sources or agentic sources, as monetization happens at roughly the same clip. This means the explosion in AI agents, driving a massive broadening in tech stack, surfaces, data processing, API calls, and everything else, will all be accretive for Datadog's business. As we'll see later in this piece, that's already happening.

In terms of where value will accrue in the rapidly evolving technology stacks, Datadog is optimistic that the most useful benefits will come from "operational complexity, not model intelligence." In other words, they believe that models are becoming increasingly similar, and an ability to harness these models, organize them, securely unleash them and purposefully optimize them is where the money will be made. The experience and guardrails DDOG has painstakingly built are proving to be differentiators, with plenty of compelling quantitative evidence to support this notion. More later.

It's one thing to vibe code a pretty user interface and colorful screen that can accomplish an impressive workload. To the untrained eye, that looks like magic and is why people are so afraid of every random announcement that Anthropic and OpenAI make. It's another thing to make sure this is done in the most efficient way possible, with the lowest error rates possible, and always with proper governance and responsible deployment.

- The recent surge in coding agents does not at all threaten this company's competitive positioning. Instead, it provides more traffic and more assets for Datadog to consolidate, observe, optimize, and monetize.

Product Innovation – GPU Monitoring:

Not so shockingly, all of the product updates from this quarter fell under the AI umbrella.

Several of the products Datadog has been working on launched to their broader customer base during the quarter. Starting with GPU Monitoring, Datadog is extending and retrofitting its world-class observability stack to malleably and effectively work for modern accelerators. And while it's called "GPU Monitoring," it probably should be called "high-performance chip monitoring," as it includes coverage of custom processors from Google, Amazon, and others. This is important. Homegrown and competing third-party observability tools are rapidly trying to add this important new class of assets to their capabilities. And? They're failing. Datadog is not. Rather, it is extending its lead within that core niche and fostering market share gains against everyone else. As data center environments begin to incorporate more custom processors and a more diverse menu of components, the complexity Datadog uniquely solves for will remain highly valuable.

A few more notes here. AI inference had been the largest opportunity for Datadog up until recently. That's now morphing into both inference and training. They are seeing a broadening in the number of companies willing to consistently train models for their own granular needs, vs. relying on frontier models to do everything. That creates yet another tailwind for Datadog's business. Furthermore, Datadog is beginning to win more hyperscaler workloads and contracts to support their next-generation observability. This is a great addition to the pile of evidence supporting DDOG’s sustainable defensibility.

These are the richest companies on the planet with the most tech talent and competing offerings across much of what Datadog provides. Their decision to go with this company instead of building internally is telling. Finally, while everyone is fixated on AI infrastructure return on investment, Datadog is a key ally in making sure these assets are providing as much value and financial gain as they possibly can. It's a good place to be in as the AI cycle rolls on.

Product Innovation – More Launches:

DDOG also launched its Model Context Protocol (MCP) Server, Bits AI and Experiments. These are all defined in the 101 section linked at the top of the article. For quick review, the MCP offering provides a standard framework for agents to access needed information and to work. It’s the agentic rail. Datadog Experiments allows for scaled split testing of agentic assets to test performance, potential vulnerabilities and user response before pushing changes to runtime environments. They were notably excited about the potential this has for the App Performance Monitoring (APM) bucket, as the tool should be highly valuable for screening and testing changes before annoying customers with unknown blunders. Finally, the Bits AI security agent is cutting threat investigation time by 98% in early usage with data-driven suggestions on optimal remediation.

Demand – More General Context:

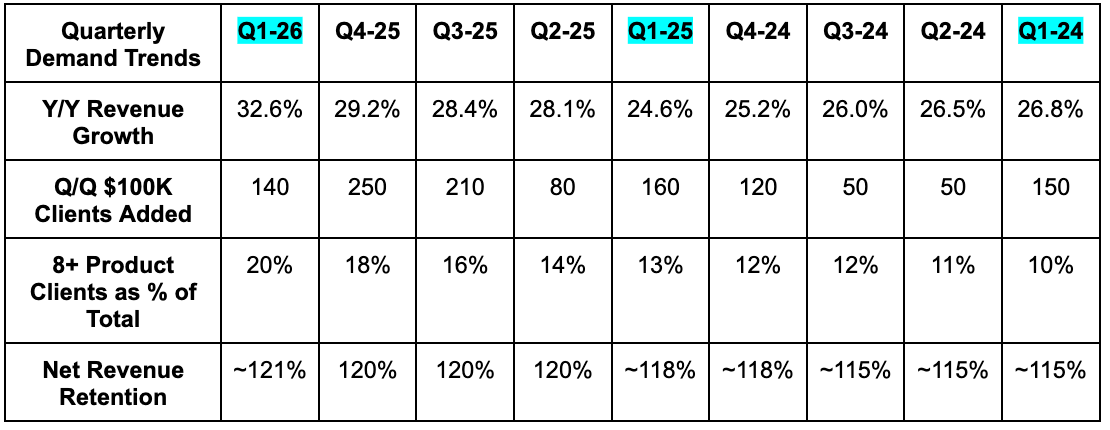

Demand trends were fantastic during the quarter. Some of that's related to previous go-to-market fixes bearing fruit, but underlying interest in the Datadog products is structurally powering most of this momentum. And as we'll see later on, this is not confined to an AI story. Demand across its AI and non-AI cohorts looks uniformly healthy. For more context, this was the strongest period for existing customer Q/Q usage growth in four years. Net new annualized revenue (different from annual recurring revenue in this case) was a new record and kept up a very strong pace in the area. Churn levels are low and stable, new logo bookings rose by 100% Y/Y. Average deal size per new customer also doubled Y/Y. Current remaining performance obligations (RPO) rose by 45%. In a word… Wow. What AI disruption?

As with previous quarters, multi-product adoption and rising average modules per contract continued to fortify Datadog as the leading observability platform. Similar to other software companies, more cross-selling means lower churn, better client outcomes, higher lifetime value, more proprietary data, better margins, higher revenue quality, longer runways, and more successful enterprises. You could call it important. 56% of its customers now use 4+ products vs. 51% Y/Y. 6+ product trends and 8+ product trends are equally encouraging. And while this is going very well, they still have plenty more cross-selling and platform-wide adoption to drive. They have 18 products of their 23 that haven't yet reached $50M in ARR. Their other 5 have, and they think the remaining 18 have a great shot to get there over time.

Leadership ran through a few deal highlights during the quarter, with a couple qualitative anecdotes that I found encouraging. They won a global hedge fund that tried to build an open source stack and failed to control costs or create positive outcomes – even in the vibe coding era. Shocker. And notably, they also signed two large deals with "AI research divisions" at two of the world's largest technology companies. Internet rumors and cloud contract breadcrumbs point to Microsoft and Meta, but we're speculating. I’ve seen others say one of them is Anthropic, and I guess you could certainly consider that one of the world's largest tech companies at this point. Regardless, this is two large contracts with two companies perceived to be the most capable in terms of building substitute solutions, and foregoing reliance on Datadog. There were several other 7+ figure deals highlighted, but there's no reason to go through the repetitive examples.

Demand – AI vs. Non-AI:

Starting with AI, existing customer growth Looks great and instills confidence in strong renewals and net revenue retention from its AI product innovation. Demand for its agentic investigations doubled sequentially, while spans sent to LLM observability tripled during that period. MCP server calls quadrupled Q/Q, and Bits AI assistant messages spiked higher as well. Furthermore, improving customer diversity was an encouraging, quarterly highlight. While OpenAI definitely represents a large ~$200M chunk of Datadog business, it now has 22 customers in the AI cohort spending $1M+ annually, and five spending $10M+ annually. This is not just an OpenAI story with firm expectations that demand broadening will continue. And again, guidance for next quarter was fantastic, despite baking even more prudence into their OpenAI assumptions than they do for the rest of the business.

Non-AI demand was also elite. Revenue, excluding the AI cohort, stepped-up to roughly 25% Y/Y compared to 23% last quarter and 19% last year. And remarkably, when stripping out their largest AI customer (OpenAI), from quarterly results, net new annualized revenue still set a new company record. Even without the AI tailwind, this business is accelerating, as appetite for cloud migrations remains large and demand across their entire suite remains robust. What looked good for Datadog this quarter? Everything.

More Notes:

- They achieved FedRAMP high certification on Datadog for Government, which opens the door for a lot more public sector deals. The company's been building go-to-market teams ahead of this expected decision, but they still have a little bit more work to do on that end, before they're ready to aggressively pursue this opportunity.

- Partnered with Sakana AI to collaborate on enterprise AI adoption in Japan. If all goes well, they should become a global partnership in the not-too-distant future.

- They are seeing no deterioration in the macro environment whatsoever.

g. Take

Subscribe below to read my take on Datadog and the quarter. Also read a full Mercado Libre review and detailed earnings reviews on the following companies:

- Axon

- Shopify & Coupang

- AMD & Uber

- Meta

- Palantir

- SoFi

- Duolingo

- Amazon

- Lemonade

- Robinhood

- Alphabet

- ServiceNow

- Apple

- Spotify

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

If you'd like to read that and full reviews on 40+ companies this season (and so much more), upgrade below.