Other reviews from this season to read:

- AMD & Uber

- SoFi

- Amazon

- Duolingo

- Meta

- Lemonade

- Robinhood

- Alphabet

- Shopify & Coupang

- ServiceNow

- Apple

- Spotify

- Palantir

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

I published an Axon Deep Dive a few months ago that can be found here. Part of that coverage includes a full explanation of their large product suite. If you need a definition for a product discussed below, it’s in there and findable with a quick “control f”

Table of Contents

a. Key Points

- Their counter drone offering is thriving.

- Impressive AI ramp.

- Near-term margin pressures.

- Signed a new $40M enterprise agreement with a large telecom provider.

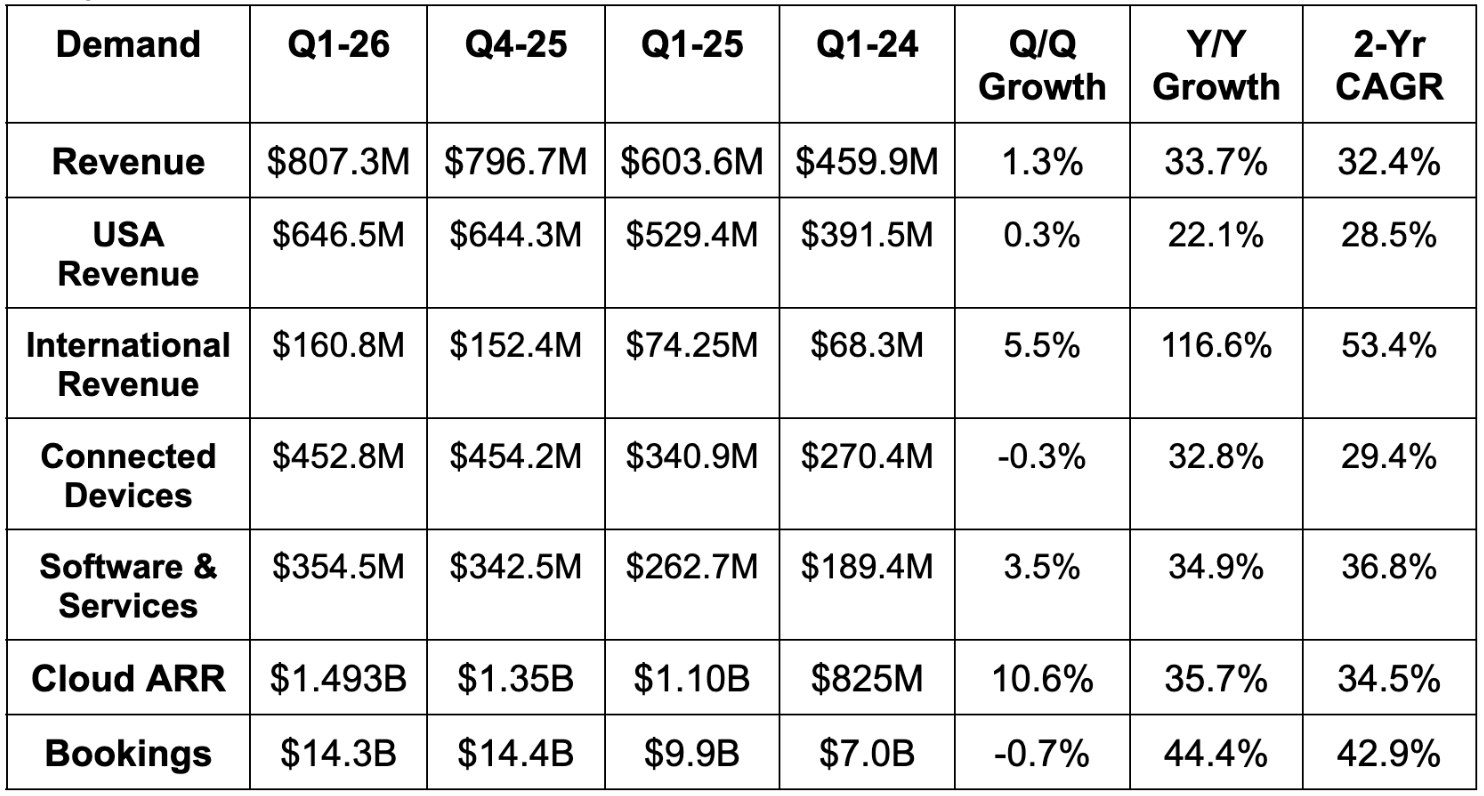

b. Demand

- Beat revenue estimate by 3.6%.

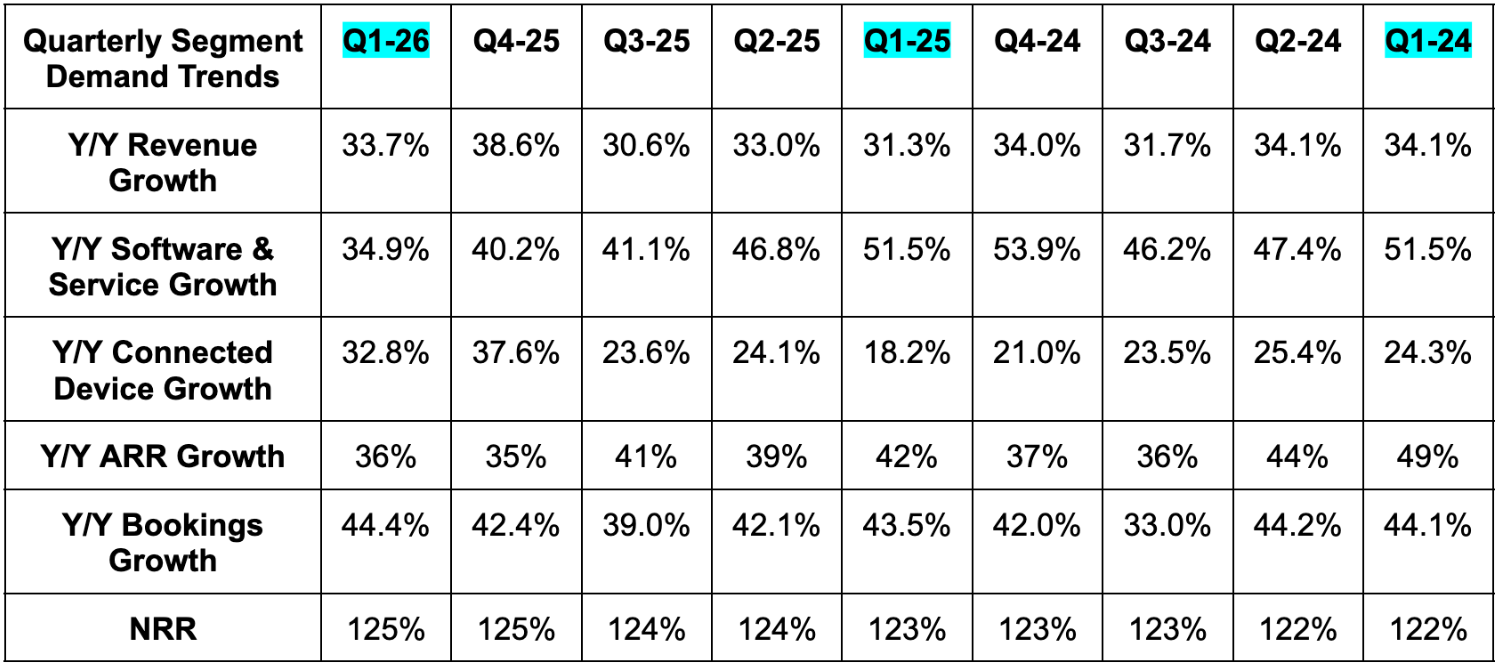

- Every product delivered at least 10% Y/Y growth. Its most mature taser segment grew by 19% Y/Y, while personal sensors, its second most mature offering, rose by 23% Y/Y. Still plenty of growth left there, and they haven't even rolled out their new cartridges which solve clothing thickness issues and eliminate a key hurdle to more adoption.

- Beat cloud ARR estimate by 3%. Net new ARR beat estimates by 40%.

- U.S. public safety, international and enterprise segments were highlighted as standouts for bookings.

“Breadth of overall demand is compelling. It tells us that the growth we are seeing is not isolated to 1 product, 1 geography or 1 customer segment.” – Axon President Joshua Isner

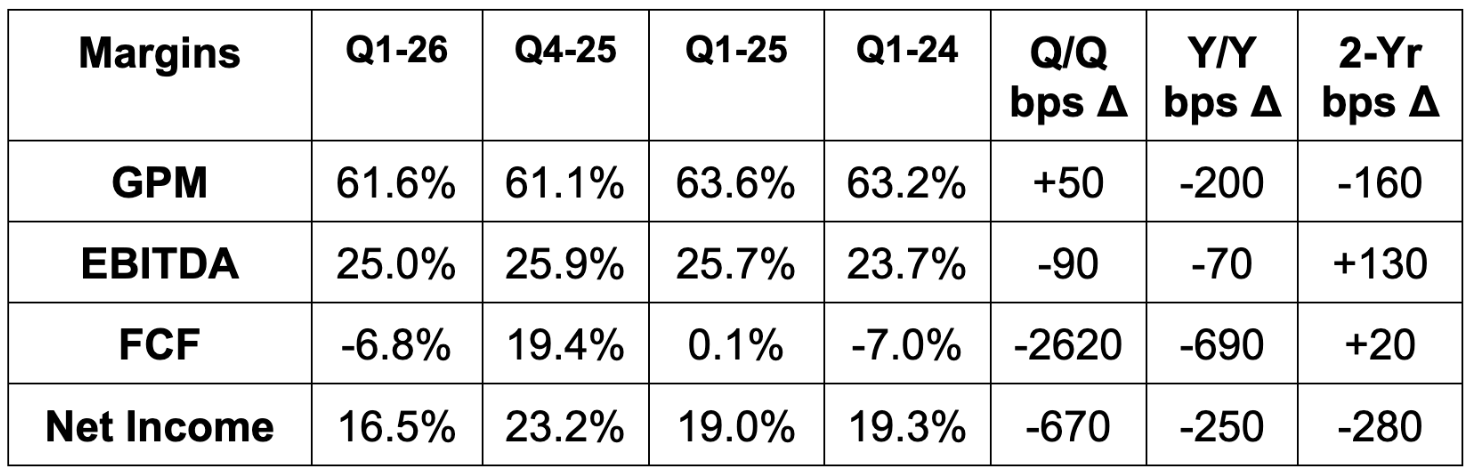

c. Profits & Margins

- Met GPM estimates.

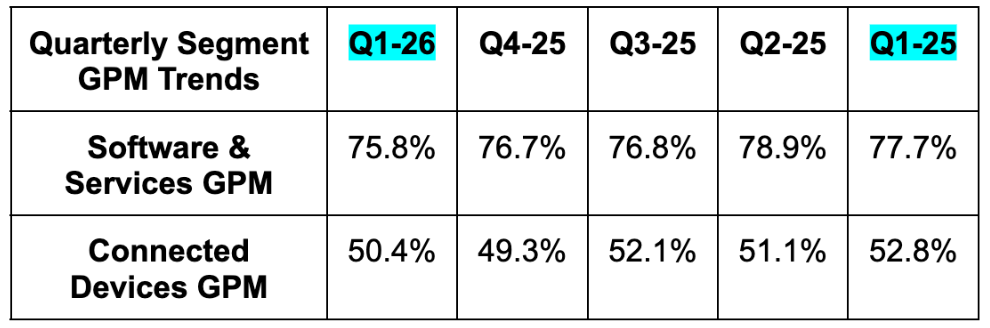

- Connected Devices GPM pressure was due to tariffs and strong Dedrone growth.

- Software & Services gross margin fell due to more professional service fees related to a large batch of new product deployments. Software GPM in isolation remained over 80%.

- Beat EBITDA estimates by 9.8%.

- EBITDA rose by 30% Y/Y via higher revenue. Potential margin expansion was forgone to invest more heavily in R&D, while GPM pressures described above also led to modest Y/Y margin pressure.

- Beat $1.59 EPS estimates by $0.02.

- Sharply missed FCF estimates due to investments to build out its Dedrone inventory amid positive demand signals.

- They are very encouraged by demand for all of their hardware, and want inventory to support expected growth over the next couple of years. Memory inflation did have a small impact on inventory growth, but the vast majority was related to the buildout.

As discussed in the recent deep dive, a blend of payroll tax accounting and equity portfolio valuation swings both make net income and FCF noisy. This is the one rare case where EBITDA is actually the least noisy and most useful metric among headline numbers.

d. Balance Sheet

Subscribe below for an overview of Axon's balance sheet, guidance, shareholder letter, lengthy conference call and my take on the quarter and company. Also read detailed earnings reviews on the following companies:

- AMD & Uber

- Shopify & Coupang

- Palantir

- SoFi

- Amazon

- Duolingo

- Meta

- Lemonade

- Robinhood

- Alphabet

- ServiceNow

- Apple

- Spotify

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

If you'd like to read that and full reviews on 40+ companies this season (and so much more), upgrade below.