1. AMD (AMD) – Q1 2026 Earnings Review

AMD 101:

AMD designs CPUs and GPUs, offers software and provides connectivity equipment for a wide array of cloud and enterprise clients. If there’s one thing the semiconductor industry loves, it’s constantly changing the names of products with a swarm of acronyms for us to juggle. What matters? AMD’s positioning within these areas and how it’s integrating them with its rack scale data center offering called Helios.

- Rack Scale is a data center blueprint that treats a server rack as a compute building block rather than the individual servers. Rack scale enables larger, more efficient connections between GPUs to turbocharge compute performance, density and efficiency.

- Taiwan Semi manufactures the chips that AMD designs.

GPU: Graphics Processing Unit. This is an electronic circuit used to process information and data. The accelerated compute needed for GenAI apps and models pulls from next-gen GPUs. AMD leadership believes its “MI” series GPUs compete very formidably across memory and bandwidth with Nvidia. They’re enjoying some nice momentum and market share in this arena, but Nvidia is still considered the performance leader by most.

- MI series GPUs are part of the “Instinct” product family.

CPU: Central Processing Unit. This is a different type of electronic circuit that carries out assignments and data processing. CPUs fall in the general compute bucket. General compute CPUs are still optimal for static, step-series and instruction-based tasks. They’re also much cheaper than deploying next-gen GPUs when they can work for the specific use case.

- AMD's family of data center CPUs is called EPYC. The latest iteration of EPYC is called Turin, with Venice coming soon.

- Its desktop and gaming CPUs are called Ryzen.

- AMD and Intel are the big boys in this market, with AMD consistently taking market share over the last several years.

More to Know:

- NPU: Neural Processing Unit: Used for AI-enabled personal computers (PCs).

- Data Processing Units (DPUs) (or Network Interface Cards (NICs)): High-performance compute accelerators that assume some of the work from generalist CPUs to allow those CPUs to focus on main tasks

- TOPS: Tera Operations Per Second. This measures NPU performance, with more TOPS being better. TOPS superiority is imperative for running Copilots and GenAI apps on PCs with optimal latency and model performance.

a. Key Points

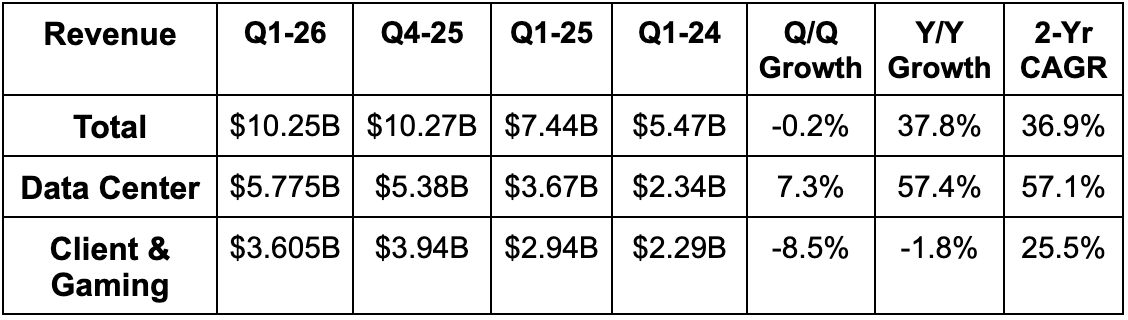

- Strong data center CPU demand drove most of the outperformance.

- GPU revenue fell sequentially due to a lower China contribution.

- Engagement for Helios remains strong and that system is on schedule.

- Memory inflation is impacting its consumer & gaming segments.

b. Demand

- Beat revenue estimate by 3.6% & beat guidance by 4.6%.

- Beat data center revenue estimate by 2.9%.

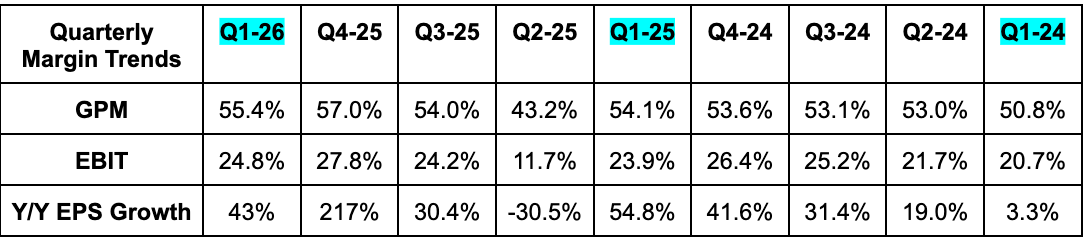

c. Profits & Margins

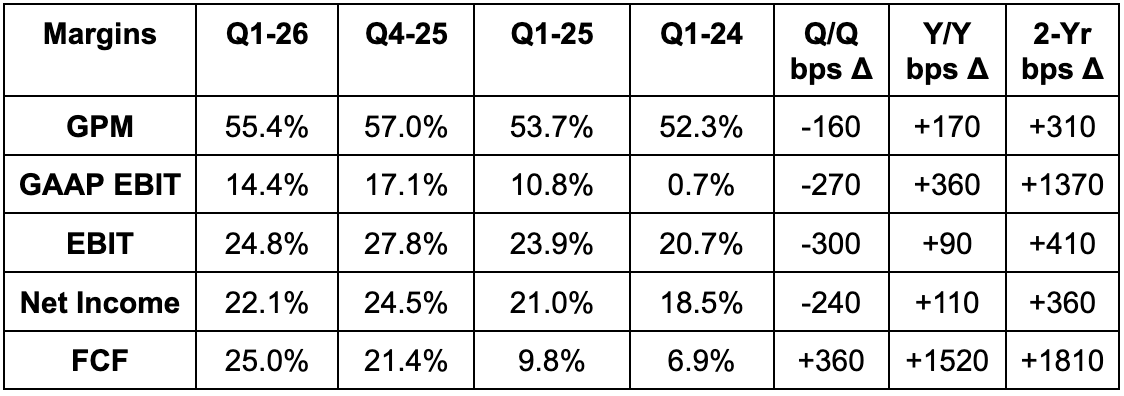

- Beat 55% GPM estimate & beat identical guidance by 40 basis points (bps; 1 basis point = 0.01%) each. CPU-based data center revenue mix shift drove GPM outperformance.

- Beat EBIT estimate by 5.4%.

- GPM outperformance and the revenue beat powered the strong EBIT result. Operating expenses actually rose by 42% Y/Y, which was above guidance, so that did not contribute to the successful result.

- Beat $1.28 EPS estimate by $0.09.

- Beat FCF estimate by 9%.

d. Balance Sheet

- $12.3B cash & equivalents.

- $3.1B debt.

- 1.5% Y/Y dilution.

e. Guidance & Valuation

- Q2 revenue guidance beat estimate by 6.5%.

- Q2 GPM guidance beat 55.3% estimate by 70 bps.

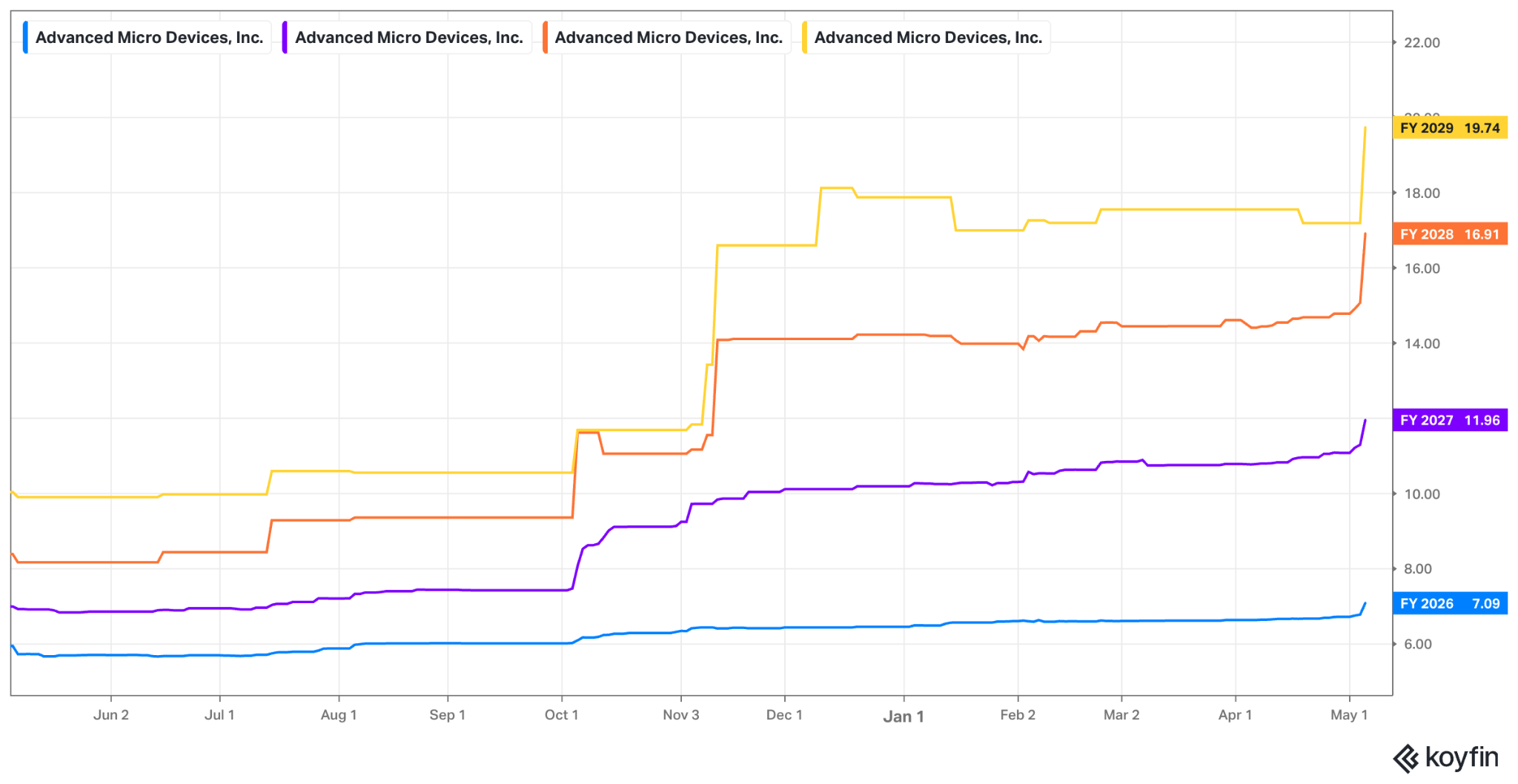

- AMD sees a “clear path” to beating its timeline to reaching $20 in EPS.

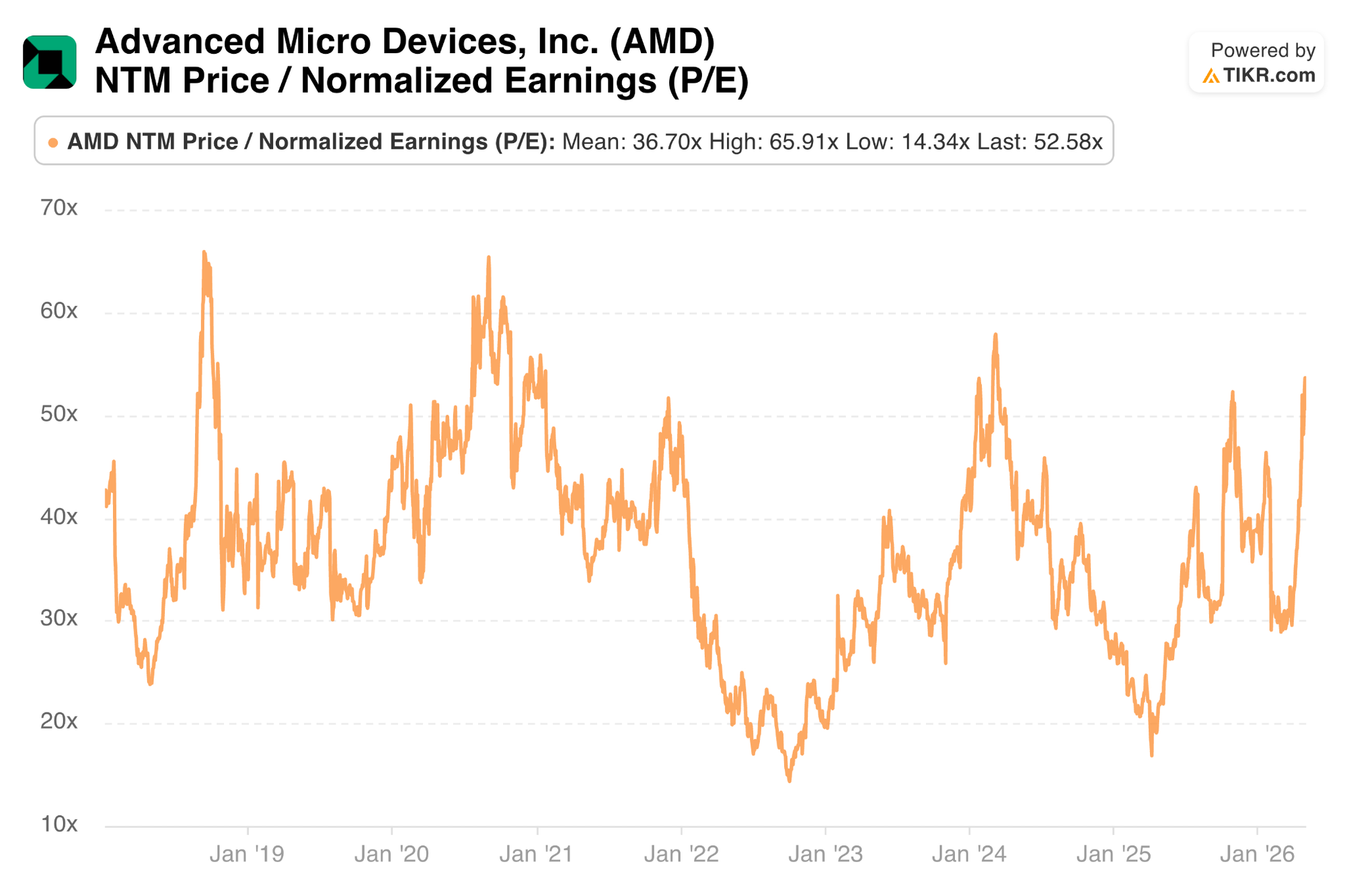

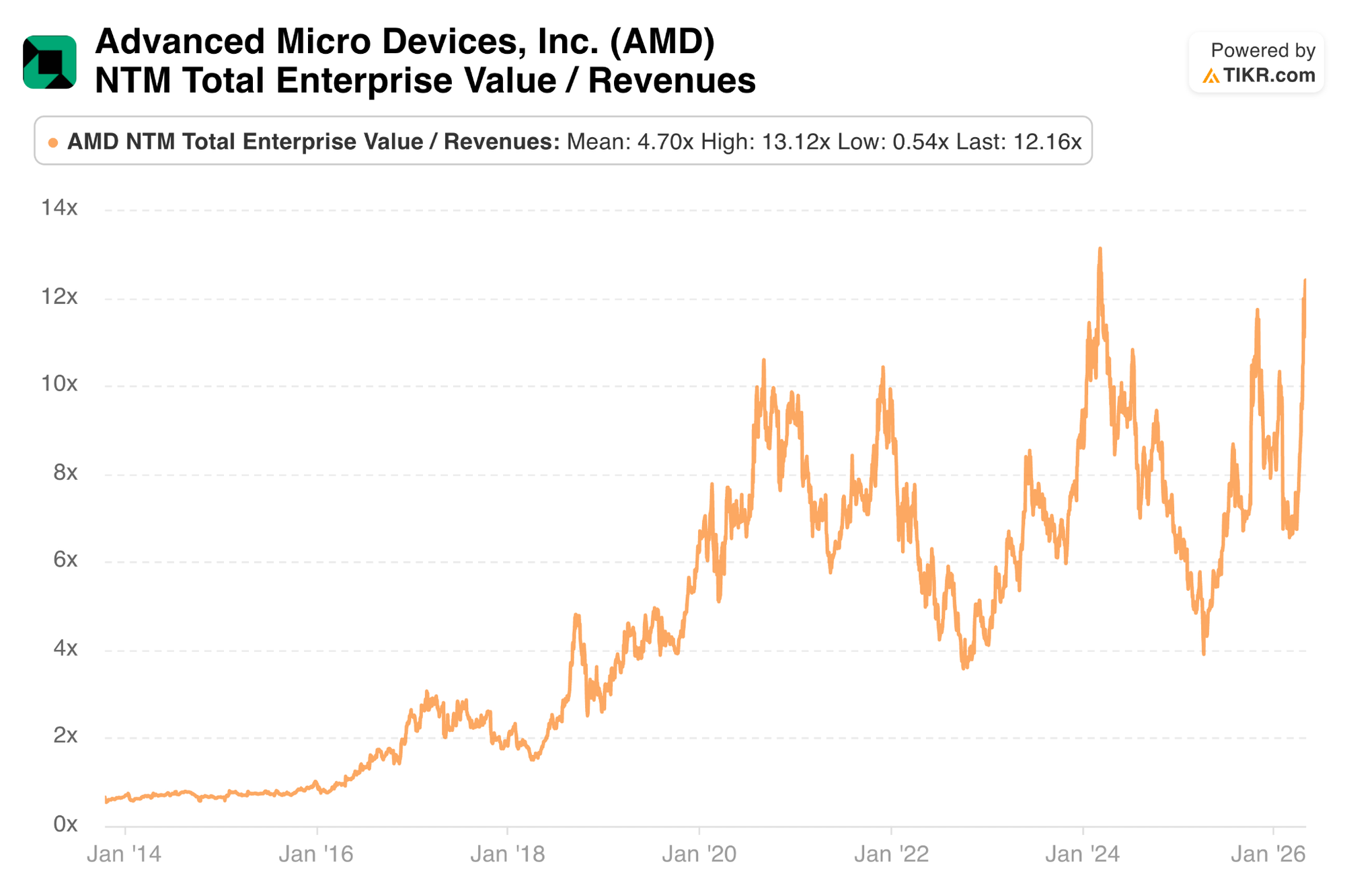

AMD trades for 53x forward EPS. EPS is expected to grow by 70% in each of the next two years thanks to 44% revenue compounding and a lot of leverage.

f. Call & Investor Materials

Thriving Data Center CPU Business:

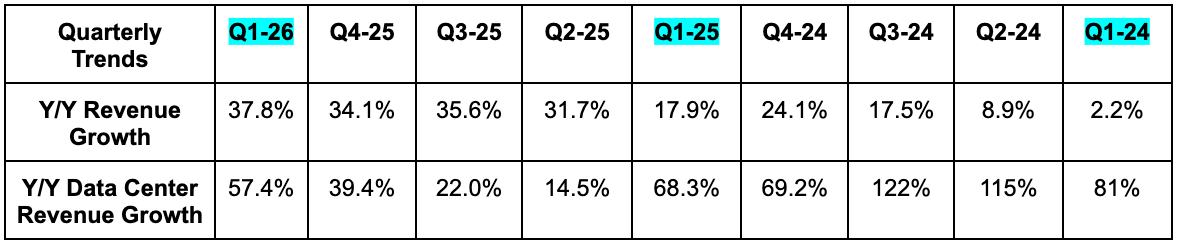

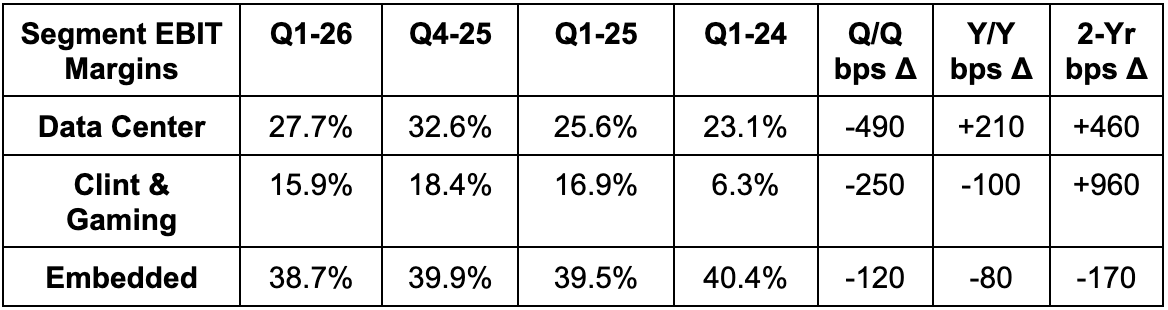

This quarter was all about an explosion in AI-related CPU demand. That is where most of the outperformance came from, as CPUs delivered 50% Y/Y growth and are gearing up for 70% Y/Y growth for Q2. Success across cloud giants and an increasingly broad list of enterprise customers catalyzed the strong result (+50% Y/Y revenue for both cohorts), while “robust growth” is expected to continue into 2027. Incredibly, since AMD's Investor Day just a few months ago, they are now doubling their total addressable market estimate for 2030, from $60B to $120B. Despite the much larger market, they also remain confident in reaching 50% market share during the planning period like they previously telegraphed.

Where is this resurgence in AI-based CPU demand coming from? As Lisa Su explained it, inference growth leads to more agents, and agents rely on CPU compute to complete their tasks. GPUs provide the inference and generation of optimal workflows. CPUs are relied on to complete simple, formulaic tasks within workflows, making them the ideal choice for agentic work allocation. While AI data centers have featured an eight-to-one ratio of GPUs to CPUs in recent years, AMD sees that eventually approaching a one-to-one ratio. This is creating a positive correlation between AI demand and CPU demand, which is currently benefiting AMD and Intel as well. Su feels poised to take the lion's share of that opportunity with their new 5th-generation EPYC CPUs extending their performance lead vs. the field. Its 6th generation product lineup, which features its first CPU built specifically for AI data centers, is also on track to debut in 2026, with performance AMD thinks will double other x86 processors and also double the throughput of ARM-based systems.

They were asked explicitly about ARM and the increasing popularity of their CPU architecture. AMD views those offerings as high quality but “more like point solutions” compared to the AMD platform – and again not as highly performing. With AMD, you get the CPUs, the GPUs, and their ROCm suite of software to help optimize hardware at every turn and extract more value throughout their useful lives.

One more important note on CPU-related demand. The explosion in growth is not coming from aggressively jacking up prices. It is predominantly coming from volume growth, which is higher-quality and more sustainable than what we’re seeing in the memory market right now. This is really good news for AMD bulls, in my opinion. They are determined to take good care of customers and only pass on price increases when they need to, as they know structural growth will depend on fair pricing, and delivering a lot more CPUs over the coming years.

Emerging GPU Business:

AMD is also very excited about better-than-expected interest in their MI450 series GPUs and Helios rack-scale platform. This platform is still on track to ramp shipments during the second half of the year, which is when GPU growth is expected to meaningfully accelerate. Strength is across both training and increasingly inference, as strong performance, efficiency and lower price tags win customers over.

This quarter, sequential growth was actually negative for this subsection of the data center business, because of a sequential decline in business collected from China. That should be very temporary. Again, as new GPUs and rack scale systems become available and close performance gaps vs. other products in the market. The observed GPU demand signals give AMD confidence in exceeding their multi-year growth target of 80% Y/Y. Certainly a positive data point for cycle longevity in AI infrastructure.

The explosion in CPU demand left some a bit concerned over whether that was cannibalistic or incremental compared to GPU demand. As already mentioned, the growth in agents is what is directly propping up growth in CPUs, so it’s mainly additive to the overall opportunity.

Finally, for GPU-based margins, there is going to be a GPM headwind as Helios ramps into the back half of the year. They've been very candid about this, and it's not a surprise. The team is in "land grab" mode at the moment. They are not focused on optimizing cost efficiencies, and instead are fixated on assuming as much market share as they possibly can, with their increasingly competitive offering. There's plenty of opportunity down the road to optimize margins. Now is just not the time. Easy thing to accept when overall results look so great.

Deal highlights during the quarter include:

- Meta’s plans to add 6 gigawatts of AMD GPU-powered compute. They’ll also be a “lead customer” for its new CPUs, showing how offering both products can lead to larger, stickier deals. They’ll begin executing these commitments around when Helios starts ramping later in the year.

- Tata Consultancy Services (TCS) in India will partner with AMD to “co-develop” Helios systems for their specific sovereign AI needs.

- AMD and Samsung are collaborating on cohesively developing the next generation of GPU and memory systems.

- Partnering with NAVER in Korea for sovereign AI use cases there.

Software:

Aside from adding immediate support for new models, there wasn’t much time spent on this part of the business. We did hear that the acceleration in cadence of updates continued through Q1 and that the team is on a great rhythm of improvement.

Non-Data Center Segments:

The client business continued to take more market share as it delivered 23% Y/Y growth for the period. Throughout their slew of desktop and mobile chips, growth is robust and product roadmaps are quickly advancing on schedule. Commercial mobile demand was especially strong here, with 50%+ Y/Y growth thanks to strong demand from Lenovo and its other OEM partners.

While demand levels should remain healthy during Q2, memory inflation is having an impact on this segment. Inflation, especially on the lower cost side of the personal computing market, is limiting demand.

Gaming demand was impacted by console cycle timing as expected. Forward-looking engagements look strong, which positions this segment for more fun results during the more favorable parts of these cycles. For the Q2 and likely most of 2026, memory inflation will hold this segment back just like it will on the client side. If you’re wondering why this isn’t impacting the data center business, it’s because demand and pricing power remain historically amazing at the moment.

- Embedded segment design wins rose by 10%+ Y/Y.

On Supply Chain Health:

AMD is calling supply chain visibility strong. They know exactly what GPU is going to be installed in what data center through 2027, and have memory supply on hand through the end of next year to make all of that happen.

g. Take

Subscribe below to read my take on AMD and the quarter. Also read a full Uber review and detailed earnings reviews on the following companies:

- Shopify & Coupang

- Palantir

- SoFi

- Amazon

- Duolingo

- Meta

- Lemonade

- Robinhood

- Alphabet

- ServiceNow

- Apple

- Spotify

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

If you'd like to read that and full reviews on 40+ companies this season (and so much more), upgrade below.