Other reviews from this season to read:

- Mercado Libre & Datadog

- AMD & Uber

- Axon

- SoFi

- Amazon

- AppLovin & Cloudflare

- Duolingo

- Meta

- Lemonade

- Robinhood

- Alphabet

- Shopify & Coupang

- ServiceNow

- Apple

- Spotify

- Palantir

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

1. The Trade Desk (TTD) – Earnings Review

Click here for an overview of The Trade Desk's business.

a. Key Points

- They continue to blame softer guidance on macro.

- Leadership is adamant that structural tailwinds remain intact.

- They are optimistic that the feud with Publicis will soon be over.

- Chief Strategy Officer Sam Jacobson is leaving for OpenAI.

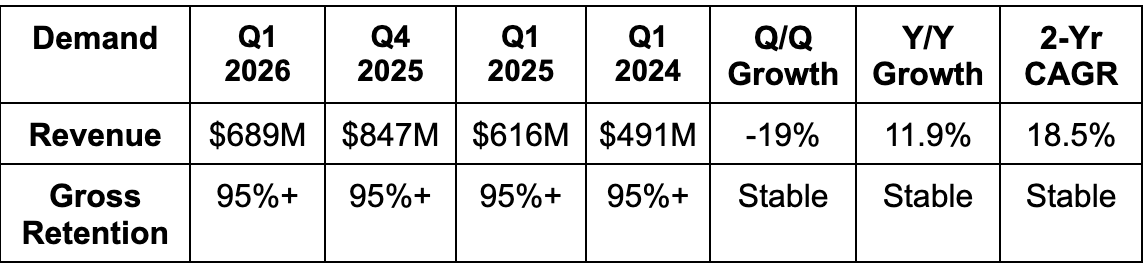

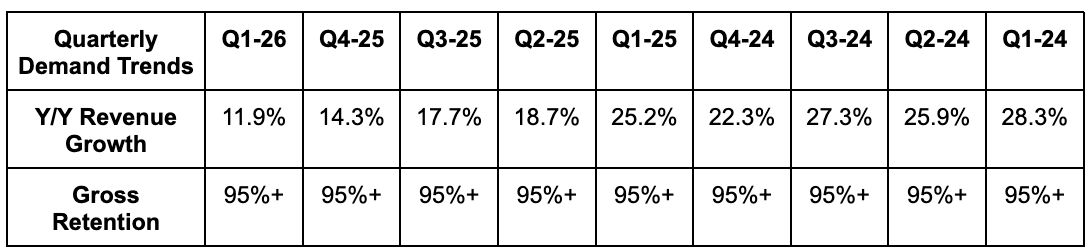

b. Demand

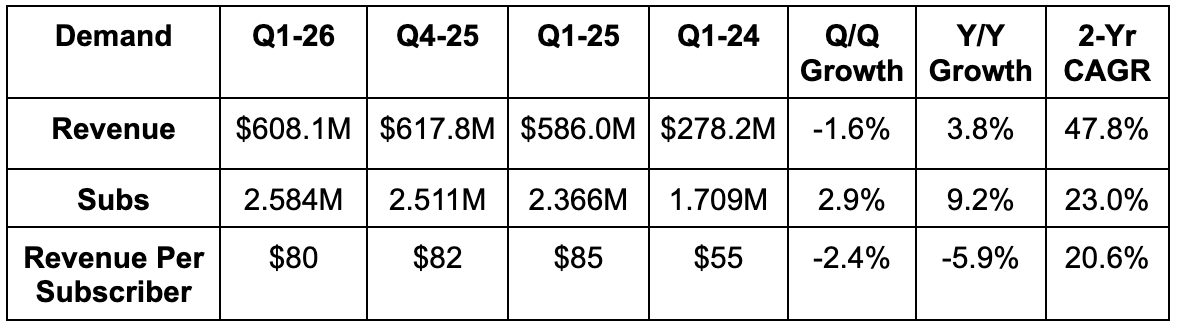

The Trade Desk beat revenue estimates by 1.5% & beat its “at least” revenue guidance by 1.6%.

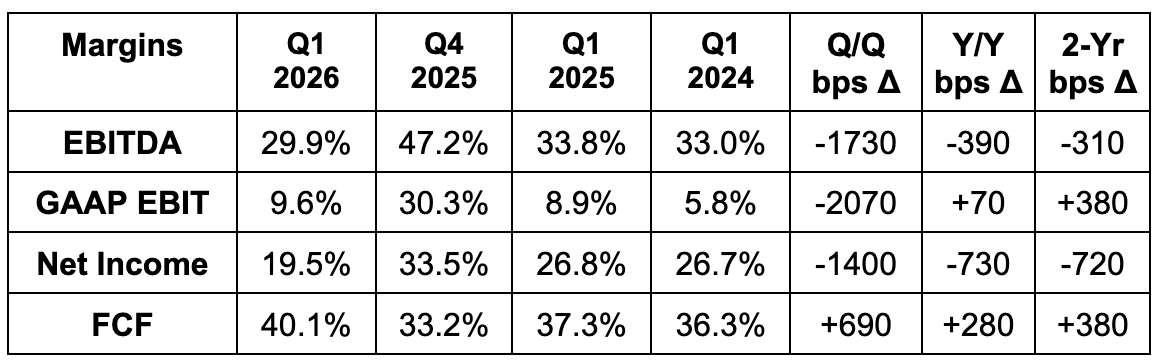

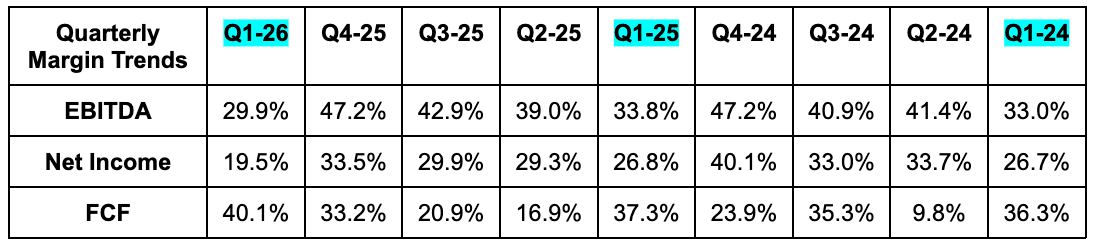

c. Profits & Margins

- Beat EBITDA estimate by 4.9% & beat guide by 5.1%.

- OpEx grew by 18% Y/Y to support platform-level innovation.

- Missed $0.32 EPS estimate by $0.04.

- EPS fell by 15% Y/Y.

d. Balance Sheet

- $1.4B cash & equivalents.

- No debt.

- Diluted share count fell by 5% Y/Y.

- Very pretty balance sheet.

e. Guidance & Valuation

For the full year, they continue to expect a 40%+ EBITDA margin, which should be roughly flat Y/Y. That was good to hear amid the 3 points of Y/Y margin contraction seen during Q1. They will get cost leverage from headcount to make up for upcoming platform-level investments. The plan is to grow their employee base at a slower pace than the business this year.

f. Call & Release

Weak Macro:

The Trade Desk blamed Macro for yet another disappointing performance vs. consensus – despite lowered expectations. It's interesting… companies that are fundamentally weaker will routinely blame Macro for their shortcomings more than direct competitors that magically are seeing more constructive backdrops. I realize that The Trade Desk caters more to global brands and these are more susceptible to tariff headwinds and geopolitical concerns. At the same time, AppLovin, Meta, Google, and Amazon all have large clients in the verticals TTD is calling out as especially weak. They are not seeing that weakness in the same light, which leads me to believe that this is not macro, but the company's own blunders continue to hold them back. Programmatic advertising remains an attractive secular growth story, and 2026 includes midterm election tailwinds that have historically led to easy year-over-year accelerations at this company. Last year, we were told that growth acceleration would happen in 2026. At this point, it's clear that's not going to come remotely close to happening. They can blame Macro headwinds that pop up, but I'm really just not buying it.

I think their mess of a Kokai platform rollout, their constant stream of organizational and strategic changes, their very public battles with large agencies accusing them of unfair take rates, their C-suite that resembles a revolving door, and intense competition from Amazon and others are the reasons for their disappointing results. If Macro was amazing, their consumer packaged goods and other struggling verticals would obviously be growing faster than they are right now. But if this company was in healthier and better shape, they would not be so seemingly fragile; they'd be more capable of overcoming these things as they pop up. They clearly are not.

In the past, The Trade Desk used periods of chaotic Macro to motivate more customers to modernize practices within targeting and measurement more rapidly, which is great for their business. These have been the periods where TTD had taken the most land and distanced itself from the competition. This year, for the first time since going public, it doesn't look like it will outgrow the market by more than a couple points. The market share gains are greatly slowing (almost flattening), which I find concerning. Still, they're adamant that they will revert to outsized growth even though it's very hard to tell from this quarter and forward guidance.

Generally speaking, we got the same quarterly spiel from Jeff Green about how he's more optimistic than ever, and the company's in a better position than it's ever been. They see these “Macro headwinds” as temporary, and think the structural ingredients underpinning the TTD business model are still firmly intact. Green continued to see connected TV as in its early innings with audio advertising quickly ramping, retail media also quickly ramping, and Agentic Search creating exciting new opportunities for the company (more later). All I will say is, we get these sermons each quarter, and they become much harder to get excited about every 90 days. Better results can fix that, but they’re not yet coming.

State of the Global Ad Market – Supply Side:

Green spent a lot of his time dissecting industry developments across various parts of the ecosystem, starting with the supply side. Inventory rose during 2025 at a rate faster than the company's ever seen. Titans like Netflix, choosing to greatly enhance ad load along with new partnerships with Spotify, helped create a lot more impressions for Trade Desk's buy-side clients. That naturally creates a buyer's market and allows its large brand customers to get more picky and more selective, both on impression, appeal, and price.

Trade Desk did acknowledge the fact that some publishers are looking to "wall off" their inventory and emulate the business models that made Facebook and YouTube so unbelievably successful. Perhaps that's holding back results, even though it didn't explicitly say so. Trade Desk thinks giving buyers a full view of the open market simply provides too many substitutes for this to work for anyone besides the mega-caps. That diminishes market power enough to make walled gardens unattractive for almost everyone (per TTD).

Their relationships with Netflix, Disney and NBC were all positively discussed. Green talked about TTD outperforming for NBC during this year’s Olympic games, showing that the company can scale and meet the moment with high-quality results during the most important events on the planet. This also proves again that live sporting events are a natural fit for programmatic bidding, with targeting potential even better considering interest swings in real-time with evolving scores and results.

On the audio side, their partnership with Spotify is developing very nicely. We saw the very first signs of this showing up in financials, as audio rose from 5% to 6% of total business for the first time. Jeff Green and The Trade Desk think this is the most under-monetized surface on the internet right now. They feel like they're in pole position to capture this opportunity. We’ll see.

- As an aside, the buyer’s market note should be very good for the company's business. And again, it's hard to see that playing out in its financials.

State of the Global Ad Market – Buy-Side:

When the company talks about walled garden models not making sense for anyone except a few companies, they're talking about Meta, Google, and Amazon.

Even for these titans, TTD discussed people increasingly realizing the shortcomings of their “cheap reach” and opaque reporting the 3 companies are sometimes criticized for utilizing. They think both the demand side and supply side competitors are growing increasingly critical of standard measuring practices that favor bottom-of-funnel and last touch attribution while discrediting all the work other placements did to improve customer intent enough to convert. This growing awareness, per the company, should be a tailwind for their model. It was this quarter for a leading pharmaceutical advertiser that previously left for Amazon due to the promise of cheap reach and the zero-fee tests. They boomeranged back to TTD for better returns. They’ll grow TTD spend by 114% this year as a result. Products like Audience Unlimited, which allows customers to use TTD’s scaled based on 3P data more conveniently and affordably, was an edge here. And per Jeff Green, it should be an edge elsewhere, considering TTD represents 80% of retail market share within its customer base and Amazon is around 15%.

- It’s important to note here that all 3 of those businesses are in fantastic shape and outgrowing this company despite a much larger base. So, while TTD may continue to criticize their ways of doing things… Those ways are working. But I digress.

- Green also spoke about a cohort of buyers who were looking to more rapidly modernize ad processes with TTD, like the company usually sees during turbulent times (talked about above). That cohort is just not currently large or meaningful enough to mask the ongoing deceleration in growth despite easier comps and cyclical tailwinds kicking in.

Trending to the Open Internet?

Leadership is arguing that an increasing focus on ad returns instead of ad price (related to cheap reach conversation above) is motivating many customers to seek out the open internet through Trade Desk’s platform. More and more, brands are realizing that paying more for a placement routinely makes sense thanks to superior expected value compared to a social ad that is usually viewed for a second or two. This is making them more confident in “soon” consistently getting more of the first campaign dollars vs. walled garden giants. TTD has been talking about this for a while and they’ve been disclosing the trend of more dollars going to the open internet over the closed ecosystems as if it was already in full swing. The addition of “soon” this quarter felt like a negative change in tone, but maybe I’m reading too far into things.

JBP Momentum & Publicis:

The company's pace of joint business partnership (JBP) additions continues to notably improve quarter over quarter. They grew JBP's at a 55% Y/Y clip, including 40% Y/Y growth, excluding renewals. On the other hand, this could have gotten a temporary boost from their loud and public battles with a large agency called Publicis. As previously covered, Publicis accused Trade Desk of some pretty shady practices in terms of fee structures, and communication of those fee structures. They no longer recommend TTD to their clients, which could have pushed more of them to embrace a direct relationship with the company through JBP’s. On the bright side, that means these companies are still determined to work with TTD, despite their agency telling them not to. At the same time, this probably is a reason why growth here is so impressive.

Speaking of Publicis, Green acknowledged that the relationship remains good and dialogue between the two companies is ongoing. He hopes that the drama will be soon behind them, and thinks the media ran with the story in sensationalistic ways that didn't truly reflect how things were evolving. They had nothing more to say about this on the call when asked.

AI:

The Trade Desk is partnering with Stagwell to infuse agentic technology into ad campaigns and impression trading. This will start with automating “creation, editing and modification of campaigns,” with phase two including agentic-inspired performance optimizations. The team elaborated on the sheer number of potential campaign optimizations, overwhelming customers, and routinely fostering more complexity than value. Unlocking conversational querying of recommendations and actionable ways to deploy those data-driven recommendations should be very powerful. The company needs to work very hard on rapidly innovating as times evolve at an especially torrid pace. They do not own impressions thanks to a scaled base of customer traffic they directly house. They are in the business of convincing customers they need TTD to buy those impressions in the best way possible. There is a boatload of agentic innovation and potential disruption happening in this specific area, and TTD must use its enterprise-facing scale, talent and balance sheet to fend off these competitors and/or homegrown solutions. Partnerships like these can help.

AI Creating New Opportunities:

Search is changing. And while Alphabet will probably continue to have a dominant portion of whatever it turns into, there are other scaled alternatives emerging that are more open to working with companies like The Trade Desk. More specific prompt inputs should allow the company to understand intent and interests in a far more precise way, easily matching customers with products they want. Because there are several other LLMs vying for market share, and because they are spending so much on scaling operations, TTD is confident that they must monetize with ads. They're optimistic about capturing a lot of those deals, and should have more to share with us in this regard in the future.

Supply Side Entry?

OpenTTD is their new “central hub” of information that openly integrates with other platforms and customers. It unifies data analytics and makes it easier (on top of OpenPath) for publishers to access what they need directly from Trade Desk. The company was very intentional to again mention that they will not get into the business of yield management for publishers. That is what the supply side does, and it would create a conflict of interest if Trade Desk did that, while they were trying to optimize return on ad spend for buyers. You cannot optimize for the same thing at the same time. On the other hand, they will make it increasingly seamless for publishers that want to perform their own sell-side tasks to access this platform and rich base of information on their own. Other products like OpenAds, which provide a cleaner environment for impression auctioning without as much supply chain mess is another product that should help.

More Notes:

- Chief Strategy Officer Sam Jacobson is leaving for OpenAI. She’ll remain a board member. Yet another executive is leaving the company.

- The company is beginning to add brick-and-mortar retail media business as it starts to become more omni-channel in nature for customers like Dollar General. An ability to target shoppers in-store is interesting. They can theoretically use geofencing to know who is entering a store and what promotion they might want.

- Partnered with LinkedIn to “activate their B2B data for connected TV (CTV) monetization.”

g. Take

Time to be blunt. This company is not executing. Their excuses (over the last 6 quarters now) don't make nearly enough sense to make underwhelming performance permissible. I will continue to closely track this organization because they were so consistently impressive for well over a decade. I will do so with the hope that they'll regain their mojo and show people all the value they provide in the massive open internet advertising market. I will not restart a position in this company until all of those things become a lot more clear, and there's no guarantee that that will ever happen. For now, I sit on the sidelines and demand that this company shows many more signs of having brighter days ahead. The fact that they cannot accelerate revenue growth in a year where comps get far easier and a midterm election happens is concerning. It's emblematic of a growth engine in permanent decline, and one deserving of all the multiple contraction it has endured over the last two years.

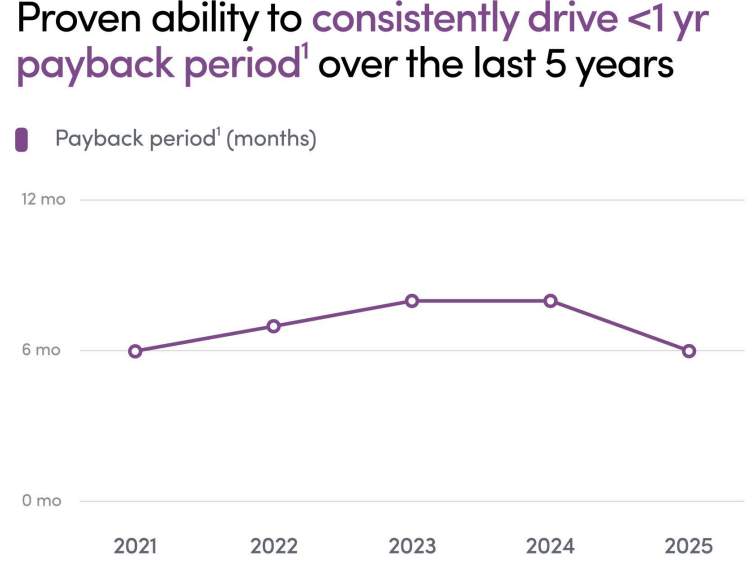

2. Hims (HIMS) – Q1 2026 Earnings Review

Hims sells men’s and women’s health products with a direct-to-consumer business model. It allows users to more comfortably access sensitive prescriptions within areas like erectile dysfunction or hair loss, without going to an office or a pharmacy. Products are mailed right to a consumer’s door.

It offers standard and personalized medicine and subscriptions. Personalization is enabled & amplified by its Electronic Medical Record (EMR) system. From its early days, Hims built this EMR foundation to enable scalable data ingestion, automate tedious provider work and foster rapid product expansion. That remains absolutely vital in the firm’s future. It paved the way for MedMatch, which is the company’s tool that uses all customer interactions and data to uncover valuable consumer insight and nudge best provider practices. It also enabled Clever Routing, which contextualizes individual user needs to prioritize and match demand with proper levels of care.

a. Key Points

- Several headwinds weighing on margins.

- Slightly weak Q1 revenue number but, more importantly, strong full-year revenue forecast.

- No longer marketing personalized, non-branded GLP-1 products.

b. Demand

- Missed revenue estimate by 1.4% & missed guidance by 0.8%.

- Zava and Livewell acquisitions are currently leading to explosive and inorganic international growth.

- Met subscriber estimates and met revenue per subscriber estimates.

- Net new subscribers fell by about 50% Y/Y.

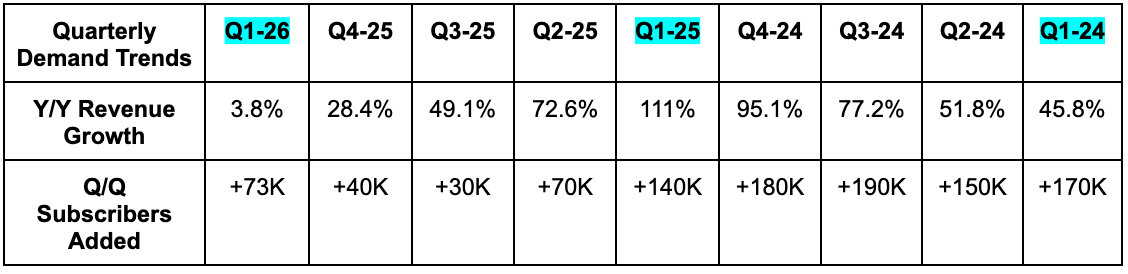

As guided to, a shift from bulk to monthly GLP-1 customer shipments is weighing on revenue growth at the moment. This decision is being called a strategic shift, but it can likely also be seen as a response to broader regulatory crackdowns. It’s a timing issue where instead of collecting revenue upfront for a lot more doses, that revenue recognition is spaced out over multiple quarters. While that held back results, the headwind was already baked into guidance and they still slightly missed their forecast. Furthermore, their March GLP-1 pivot meant halting the marketing of their personalized GLP-1 offerings and leaning into branded offerings like Wegovy. This quelled serious legal concerns and (in my opinion) was the right decision for the company. It turned Novo Nordisk and other GLP-1 makers from foes into paranoid friends. Still, the change comes with a negative as well. HIMS was able to undercut competitors with the non-branded offering. It no longer has that edge, which erodes differentiation in a crowded market and likely weighed on demand at least a little bit.

c. Profits & Margins

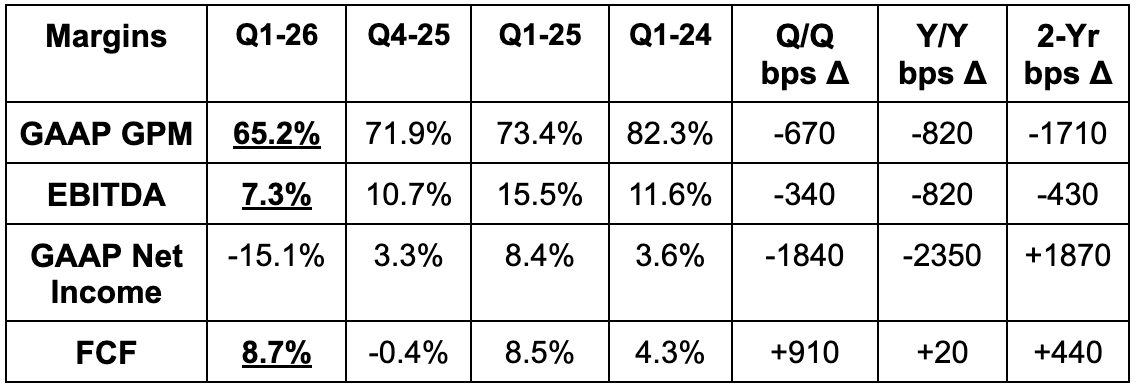

- Missed EBITDA estimate by 2.4% & missed guidance by 1.6%.

- Missed $4M GAAP EBIT estimate by $82M or by $54M ex-legal & M&A.

- Missed $0.13 EPS estimate by $0.32. Some services had consensus estimates at $0.02 instead of $0.13.

- Beat -$5M FCF estimates by $58M.

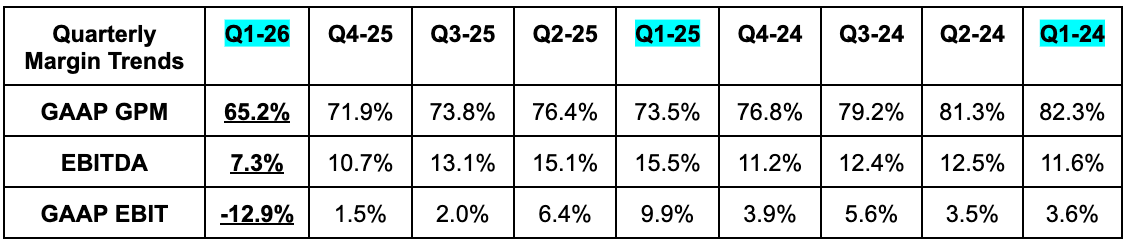

Going back to their March GLP-1 pivot for a moment, this weighed heavily on margins. The shipments of smaller doses of branded GLP-1 drugs is now lower margin than the bulk personalized shipments HIMS had been doing. Furthermore, they took a $28M input cost restructuring charge that lowered GPM by a full 5 points during the quarter. Another $5M in charges hit EBIT and net income margins by another point (EBITDA is non-GAAP and unaffected). Still, 3 points of GPM contraction and significant deleveraging further down the income statement, but not nearly as bad with this in mind. That was great to hear, but leadership also said GPM could worsen by a couple points from the 65% level over the next quarter or two, so the pressures will remain in place for now. It sounds like they might be taking more inventory charges next quarter, but they didn’t explicitly say so. For net income, legal and M&A-related charges lowered that metric by another $28M during the quarter. For these reasons, adjusted EPS (which I use above) is a better metric this quarter.

As you can see, while there are significant non-structural items impacting margins, things are still worse than expected for both EBITDA and especially EPS. That’s likely related to a combination of these items being larger than analysts modeled and several investment areas the company is aggressively pursuing. These include AI, manufacturing capacity expansion, new categories like peptides, global expansion and general R&D (including hiring). They expect all of these investments to drive enough incremental demand and long-term efficiency gains (this specific cost growth won’t be perpetual) to start helping margins next year. Their priority right now is taking more market share in existing areas and rapidly scaling into new products with their vertically integrated production facilities.

d. Balance Sheet

- $750M cash & equivalents.

- $974M senior notes.

- 2.8% basic share dilution. Diluted share count down Y/Y.

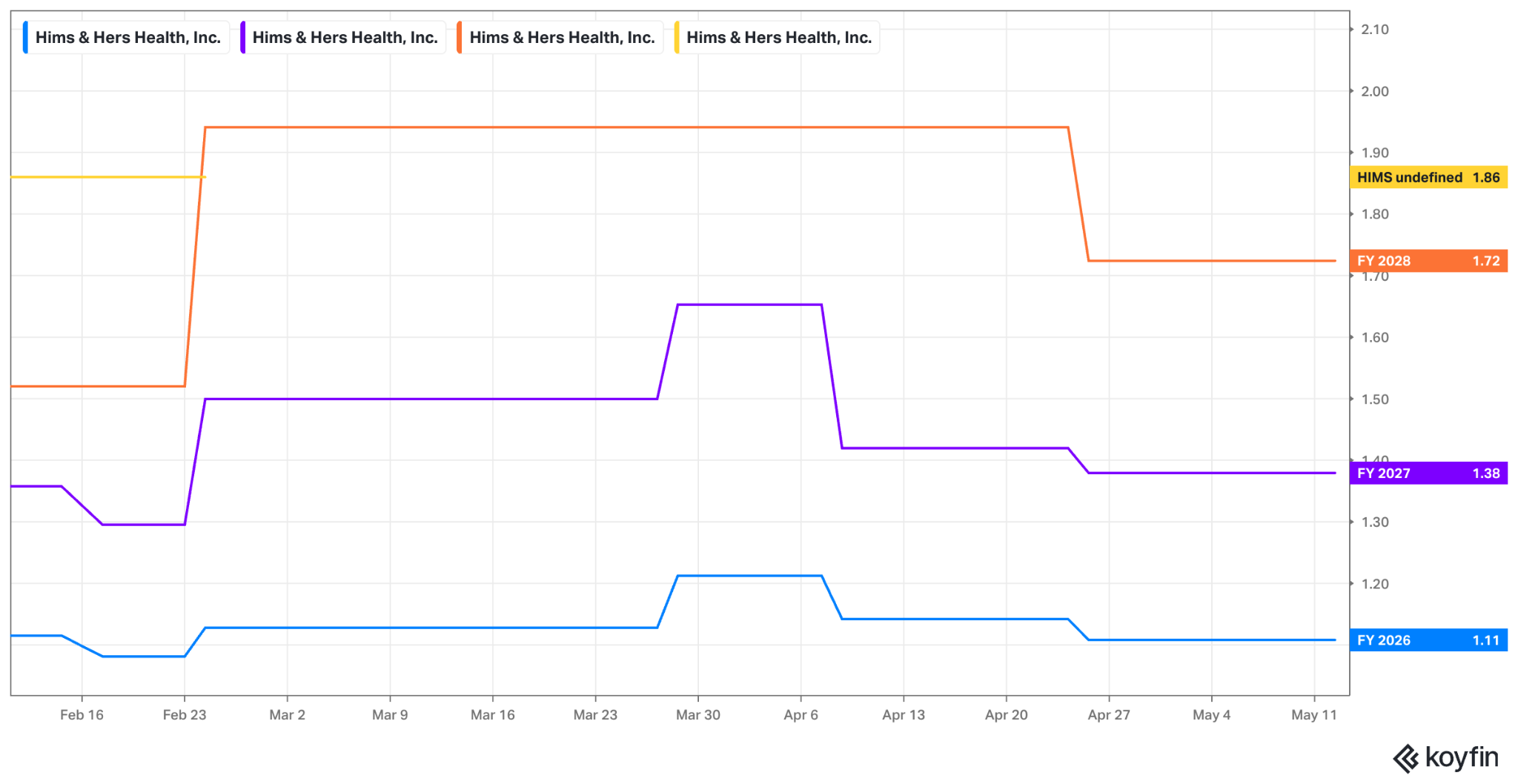

e. Guidance & Valuation

Annual:

- Raised annual revenue guidance by 3.5%, which beat by 6.6%.

- Lowered annual EBITDA guidance by 7.4%, which missed by 5.0%.

Q2:

- Revenue guidance beat estimates by 7%.

- EBITDA guidance missed estimates by 36%.

More guidance context:

- Guidance still does not include Eucalyptus M&A (for international expansion).

- GPM will continue to compress as all of these investments and near-term GLP-1 headwinds rage on.

- EBITDA growth should meaningfully improve for Q3 and Q4 thanks to expected marketing efficiencies and more fixed cost leverage from accelerating revenue growth and moving beyond temporary expenses like the inventory charge.

- Despite all of the margin challenges, they reiterated 2030 targets calling for $6.5B+ in revenue and $1.3B in EBITDA.

- They expect to return to positive GAAP net income in 2027.

- When asked if they could get back to a 75% GPM, they turned the conversation to focusing on EBITDA dollar growth. In other words, probably not.

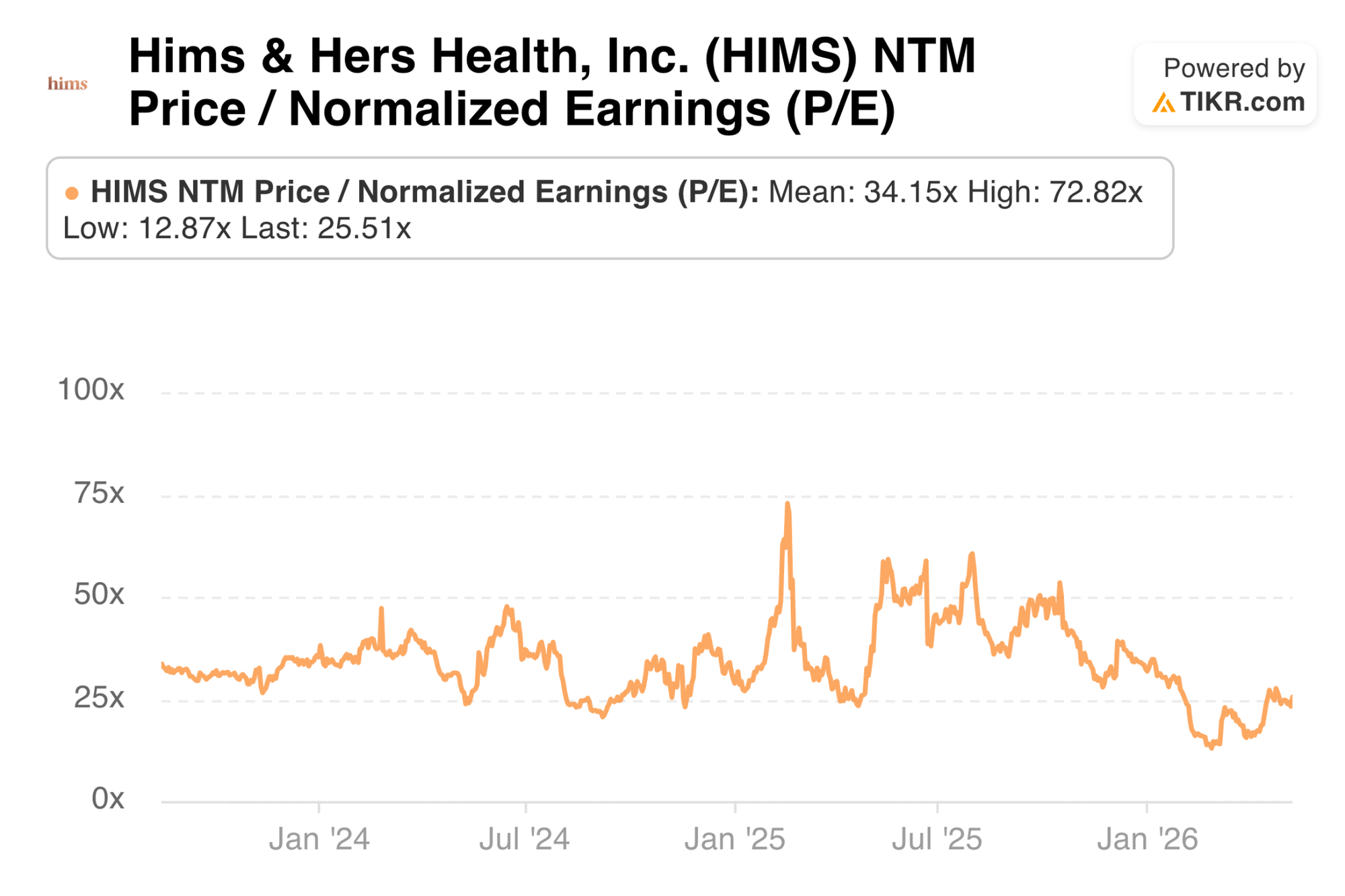

HIMS trades for 25x forward EPS. EPS is expected to grow by 1% this year and by 24% next year. There will be negative revisions following this report.

f. Call & Release

GLP-1 Business:

While the altered GLP business is lower margin and less differentiated, it still provides a lot of value and is doing well. Their Novo Nordisk offering is up to 125,000 prescriptions and netting 100,000 new high-engagement subscribers per month. This business isn’t turning into a loss leader, but it is turning into a less profitable revenue generator. Getting these people in the ecosystem will mean more cross-selling to higher-profit offerings.

Pursuit of Proactive & Preventative Care:

HIMS is pushing hard to evolve into an end-to-end source that focuses not just on addressing symptoms, but finding issues faster. This holistic care vision would naturally create longer-term subscriber relationships and enhance lifetime value. It would also make HIMS a better company in terms of driving more compelling patient outcomes.

Investments like their YourBio purchase to vertically integrate “painless” blood draw from home will be highly important tools in bringing this all to life. This will greatly reduce friction, nuisance and cost associated with highly accessible blood tests and help customers take more control of their health. Knowledge is power, and this will mean more patients having better knowledge faster. For HIMS, that helps support launches in categories like its testosterone offering, where blood testing has already netted tens of thousands of new customer relationships with strong positive outcome rates.

The company is modernizing their operating system with this strategy in mind. They are building a revamped platform that “supports great complexity” and better grasps the vast number of data points, health attributes and interactions each individual customer features. This is an important piece of walking before they can run by ensuring their platform is ready for this more intricate go-to-market. Importantly, this operating system is also being built for malleability and scalability. It features a Lego-like, no-code design that allows for seamless design updates, product introduction and other changes without disruption. That will be imperative for enabling further category expansion without crippling user experience or other bottlenecks.

Data:

The item bringing everything you just read above to life is data. Data is personalization. Data is better recommendations. Data is more cross-selling. Data is the lifeblood of this business. With HIMS’ scale comes an abundant flow of information that it’s determined to leverage. In doing so they spin a compelling flywheel where each new customer means more information to train algorithms, more personalization, better experiences and eventually more customers to spin this round and round. An eventual entry into wearables should be incremental to this data trove as well.

AI will unsurprisingly be the most valuable player for extracting value from data. MedMatch is a good early example of this coming to life, but their vision extends far beyond it. They plan to get to the point of an army of agents working to support tedious provider tasks and more effectively nudge best practices and adherence for consumers. Early products on their way to achieving their ambitions include their provider Copilot and a Labs AI offering that simply explains biomarker results. They have a consumer-facing agentic weight loss companion in the works as well.

Peptides:

This July, the FDA will meet to determine whether peptides can be legally made and removed from the “prohibited from compounding” list. HIMS is excited about this, but was careful to say it likely won’t be a first mover. It wants to go slowly, make sure all regulatory stakeholders are taken care of and be the “best mover.” They know they have the brand, customer base and vertically integrated manufacturing capabilities to foster great experiences and a successful launch. Perhaps learning from GLP-1 headaches, it knows doing this right is worth modest delays. The company aims to rely heavily on provider recommendations and the highest quality ingredients to appease regulators and position this for sustainable success.

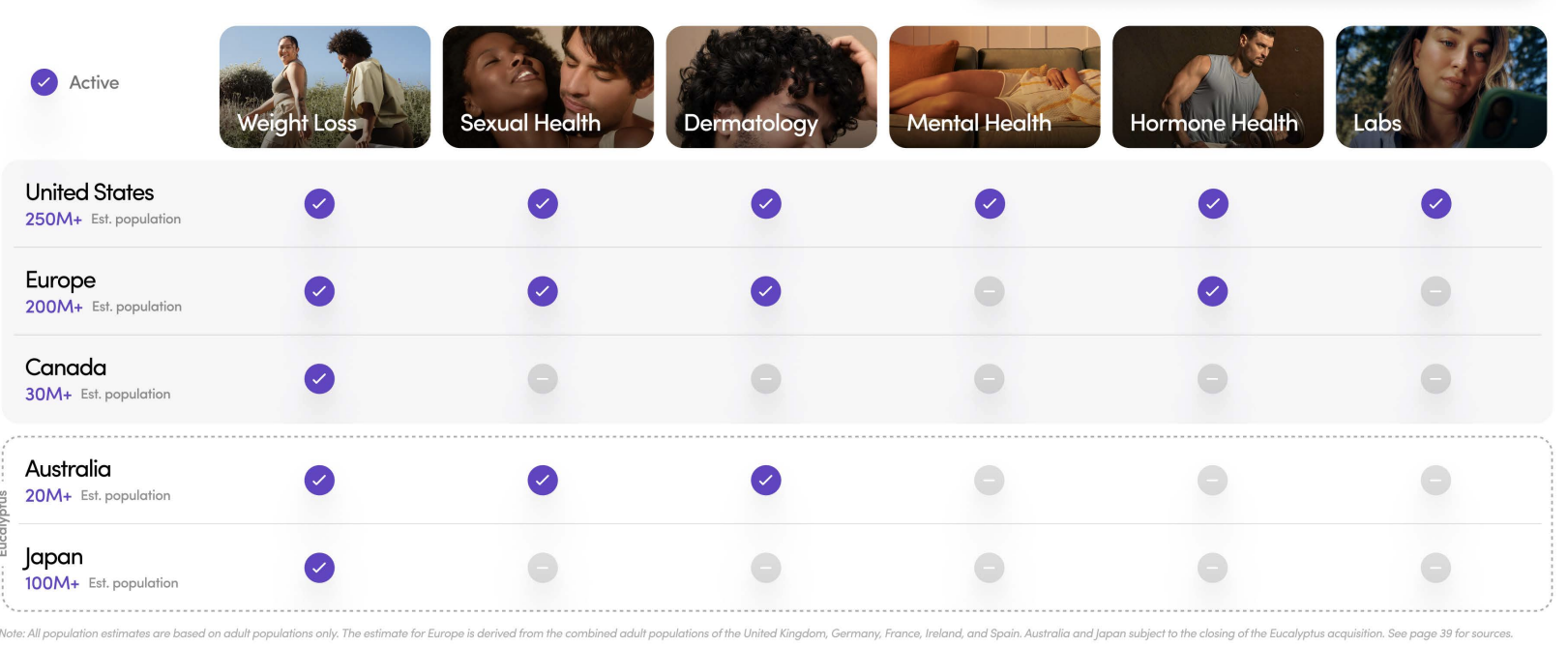

Global Expansion:

- They still expect Eucalyptus to close during the second half of the year. This will entail a $240M cash outlay upon closing, with more payments coming over time as milestones are reached.

- They think they’ll continue attracting high-quality global partners due to their strong outcome impacts and global supply chains.

g. Take

Very noisy quarter. There are some structural margin headwinds that will continue going forward (like the branded GLP-1 shift). At the same time, there are temporary headwinds making the margin contraction look even worse, and amplifying the weakness we're currently seeing. From a demand perspective, trends look quite good, and their entry into peptides, hormone treatment, at-home blood tests, and more categories should provide growth outlets to keep expanding in the coming years. I think their GLP-1 pivot is the right decision, and taking their medicine here will prove to be a good strategic shift in hindsight. It takes a lot of legal pressure off the table, and turns very rich and very powerful enemies back into partners.

I think their focus on personalization is the right one, although I do question how big of a moat that truly builds. Other companies, especially cloud titans like Amazon, are capable of data analytics too. And when competitors like that one are increasingly focused on winning in this specific area, they can lean into operating at razor-thin margins, with world-class fulfillment, instead of needing to win on personalization. That makes me a bit nervous. Longtime subscribers know that I've been a skeptic of this name for a while, but the multiple has come in a ton in recent quarters, and that's led me to move my stance from bearish to more neutral. That's about where I stand right now. It's not my favorite investment, but I don't really think the risk/reward is nearly as unfavorable as it has been in recent years.