Other reviews from this season to read:

- Mercado Libre & Datadog

- AMD & Uber

- Axon

- SoFi

- Amazon

- Duolingo

- Meta

- Lemonade

- Robinhood

- Alphabet

- Shopify & Coupang

- ServiceNow

- Apple

- Spotify

- Palantir

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

1. AppLovin (APP) – Q1 2026 Earnings Review

AppLovin is an advertising technology company. It operates a two-sided marketplace with the aim of optimally matching demand with the optimal placement for everyone involved. Inventory spans across gaming and now consumer verticals like e-commerce. Axon 2.0 is the name of its AI-powered ad auctioning engine that powers its demand-side platform (DSP) called AppDiscovery. This platform is meant to granularly quantify ad impression value for each specific investor, helping them find the perfect placement.

Max is used on the supply-side for publishers to auction their opportunities to an aggregated base of demand. The company used to operate a gaming studio where they developed and provided games to customers, but they sold that business last year to exclusively focus on advertising.

Other products to know:

- Axon 2.0 is the technology behind its ads platform.

- Adjust is their measurement and attribution tool that allows stakeholders to understand how placements performed.

- Wurl is their ad platform retrofitted and purpose-built for connected TV (CTV).

a. Key Points

- The non-gaming ad business is scaling nicely.

- Margins continue to move from elite to more elite.

- On track to debut their highly anticipated self-serve platform in a couple weeks.

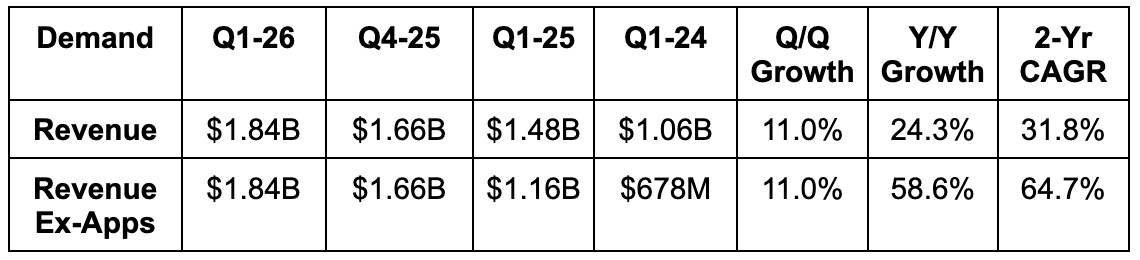

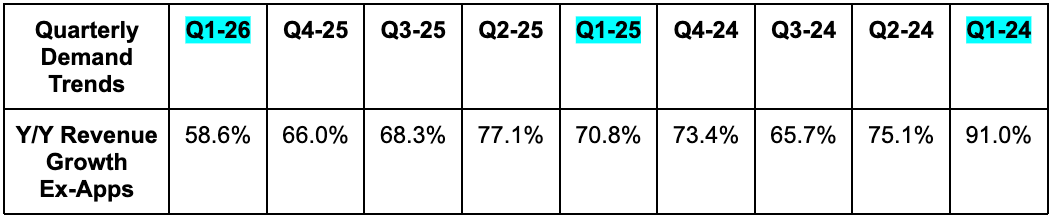

b. Demand

APP beat revenue estimates by 4% & beat guidance by 4.9%.

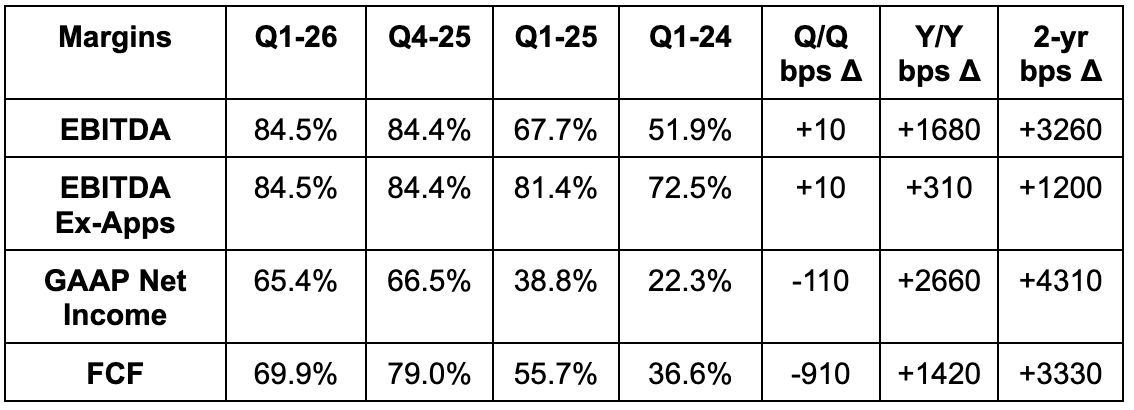

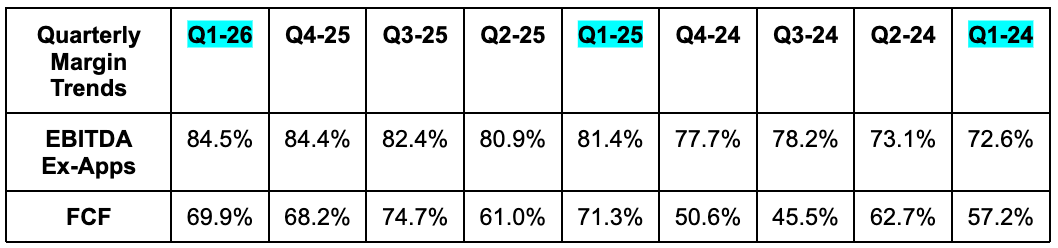

c. Profits & Margins

- Beat EBITDA estimate by 4.4% & beat guide by 5.2%.

- Beat FCF estimate by 12%.

- Beat $3.46 GAAP EPS estimate by $0.10.

d. Balance Sheet

- $2.76B cash & equivalents.

- $288M equity investments.

- $3.51B debt.

- Diluted share count fell by 0.7% Y/Y.

e. Guidance & Valuation

- Revenue guidance beat estimates by 2.1%.

- EBITDA guidance beat estimates by 2.5%.

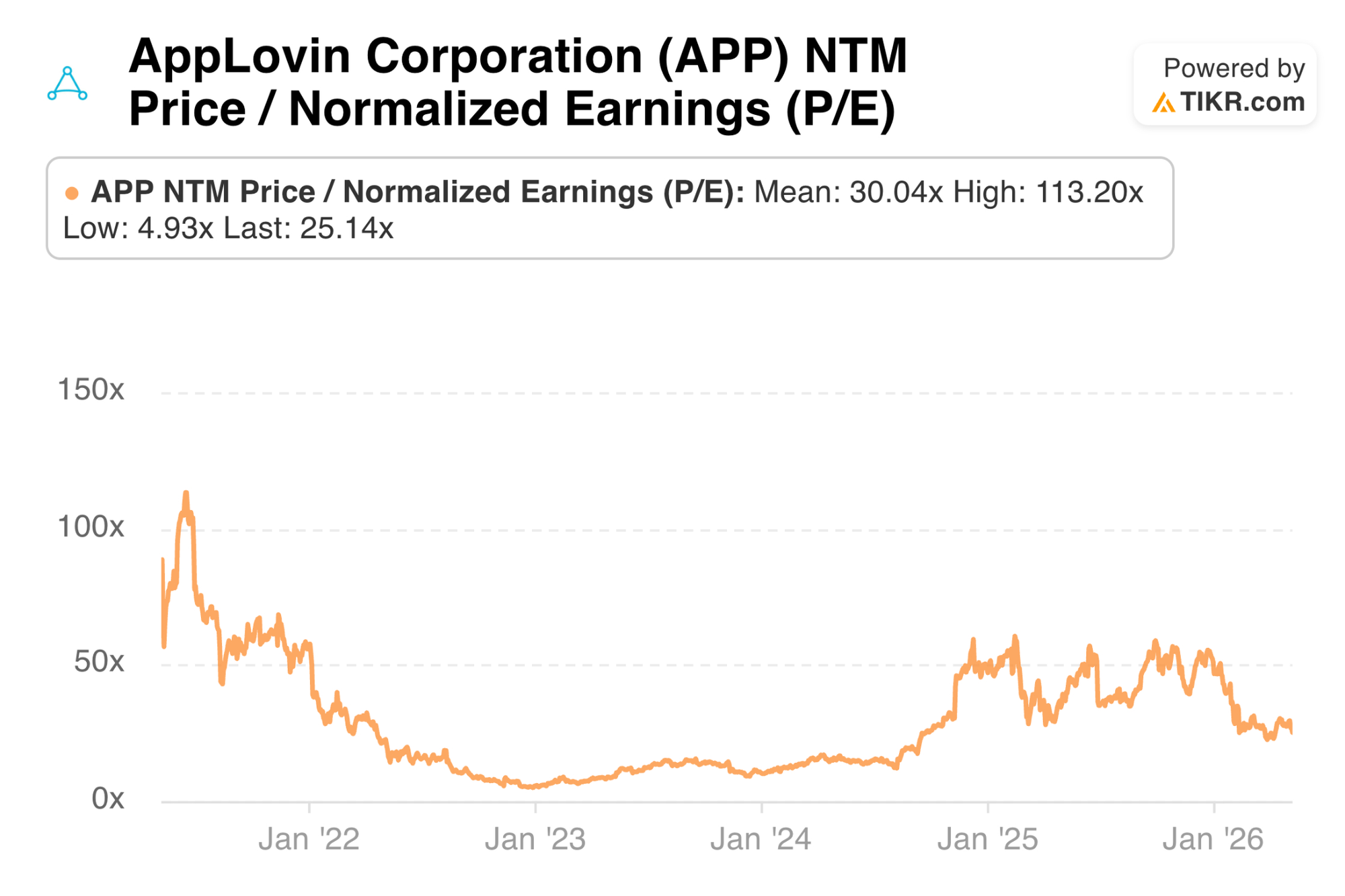

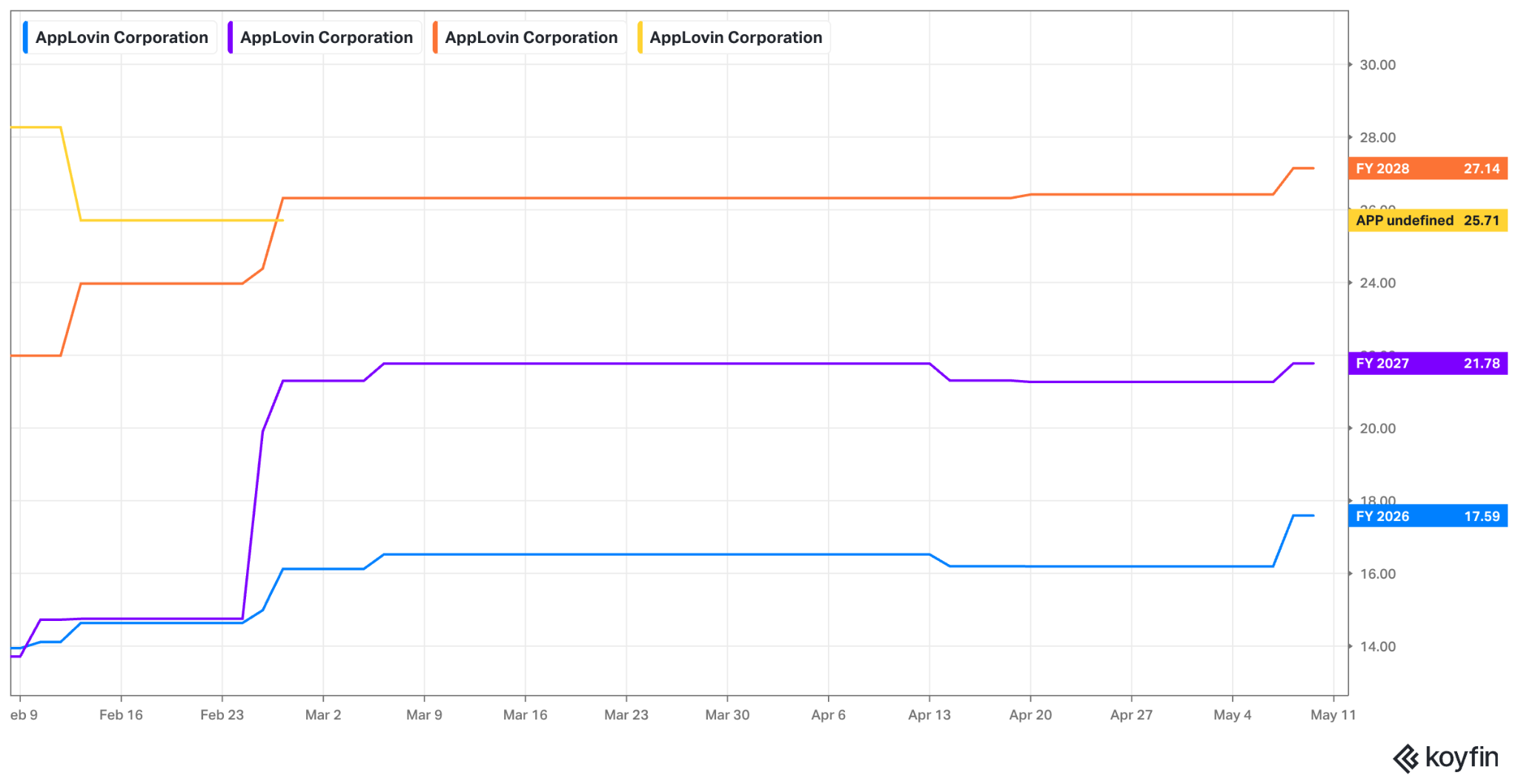

APP trades for 18x sales, but just 25x EPS due to the incredible margins. EPS is expected to grow by 65% this year and by 24% next year.

f. Call & Release

Platform Opening:

AppLovin has been gearing up for its Axon Ad Platform/Manager to unlock self-serve access, rather than solely direct company management. This should be especially great for enabling APP to access demand from the long tail of smaller advertisers without needing to dedicate expensive resources to them. Importantly, the platform will also be open in the sense that customers can manage their APP campaigns with whatever model and agent they want to use.

With less support comes the need for better tools so that these advertisers can still realize the kind of successful outcomes APP delivers to managed clients. Its AI-powered Video Generation tool is a good example of this. It will debut in the coming days as a way for advertisers across many verticals to automate fitting their existing product listings, marketing content and other materials for APP placements. This, using Axon 2.0, will be done in ways to optimize return on ad spend (ROAS) and remove the friction that companies (especially non-gaming customers) experience with fitting the right format into the right impression.

Core Gaming Ads Business:

There are a few tailwinds that continue to drive excellent core business growth. AI content creation tools are allowing developers to ship more quickly and cheaply, meaning more supply for APP to monetize. They’re not overly bullish on the massive influx in new apps to the app stores, as they think most are low-quality “slop.” But they are excited about some world-class developers getting their hands on better tools to drive this expected tailwind.

Next, there is ongoing momentum to embrace more ad-based monetization sources among the large batch of established game publishers that only monetize via in-app purchases. Leadership excitedly spoke about creators increasingly focused on embracing hybrid business models, knowing most are capped at 10% of total customers who will purchase things in-app. Why not monetize the other 90% as well? They now increasingly are – with APP by their side. A lot of this change has to do with APP broadening the type of advertisers it services. In its earlier days, a lot of the ad demand for its gaming publisher clients was from their direct competitors. Now, APP has a much broader set of ad-buyers from different sectors, making the game makers much more comfortable with an ad business (without supporting their foes).

- APP still feels like the inventory across the 1.4B active users its publishing clients represent is significantly under-monetized. Ongoing business shifts described above and general ad load increases will close this gap over time and provide a steady source of growth while that happens.

Budding Consumer Ads Segment:

Going back to non-gaming ad-buying customers, APP continues to leverage growing scale and experience to make steady model improvements and drive better results. Over the last quarter, these improvements led to a 1.3% boost in ad conversion rates, and the expectation is for a steady stream of updates that will foster more advancements in targeting and measurement over time. They’ve run the same playbook on the gaming side of the business quite well, and are confident those learnings can be extrapolated and applied for e-commerce, fintech, food delivery and other customer types as well. They’re building out important lead generation capabilities to better serve these types of customers that rely on this type of key performance indicator for success.

As an aside, I’m a fan of the small, frequent iteration approach to their product offering. Competitors like Trade Desk have gotten into trouble by relying too heavily on big annual launches where so much time and effort was spent before actually learning from customer reactions. APP’s strategy (which Trade Desk now more closely matches) not only means customers enjoy faster access to upgrades but less risk tied to each of those upgrades. And this seems to be working well. March traffic was up 25% compared to January, while April traffic reached a new company record, which is notable considering Q4 is seasonally their strongest period.

- It’s worth noting here that Axon 2.0 is a great enabler of all this productive change, and (per the team) has been the driving force behind APP’s sharp multi-year acceleration since it debuted in 2023.

Importantly, APP is not seeing growth from non-gaming ad-buyers crowding out demand from gaming ad-buyers. As they explained it, the inventory they’re offering to this newer source of demand was not well suited for gaming customers and instead represented excess space to monetize.

Impressive Marketing Efficiency:

APP continues to enjoy a sub-30 day payback period for its own performance marketing. Furthermore, the vast majority of these new customers continue to spend well beyond that 30-day window, immediately delivering $70K+ in annualized value.

Connected TV:

There has not been much time spent on this side of the business over the last couple of quarters. That’s not because they’re souring on the opportunity. It’s not because they are failing on product design. It’s because the consumer ads side of the business has turned into such a massive opportunity that they’ve decided to prioritize it over this for the time being.

Expenses:

While APP plans to continue spending on GPUs and other assets to support customer scaling, they do not expect margin compression from here. They expect their best-in-class margin profile to stay that way, as a combination of rapid growth, headcount control and other OpEx leverage help keep margins at least stable from here.