Other reviews from this season to read:

- Mercado Libre & Datadog

- AMD & Uber

- Axon

- SoFi

- Amazon

- AppLovin & Cloudflare

- Duolingo

- Meta

- Lemonade

- Robinhood

- Hims & The Trade Desk

- Alphabet

- Shopify & Coupang

- ServiceNow

- Apple

- Spotify

- Palantir

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

Table of Contents

On Running is a premium athletic shoe and clothing company quickly gaining ground against Nike and Adidas. They have several popular running shoe products, with 8 of them contributing at least 5% of overall revenue. This is not a one-trick pony. In terms of sports, they’re popular for runners and tennis players, with expansion into more activities going well. It’s founder-led, with a focus on operational excellence and creating the next trending category through impactful, focused innovation – like LightSpray. As a reminder, LightSpray is On Running’s new automated manufacturing technique. It uses robotic arms to (as the name indicates) spray a light material right onto the sole of the shoe to form a single-piece, laceless model. Impressively, it takes a robot 3 minutes to make a shoe and is comparatively quite cheap. That combination should be fantastic for On’s long-term margin ceiling.

a. Key Points

- Strong quarter for brand building.

- Healthy traction with younger customers.

- Record margins despite tariffs.

- Strong growth despite the strict dedication to only quality revenue opportunities.

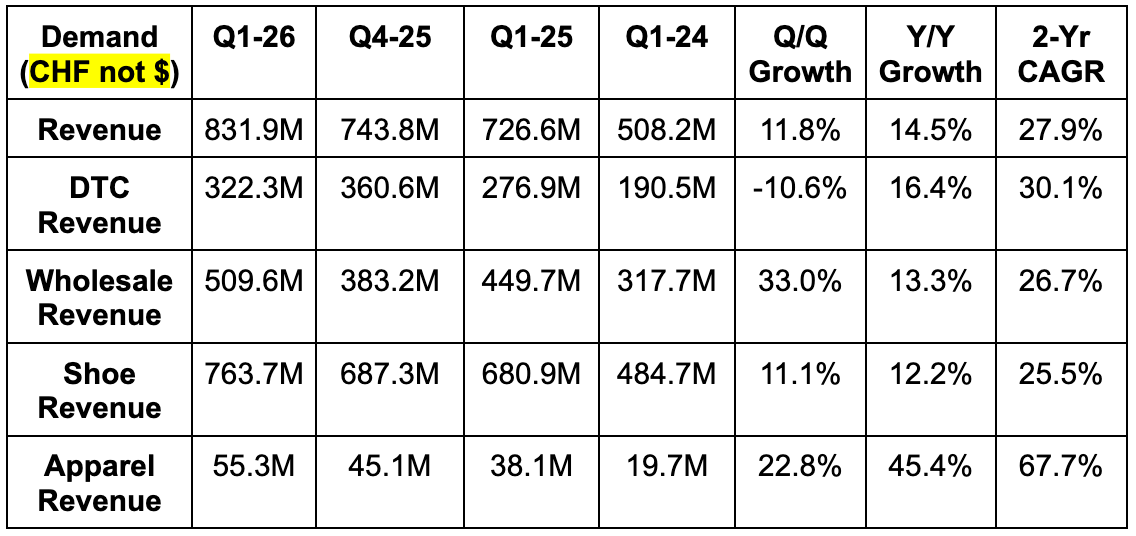

b. Demand

- Beat revenue estimates by 1%.

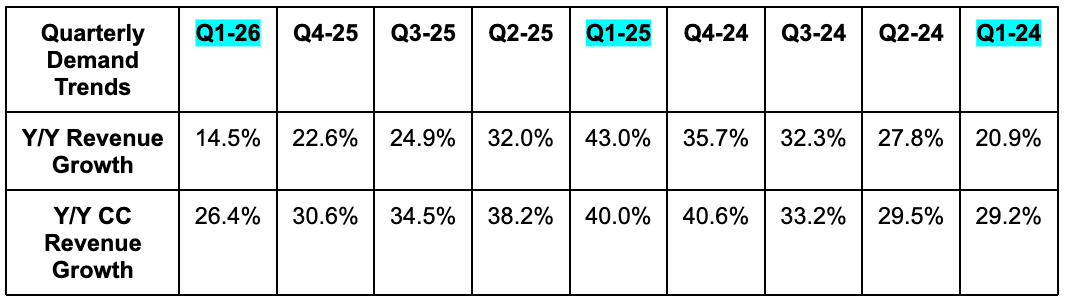

- Europe, Middle East & Africa (EMEA) growth was held back a bit by war.

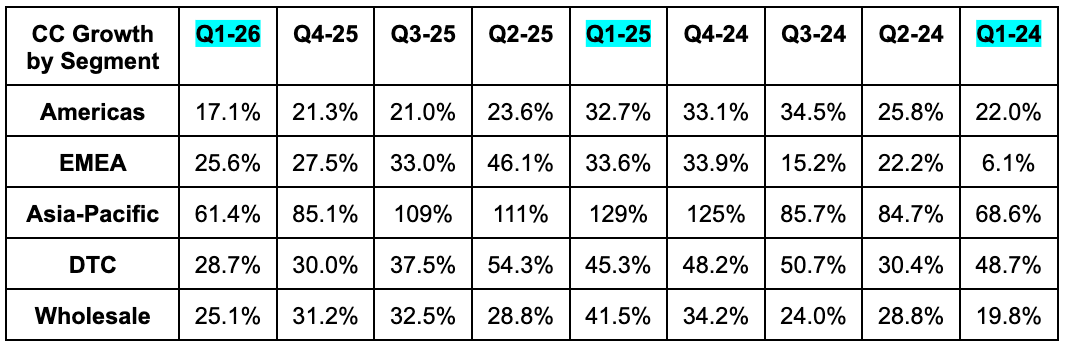

- Korea was cited as a country standout this quarter, with 200%+ Y/Y growth and fantastic success across existing stores.

- Beat wholesale revenue estimates by 2%.

- Direct-to-consumer (DTC) revenue slightly missed estimates.

c. Profits & Margins

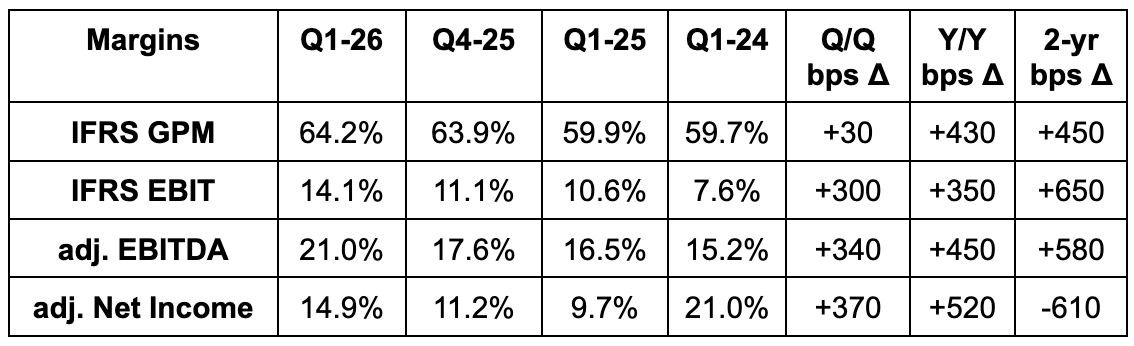

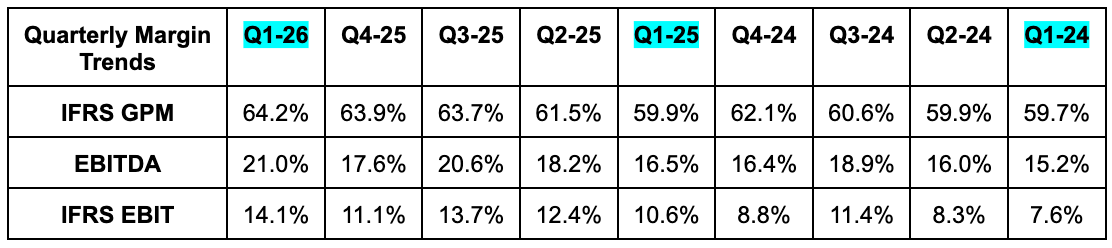

- Beat 61.4% GPM estimate by 280 basis points (bps; 1 basis point = 0.01%).

- The sharp Y/Y GPM expansion was despite an incrementally larger tariff impact during the quarter.

- The mix-shift to DTC sales and full-price strength helped more than offset tariff headwinds.

- Beat EBITDA estimate by 22%.

- They continue to aggressively invest in brand-building, LightSpray and other innovation.

- Beat 0.27 CHF (Swiss Francs) EPS estimate by 0.10 CHF.

- FX drives big quarterly net income swings. EBIT is a better metric here. FX lowered net income by $0.3M vs. $14.5M Y/Y.

d. Balance Sheet

Subscribe below to read about ONON's Balance Sheet, guidance, valuation, the details of its investor materials published tonight and my take on the quarter and company.

Upcoming reviews include Sea Limited, Nu Bank, Snowflake, Zscaler, Nvidia and so many others. This is where investors (including Fortune 500 executives) come for signal over noise and to invest with good reason.