Other reviews from this season to read:

- Nu

- Mercado Libre & Datadog

- AMD & Uber

- Axon

- SoFi

- Amazon

- On Holding

- AppLovin & Cloudflare

- Duolingo

- Meta

- Lemonade

- Robinhood

- Hims & The Trade Desk

- Alphabet

- Sea Limited

- Shopify & Coupang

- ServiceNow

- Apple

- Spotify

- Palantir

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

Table of Contents

a. Key Points

- The U.S. recovery is in full swing.

- Margins rose Y/Y with some help from temporary items.

- The loyalty program outperformed seasonal trends.

- Raised annual comp store sales (CSS) growth guidance.

b. Demand

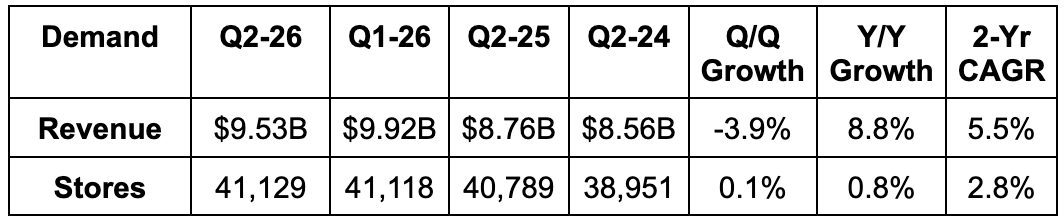

- Revenue beat estimates by 4.3%. Foreign Exchange Neutral (FXN) revenue growth was 8% Y/Y.

- North American revenue beat by 3.5%. North American licensed revenues were flat Y/Y due to some store closures. Airport, retail and grocery store strength helped offset this.

- International revenue beat by 2.7%.

- Channel development revenue beat by 21.5%.

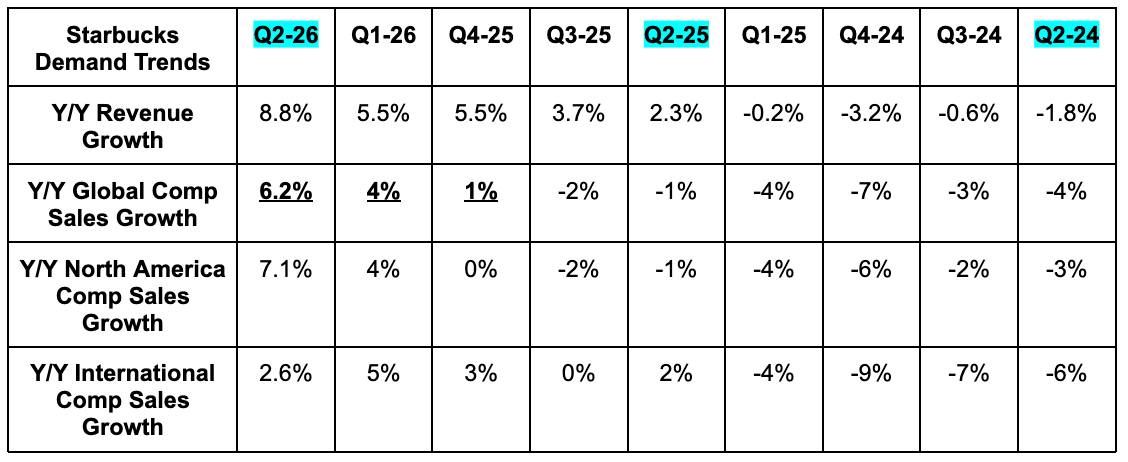

- 6.2% comp store sales (CSS) growth beat 3.7% estimates.

- 7.1% U.S. CSS growth beat 3.7% estimates.

- 2.6% International CSS growth missed 3% estimates.

More Y/Y Comp Store Sales (CSS) Growth Data:

- Within global CSS growth:

- Transactions rose by 3.8% compared to 1% last quarter and -2% the quarter before.

- Ticket size rose by 2.3% compared to 1% growth last quarter and 0% the quarter before.

- Within North American CSS growth:

- Transactions rose by 4.4% compared to 3% growth last quarter and -1% the quarter before.

- Ticket size rose by 2.7% compared to 2% growth last quarter and 1% the quarter before.

- USA CSS growth was 7.1% thanks to 4.3% transaction growth and 2.7% ticket size growth. This was a 3-year record for transaction growth, and included growth across all day-parts, income cohorts and ages. USA delivery revenue is also up 30% Y/Y so far this year.

- Within International CSS growth:

- Transactions rose by 2.1% compared to 3% growth last quarter and 6% the quarter before.

- Ticket size rose by 0.5% compared to 2% growth last quarter and -3% the quarter before.

- China CSS growth was 0.5% Y/Y, compared to 3% growth last quarter and 2% the quarter before. This was its 4th straight quarter of positive CSS growth.

- 10/10 of their largest markets delivered positive CSS growth for the first time in over two years.

c. Profits & Margins

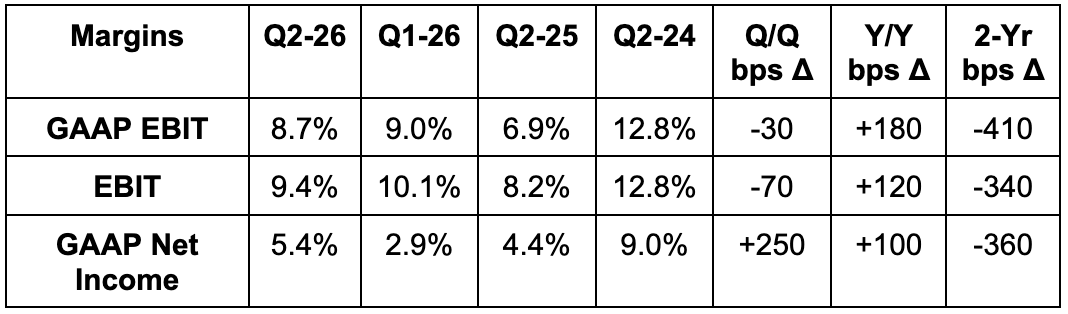

EBIT leverage was materially boosted by the China Joint Venture (JV) deal closing. That paired with easier comps enabled Y/Y EBIT margin expansion, while outperforming CSS growth and ongoing cost control efforts also helped. It was a mix of structural factors and one-offs. For context, its international EBIT margin rose by roughly 8 points Y/Y to over 20%. Half of that expansion was thanks to the China JV-related accounting change and half was related to more permanent factors. EBIT margin is fully expected to keep rising over time, as leadership laid out earlier in the year at their investor day. At the same time, that path won’t be linear and this might create some very short-term noise. North American EBIT margin, fell by 170 basis points Y/Y to 10.2% due to ongoing investments in the (clearly working) Back-to-Starbucks turnaround plan. Furthermore, 190 bps of added distribution costs from product innovation, inflation and tariffs amplified the margin pressures. This explains the entirety of the annual margin degradation, and these tariff and inflation items are expected to ease for the rest of the year, which will obviously be a positive.

So… to summarize. Margins are beginning to move in the right direction. International margins got an accounting-related boost that created a non-recurring progress sugar high. North American margins were held back by items that will fade throughout the rest of the year.

- EPS rose by 22% Y/Y and GAAP EPS rose by 32% Y/Y. This was its first quarter of positive Y/Y EPS growth in 2+ years and came despite a 29.8% tax rate compared to 23.5% Y/Y (related to China deal closing).

d. Balance Sheet

- The 60% China sale includes $3.1B in cash proceeds. They will use this to reduce debt and for “ongoing balance sheet management.”

e. Guidance & Valuation

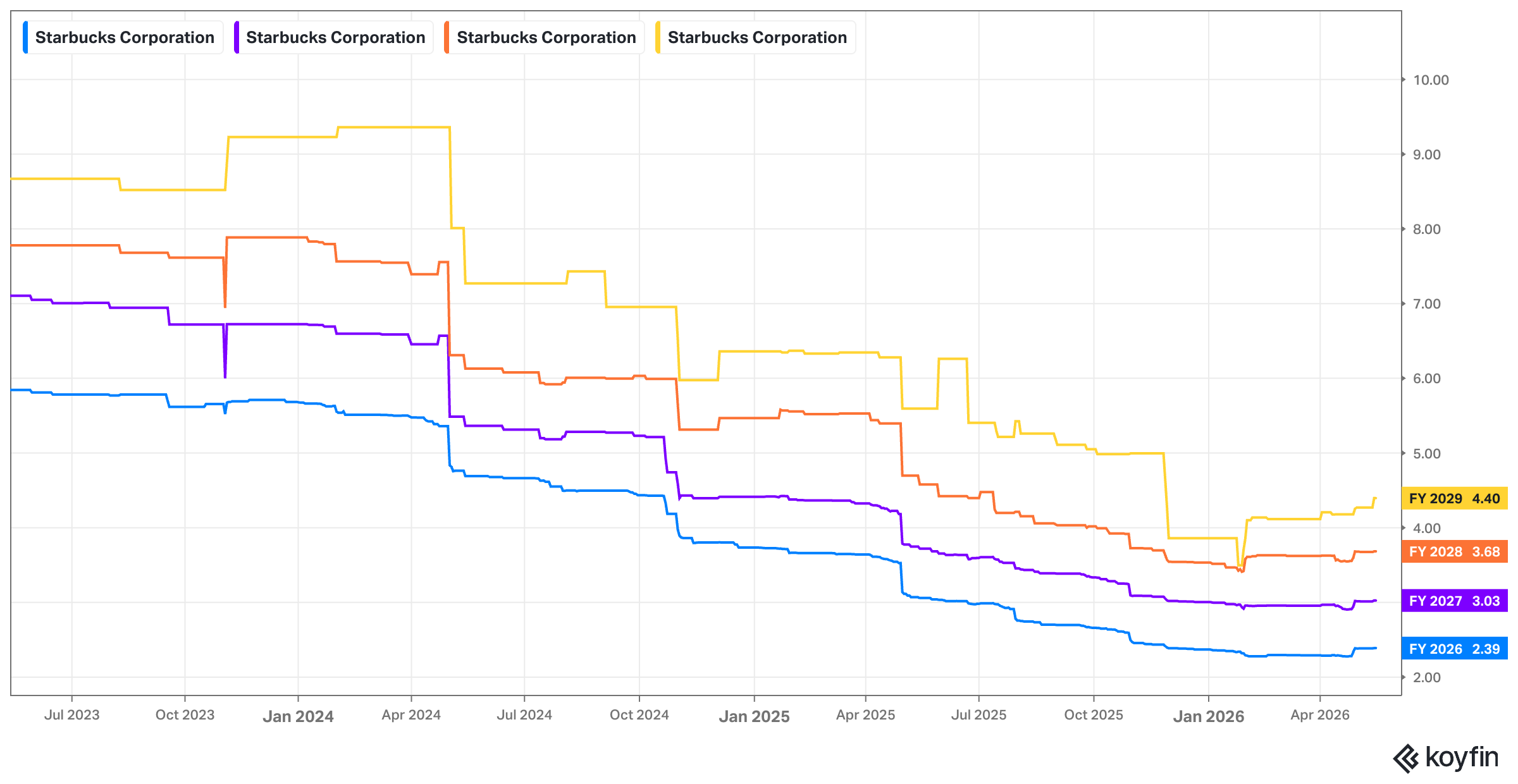

Starbucks raised CSS growth guidance from 3%+ to 5%+, as they excitedly discussed strong CSS trends continuing through April despite higher gas prices. Revenue for the year is expected to be roughly flat due to the 60% sale of its China business to Boyu Capital and the coinciding JV formation. That’s why estimates for FY 2026 and 2027 fell after the call despite outperforming demand. They also now expect $2.35 in EPS, compared to $2.27 guided to last quarter. EBIT margin is still expected to slightly improve as well. While they will get a lot less revenue from China going forward, the revenue they do get will be much higher margin (~50%), which greatly offsets that headwind. They were asked why such a large CSS raise didn’t coincide with a bigger EPS raise. This was related to macro prudence stemming from the aforementioned gas inflation. They’re not seeing any weakness in trends but wanted to include that in the range of possibilities.

- On track to deliver $2B in annual OpEx savings by FY 2028.

- They still plan to open 625 stores this year, with 475 additions planned for their international business (half in China) and 150-175 in the USA.

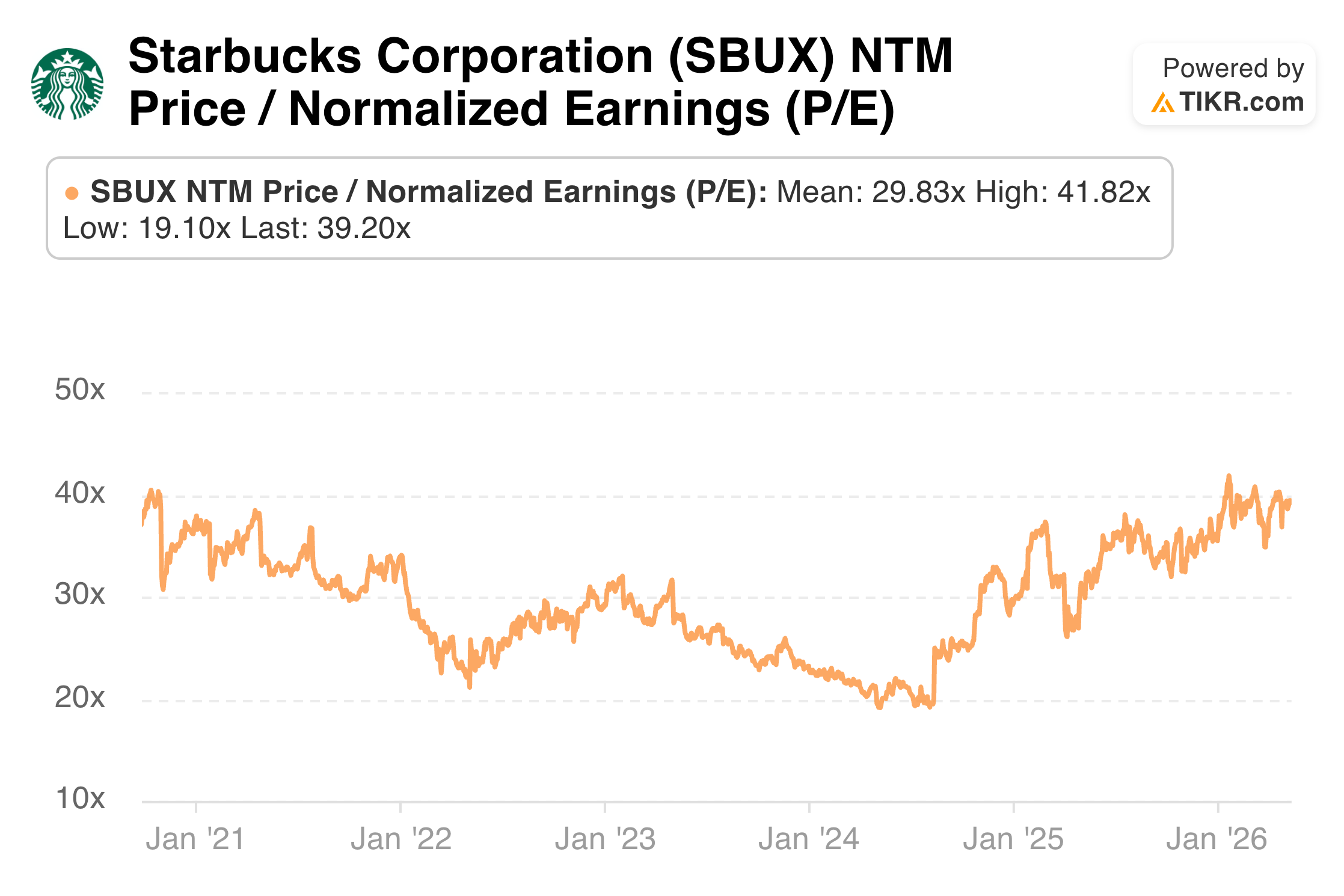

SBUX trades for 40x forward EPS. EPS is expected to grow by 12% this year, 27% next year and 22% the year after.

f. Call & Investor Materials

Turning the ship around – Green Apron Progress:

The Green Apron initiative continues to rock and roll for Starbucks. As a reminder, this entails better workflows, order prioritization tools, upgraded stores, personal touches like hand-written names and no upcharges for non-dairy milk and enhanced labor allocation. This is the key ingredient powering much better financial trends just like leadership said it would over a year ago. Corporate behemoth turnarounds are very hard. New teams routinely come in, get shareholders excited and flop due to underestimating the difficulty in fixing massive and broken enterprises. Niccol is bucking that trend. Just like he did at Chipotle, he’s focusing on the right things and surgically executing on the rollout of every repair. For example, their store aesthetic uplifts have all occurred on schedule with zero store hour disruption and they reiterated the rollout timeline. That would have been unheard of under previous leadership.

As a result of all this work, U.S. morning business volume is back to 2022 peaks, afternoon traffic is improving, comps are accelerating everywhere and SBUX is winning back the type of pristine brand reputation it had surrendered in recent years. They are not earning business via endless discounting like they did under previous leadership. They’re prioritizing much more structural sources of demand. Faster, more consistent throughput… higher in-stock rates… a better menu… prettier stores… a loyalty program upgrade… and more. They’re turning things around the right way. For more evidence, brand affinity scores set 5-year highs (led by Gen Z improvements), value perception improved and momentum fully carried into May.

There’s a lot more improving left to do as well, with new initiatives like scheduled pick-up times expected to be incrementally positive for service speed trends. They still have stores to refresh and still have 40% of their stores not yet at “4 shots” (basically an “out of 5” ranking system). They know how to get those stores back on track because they’ve already proven it for the other 60%. As that plays out, the comp store tailwinds will just keep strengthening.

Turning the ship around – GROW Program:

It’s one thing to provide systems, support and room for stores to improve. But “improvement” can often be a highly subjective and abstractly measured thing. That makes it often confusing for employees to track their success. It makes it harder to connect hard work with tangible and rewardable execution. That’s what the GROW program is for. It’s meant to provide structure and clarity for how SBUX is evaluating their team members. Clarity and concrete goals drive motivation because people actually know what they’re trying to accomplish. This is what splits measurement into a few key performance indicators (KPIs) and uses those indicators to rank stores on the “5 shot” scale. They raised the portion of stores at or over 4 shots by 30 points Y/Y, with plenty of progress left to enjoy. This is helping lower turnover, stabilize store leadership and enable SBUX to effectively handle the surge in traffic they’re currently seeing.

Turning the ship around – Menu:

Menu innovation is accelerating now that SBUX has re-built their idea pipeline following years of mismanagement. Their new energy Refreshers performed better than expected, and SBUX expects to fare well against new competitive entrants in this arena. In a push for even deeper personalization, they're now even letting customers tweak caffeine amounts in these drinks, which is not only creating better product-market fit, but also allowing the products to work better across both morning and afternoon day parts. Customers can choose more caffeine in the early hours, and can elect to lay off later in the day. This is Starbucks getting more out of its product innovation.

Baked-good introductions performed predictably well, as SBUX moves away from guessing on new product introductions to running stage-gate and data-driven processes like they used to. This is helping food attach rates begin to rise, which supported ticket growth during the quarter.

Turning the ship around – Loyalty Program:

The revamped Starbucks loyalty program is performing very well across all tiers. They normally see a sequential seasonal decline between Q1 and Q2 in total membership, yet saw Q/Q expansion this quarter thanks to all the updates they’ve made. Total membership rose 4% Y/Y and frequency is improving as fans gravitate to new perk formats. 4+ visit-per-week members are rising steadily.

More Notes:

- Japan and Korea were cited as international standouts during the quarter.

- They expect international store growth to turn positive again as they lap some closures. China is expected to move from 1,000 locations to 1,500 over the next 3 years.

- Their smaller channel development segment rose by 38% Y/Y thanks to higher Global Coffee Alliance revenue and its multi-serve “Refreshers concentrate” that’s turning into its “largest CPG launch in over a decade.”

- Visibility across the Olympics, Coachella and ChatGPT are working as part of an ongoing effort to lean back into marketing to non-loyalty members.

- Added a new office Nashville to support growth in the Southeast.