Table of Contents

a. Taiwan Semi 101

A brief overview of TSM's business can be found here.

b. Key Points

- AI continues to power impressive growth and guidance raises.

- Gross margin is expected to remain strong despite two major headwinds.

- Packaging competition from Intel is good for the largest piece of TSM’s business.

- Raised CapEx guidance.

c. Demand

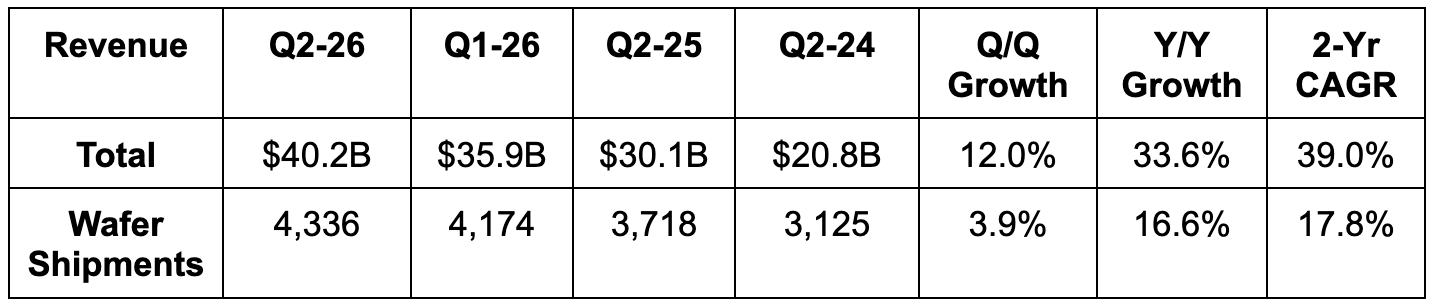

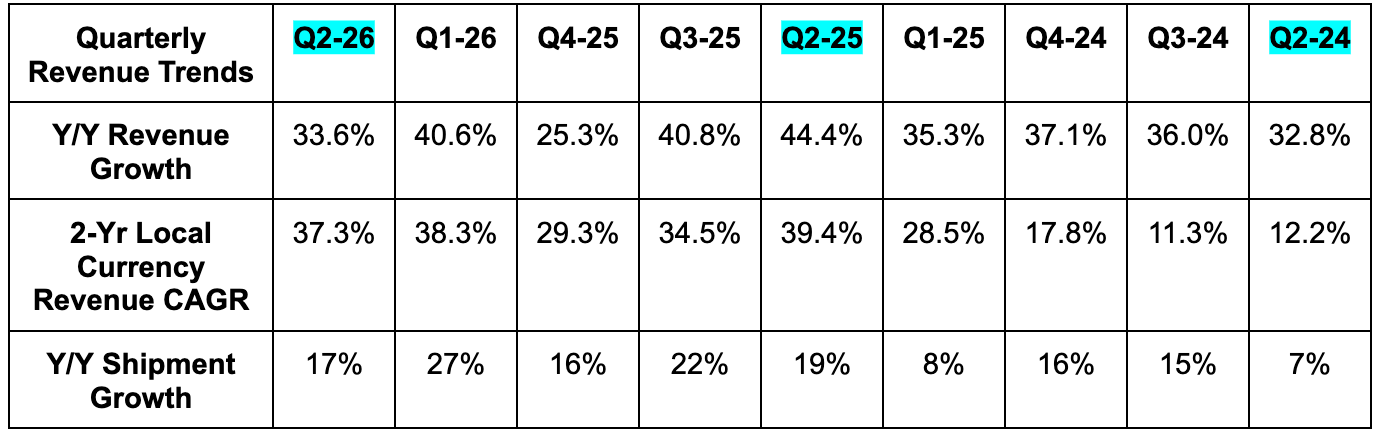

Taiwan Semi revenue beat estimates by 2.3% & beat guidance by 1.5%. Revenue came in right at the high end of TSM’s guidance range. High-Performance Compute (HPC) was again the standout this quarter. It jumped from 61% of total revenue to 66% compared to last quarter, as the segment again grew by 20% sequentially. Smartphone revenue fell 4% sequentially and from 26% of total revenue to 22% of total revenue during that time. This is where rampant memory inflation is hurting TSM customer demand the most. Auto revenue grew by 15% sequentially and stayed at 4% of revenue. Finally, N2-based revenue jumped to 3% of total revenue as that technology successfully proliferates.

d. Profits & Margins

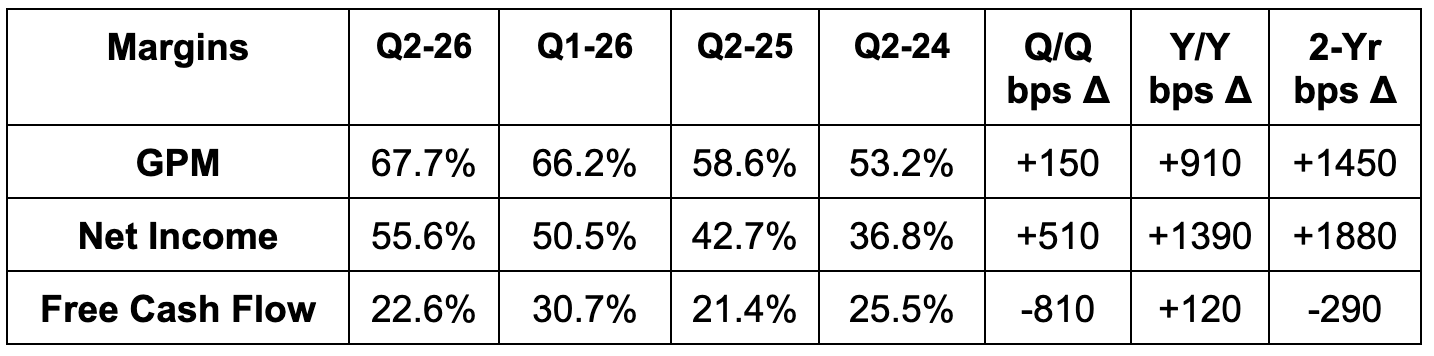

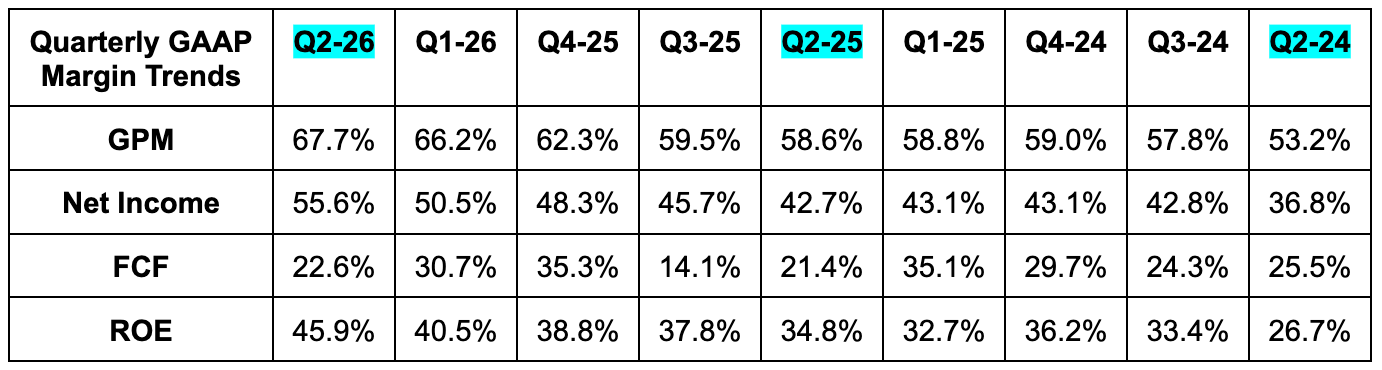

- Beat 67% GPM estimate by 70 basis points (bps; 1 basis point = 0.01%). Y/Y gross margin expansion was due to ongoing manufacturing efficiency gains and higher capacity utilization. It was also despite headwinds coming from the ramp of its N2 technology and overseas capacity scaling.

- Beat $3.83 EPS estimate by $0.48. If we exclude the entire Y/Y benefit from selling its stake in Vanguard International Semiconductor Corporation, it would have beaten expectations by $0.12.

- 77% Y/Y EPS growth would have been 62% excluding this help.

- Beat 42% GAAP return on equity (ROE) estimate by about 4 points.

- Free cash flow grew by 44% Y/Y. This is despite $15.7B in CapEx compared to $9.6B last year.

e. Balance Sheet

- $98 billion in cash & equivalents.

- Inventory rose 27% Y/Y. Inventory turnover days rose from 76 to 87 Y/Y.

- $7 billion in long-term investments.

- $25.5 billion in bonds payable (debt).

- Share count is roughly flat Y/Y.

- Dividends rose by 37% Y/Y.