Housekeeping:

- Click here to read the basics on MongoDB's business.

- My Zscaler earnings review can be found here.

- My Snowflake earnings review can be found here.

- A few dozen other detailed earnings reviews from this season can be found here.

- My current portfolio & performance vs. the S&P 500 can be found here.

a. Key Points

- Early interest in MongoDB's AI products is strong.

- "Several frontier model companies" are MongoDB customers.

- Large backlog outperformance points to strong forward-looking demand.

b. Demand

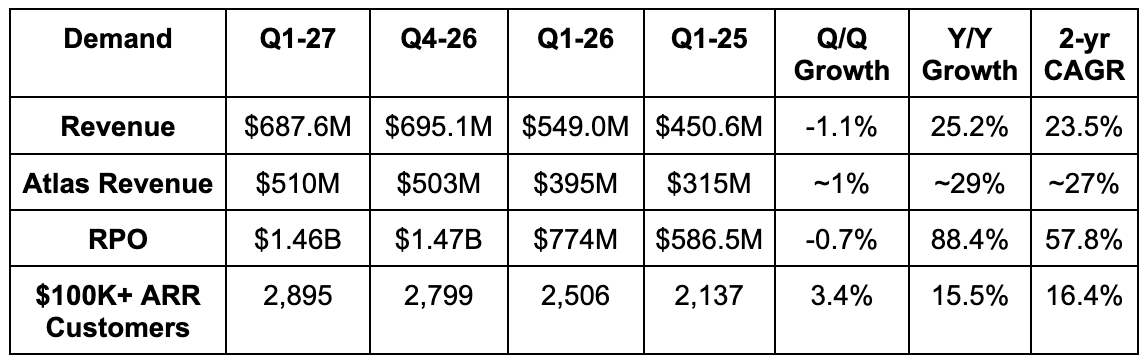

- Beat revenue estimate by 3.6% & beat guidance by 3.8%.

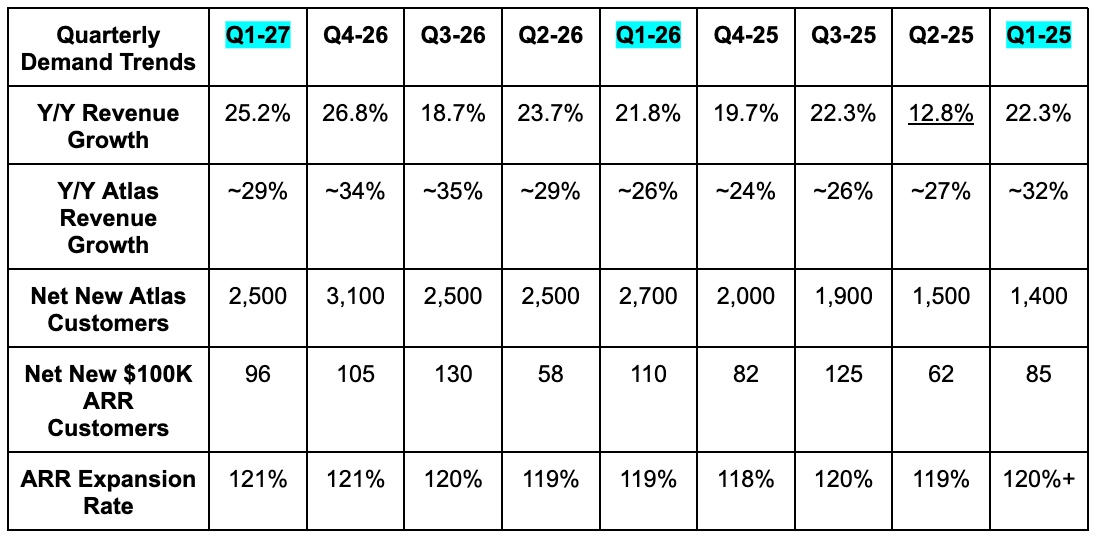

- Good to see a meaningful Y/Y growth acceleration compared to both Q1 2026 and Q1 2025.

- Atlas crossed a $2B annualized run rate.

- Beat $1B remaining performance obligation (RPO) estimate by $460M or 46%.

c. Profits & Margins

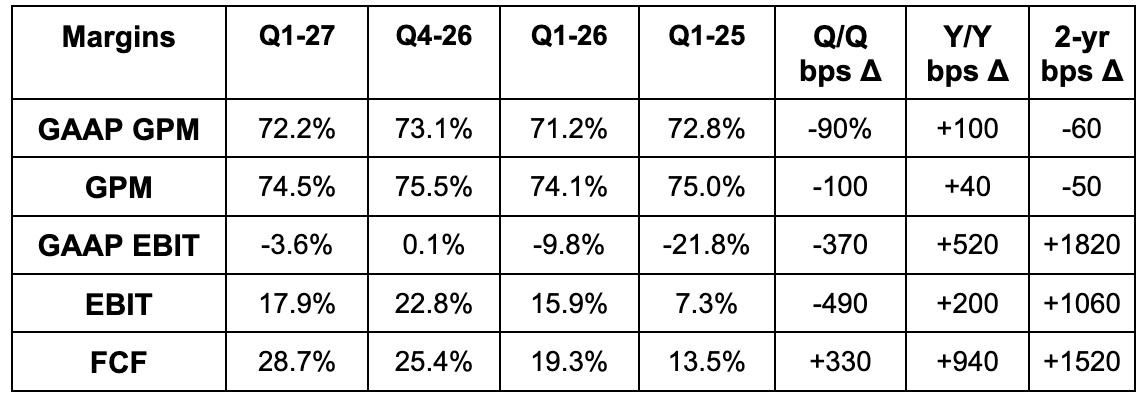

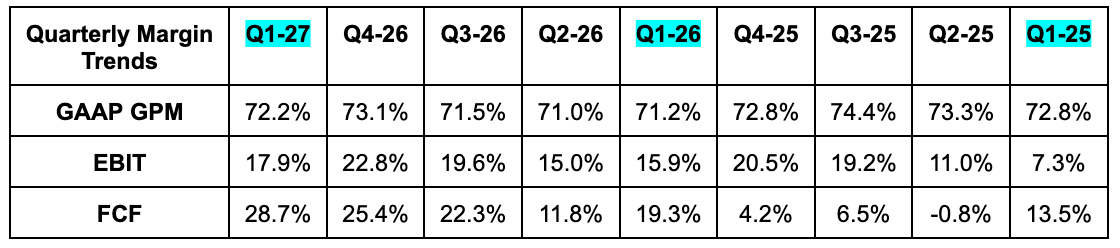

- Beat EBIT estimate by 14.1% & beat guidance by 15.1%.

- This was driven by revenue beats.

- Beat 74% GPM estimate by 50 basis points (bps; 1 basis point = 0.01%).

- Beat $1.17 EPS estimate by $0.15 & beat guidance by $0.15.

- Beat -$46M GAAP EBIT guidance by $21M.

- Beat FCF estimate by 70%. This metric is heavily tied to collection timing on a quarterly basis. Noisy.

d. Balance Sheet

- $2.4B cash & equivalents.

- 0.6% Y/Y dilution.

- No debt.

e. Guidance & Valuation

Annual Guidance:

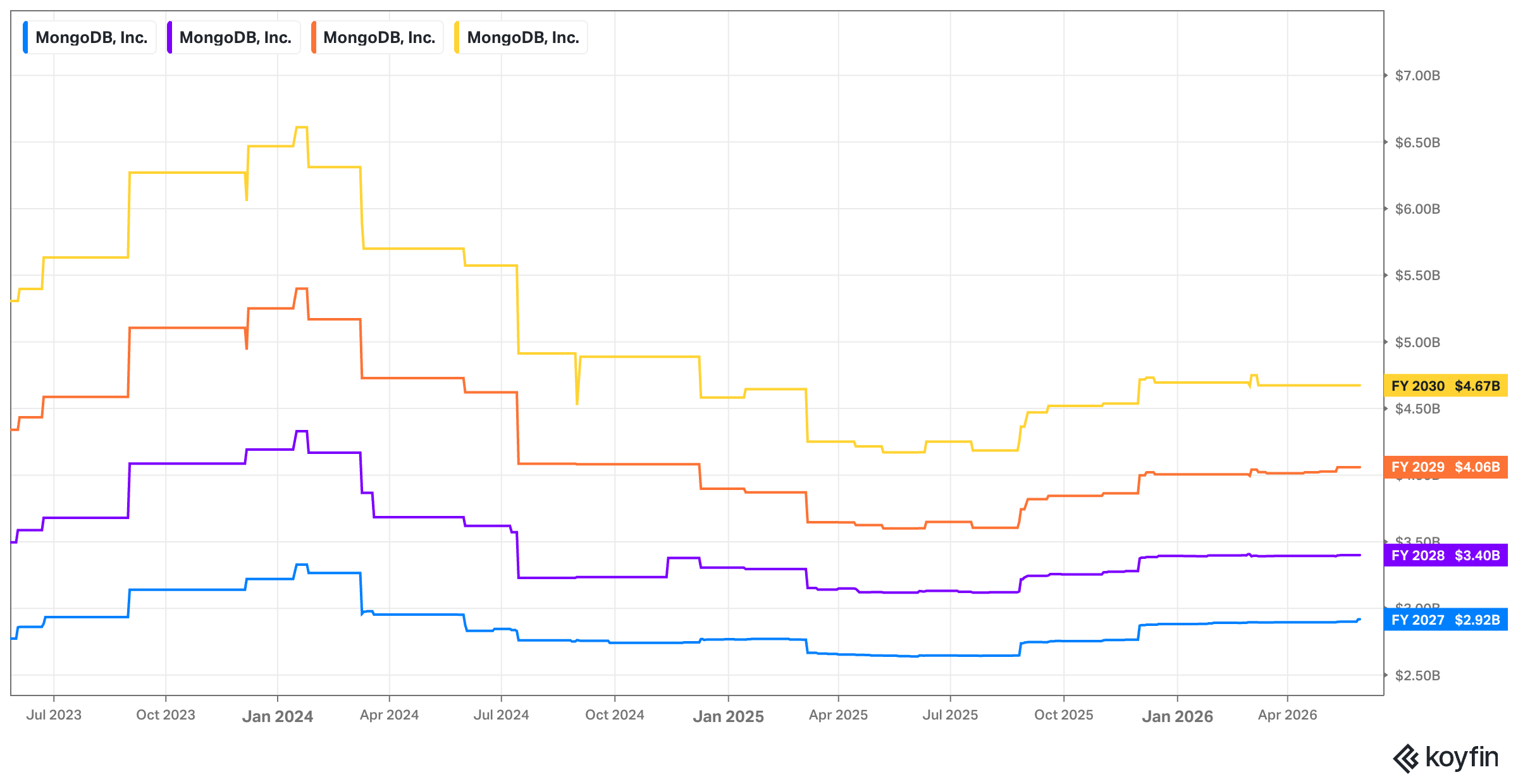

- Raised annual revenue guidance by 2.1%, which beat estimates by 1.4%. Excluding M&A, guidance would have been raised by 1.7% and that would have beaten estimates by 1%.

- Annual revenue guidance also includes 24% annual Atlas growth expectations compared to 22% growth previously forecasted.

- Raised annual EBIT guide by 6.5%, which beat estimates by 6%.

- M&A had no impact on profitability.

- Profit guidance includes higher planned investments in Japan go-to-market and their U.S. federal business.

- Raised annual $5.84 EPS guide by $0.21, which beat estimates by $0.21.

Q2 Guidance:

- Q2 guidance was also well ahead across the board.

- Q2 Atlas revenue is expected to grow by 26% Y/Y. Leadership cautioned investors that the degree of difference in Atlas results vs. expectations will likely be small in Q2. At the business scales and the customer base diversifies, local consumption volatility has a smaller impact. The gaps vs. annual Atlas guidance could be larger for the rest of the year.

- The non-Atlas segment for Q2 is expected to grow by 20% Y/Y for Q2.

More guidance notes:

MongoDB is assuming 0% Y/Y non-Atlas growth for Q3 and Q4 in its annual guidance. Comps do get more difficult, but I still think this is overly pessimistic. Like they have during previous quarters, the team is only including secured deals in the forecast. If there are more wins that come, that will present pure upside to results vs. forecasts. These “surprise” (or not surprising) wins routinely come for MDB and help power the material revenue beats they almost always deliver vs. consensus. They love to sandbag and love to use on-premise business volatility as the excuse. I expect more outperformance vs. the updated annual guide for the rest of the year (even with the smaller Q2 Atlas revenue volatility).

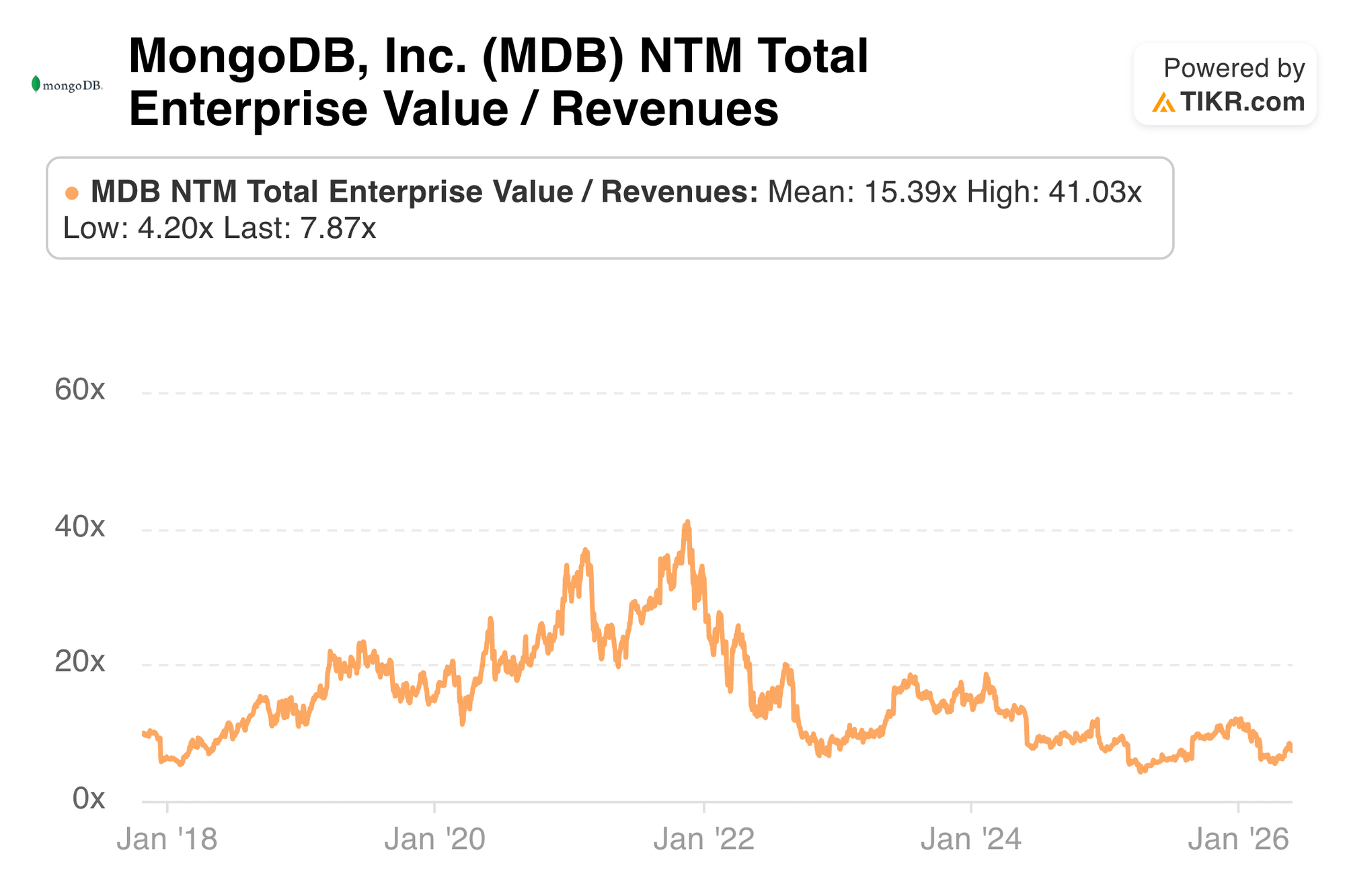

Estimates will move materially higher following this report. As of right now, MDB trades for 45x forward FCF. FCF is currently expected to grow by 6% this year (again that will move much higher) and by 24% next year.

f. Call & Release

Subscribe below to read a review of MongoDB's investor materials, my take on the quarter/investment and so much more.