News of the Week (June 19 - 23)

News of the Week (June 19 - 23)

PayPal; Shopify; Meta; SoFi; Amazon; Uber; Alphabet; Lemonade; Tesla; Match; Final Headlines; Macro; Portfolio

Today’s Piece is Powered by our Friends at Long Term Mindset:

1. PayPal (PYPL) -- KKR

Buy Now, Pay Later (BNPL) Receivables Sale

As it has told investors to expect, PayPal sold its portfolio of European BNPL receivables to KKR this week. Initial proceeds are set to be in the $1.8 billion range with KKR agreeing to purchase up to roughly $42 billion more in future European originations. With this cash, PayPal expects to buy back an additional $1 billion in stock this year ($5 billion v. $4 billion previously). As the deal was already in the works throughout 2023, it was part of the firm’s annual demand and margin guidance -- no changes there. PayPal will continue to underwrite and service the credit product as it has, but now won’t have to store the credit risk on its balance sheet anymore.

What does PayPal Get?

Besides the fresh $1.8 billion cash infusion, PayPal gets to enjoy the original perks of BNPL while eliminating its (and investors’) least favorite part of it. What do we mean by this? PayPal collects no interest on these loans, charges no late fees and doesn’t charge merchants for access to the product. It doesn’t really monetize it directly which is one of the reasons it has become so popular vs. other competition. Instead, PayPal benefits from the volume and engagement “halo effect” that this option brings. By offering its BNPL as another option for flexible consumer repayment, merchants see a 20%+ boost to transactions, a large basket size bump and a material lift in overall volume. This volume benefit feeds PayPal’s revenues and, considering BNPL skews to debut-funded transactions, helps its margin profile a bit too.

PayPal gets to keep enjoying all of these perks. Now however, it can do so without sacrificing its balance sheet flexibility to grow the segment. With its BNPL processing volume rising 160% Y/Y last year to $20 billion (and rapid share gains), the balance sheet bloat was becoming more pressing and this sale alleviates the eventual bottleneck. Simply put, the sale removes a limiting factor for PayPal’s credit growth and allows it to responsibly expand into more product adjacencies without creating excess risk.

Furthermore, PayPal is not a chartered bank. It cannot use deposits to directly fund its loans and instead must fund with equity capital, its cash position and debt. This gives it a slight access to capital and efficiency disadvantage vs. chartered banks. As a payments and technology company, it wants to focus on its strengths and core competencies there.

What does KKR Get?

If PayPal collects no interest and doesn’t charge late fees, why would KKR want this credit? How does it profit?

While we don’t have specific transaction terms, PayPal likely had to offer a slight discount on the receivables to motivate interest. It was likely willing to make this concession to cash out more quickly at slightly worse unit economics and prioritized flexibility today over slightly more margin tomorrow. This is the right decision in our view and one that KKR is happy to support.

It’s worth noting here that PayPal is the highest quality underwriter in BNPL. Its authorization and loss rates are both best in class via the extensive data it has on each customer to round out their profile and to predict repayment ability. Standalone offerings and tech giants do not have this treasure chest of highly relevant financial data to power these decisions. For that reason, the discount PayPal had to offer to attract interest in these assets was likely modest.

Looking Ahead

Leadership in the past had consistently hinted at wanting to sell all of its BNPL receivables. It told us it would start in Europe this year and likely expand elsewhere thereafter. So? There’s probably a North American receivables sale coming at some point to feed its cash pile and share repurchases.

2. Shopify (SHOP) -- Shop Pay

The News:

In the last two years, Shopify has opened its checkout accelerator (Shop Pay) to external surfaces like Meta’s Family of Apps and more. Any Shopify merchant was able to seamlessly offer this option with a click of a button. Shopify’s goal is to maximize merchant success and volume wherever it can. Successful merchants mean a more successful Shopify in a truly cohesive fashion. Because Shop Pay is 4x faster than the average guest checkout and delivers a 10%-50% conversion boost vs. all other choices, placing this button across the internet is a clear way to accomplish Shopify’s mission… So that's what it’s now doing.

Shop Pay will be available for any non-Shopify merchant site for the first time. Shop Pay has been added as a new component to its newer a la carte enterprise package (called Commerce Components by Shopify (CCS)) as a standalone offering. Per the release, this decision was in response to “strong demand from large retailers seeing the success of the buyer network.” This offers some confidence that the opening will be met with a warm welcome. We’ll see.

Why Does this Matter?

This could be materially positive news for a few reasons. The first is intuitive. Shop Pay is Shopify’s largest revenue driver within its merchant solutions bucket. By placing the best-in-class checkout flow (and its 100 million total users) within popular e-commerce sites, Shopify will surely find some market share to juice growth within this segment. The revenue has lower gross margin than its subscription business but comes with a similar EBIT margin which makes the growth just as compelling in our mind.

Again, within commoditized checkout, speed, clicks and confidence are the ways to standout. Shopify’s single click process (the result of its massive payment vault), ultra-low latency and fraud protection program all deliver these edges for merchants. Players like PayPal arguably offer deeper buyer and seller protections, but they’re still working on single click transaction completion.

Beyond the direct revenue boost, Shopify should gain significantly more touch points to drive product cross-selling. CCS merchants will frequently start with the single Shopify product; some will invariably end up with many more. Shop Pay is the perfect frictionless gateway product to open the door to more Fortune 500 brands. These brands simply want optimal consumer checkout choice and Shop Pay provides it. The consumer delight and tangible, incremental merchant success that it delivers should quickly shine. The added revenue and efficiency should leave many of these brands thinking “what else can Shopify do for me?” This is speculative, but really not much of a stretch. We’d be surprised if this didn’t play out.

Next, this evolution is somewhat similar to the path PayPal took to grow into an over $1 trillion volume payments juggernaut. It grew up as a tuck-in payment option to its parent company eBay while Shop Pay did so within its parent company Shopify. Not exactly the same dynamic, but similar. Opening up the PayPal button to the world was a key driver of PayPal’s exploding market share and volume throughout most of the 21st century. Now Shopify is following suit with a seemingly superior product offering. Could this be as impactful to this model as it was for PayPal? Time will tell but we like the strategy.

More Perks:

Largest brands serve as signs of best practices for smaller brands to drive more SMB adoption.

This will enhance Shopify’s customer data sources and profiles to improve other products like its credit underwriting and marketing suites.

Adyen:

As part of the news, Shopify and Adyen are deepening their already tight partnership. Large merchants routinely require global payment processes/methods to sell throughout the world. Shopify uses mainly Stripe and Adyen (and PayPal’s Braintree in France) to provide this flexibility and reliability. Stripe is the main partner for Shopify Payments, but Adyen offers key plug-ins to local payment methods (LPMs) like iDEAL in the Netherlands and others.

The deepening relationship will entail a more complete Adyen integration for large global enterprises to enjoy its full payment roster for optimal conversion. Interestingly, it will also include a joint go-to-market partnership to pursue larger clients.

Payment orchestration has become more important within commerce as processes have become more global and complex. For certain transactions, Shopify can orchestrate a transaction through Adyen’s processing network to close a purchase in the most profitable way for the merchant. Sometimes Stripe is the best, highest transaction margin option. By working closely with both, it ensures it can offer merchants the best choice a larger portion of the time. Another small source of making merchants more successful.

Long-Term Mindset is a FREE weekly newsletter emailed each Wednesday. Each issue contains five pieces of timeless content to encourage you to think long-term. All issues can be read in less than 1 minute. There’s a reason why we are consistent readers and think you should be too. Subscribe here.

3. Meta Platforms (META) -- WhatsApp and Regulation

a) WhatsApp

WhatsApp is debuting its “Community Entry Point” feature to allow users to navigate and see lists of groups and organizations linked to communities. WhatsApp is still in the early innings of finally ramping up monetization with its massive global user base. That monetization will entail things like messaging ads, new tools like fetching an Uber through the app and business profiles.

Brand discovery is a big part of making monetization as impactful as possible. By organizing WhatApp’s giant ecosystem into more intuitive, categorical groupings, these businesses will inherently become easier to find and interact with. This tool won’t be directly monetized, but makes extracting value from the WhatsApp ecosystem easier for Meta.

b) Canada

Canada’s Online News Act was passed into law. This law forces digital publishers to negotiate with news organizations to pay them for access to their content. Meta claims the law “ignores the realities of how the platform works.” It discounts the value of Meta’s unparalleled traffic to near zero while overlooking the immense value that news organizations get from plugging into that traffic for free. It creates inefficiency by creating arbitrary guardrails to value content rather than letting organic interest and impressions dictate that value like it should. While this is a bit annoying, it’s not all that material to Meta. With half the planet on its apps, 30 million users in Canada won’t be all that needle moving while they’ll still be able to use the services without this news content.

4. SoFi Technologies (SOFI) -- Supreme Court, SoFi Invest & Noise

a) Supreme Court

The supreme court will rule on the legality of $10,000 ($20,000 for Pell Grant recipients) in student loan forgiveness late next week. While this decision matters for SoFi’s business, it already secured the potential big win via the end of the student loan moratorium. Payments will resume in October and that is what mattered most. Why? Potential forgiveness represents only about 15% of the outstanding credit SoFi can refinance. For Pell Grant recipients that forgiveness is closer to 30% of the outstanding credit, but SoFi generally underwrites highly affluent borrowers that would qualify just for that 15% if anything.

The other 85% of the outstanding credit will soon be strongly motivated to refinance in order lengthen terms or lower rates. That is what the end of the moratorium means and is why that was so vital to SoFi’s business. Furthermore, newly originated student borrowers will now be driven to refinance as soon as these new borrowers can secure more favorable terms. That wasn’t true for the last 3 years. The math is simple: 85% of outstanding credit and 100% of new originations being pushed to refi is far more impactful than 15% of outstanding credit.

How will this ruling go? We really don’t know and can only speculate. With the conservative leanings of the current court however, the majority expect forgiveness to be deemed unconstitutional.

b) SoFi Invest

SoFi Invest’s product offering is too limited and the user interface needs work. The company has done a wonderful job rapidly building out its one-stop shop in just a few years. It’s now time to make sure products like this one are as pretty, slick and functional as possible. Most of its products are… but this one isn’t. SoFi and Anthony Noto know this to be the case. In response to some Twitter complaints this week, Noto told investors that SoFi was working on a soon-to-be-rolled-out overhaul to its invest interface. In our view, it should look to emulate Robinhood’s as closely as possible.

c) Noise

Compass Point initiated SoFi with a sell rating this week and a $5 price target. Aside from fundamentally positive recent notes from other firms like Truist, Bank of America, Oppenheimer, BTIG and others… and despite Compass Point not being a name brand within sell side research, it’s still interesting to hear them out. The research report read exactly like other bear cases we’ve heard leadership consistently debunk in investor conferences recently. It centered on loan valuation methodology, room to grow the balance sheet (or capital and leverage ratios), credit quality amid poor macro and capital market demand for its loans. It even repeated the Wedbush-cited risk of SoFi possibly needing to reclassify its loans from held-for-sale to held-for-investment. This is not even remotely realistic as a possibility. And, even if it were, it wouldn’t impact SoFi’s credit valuation.

We’ve addressed all of these concerns in detail in recent issues and would point readers to those pieces to avoid being redundant. The 3 pieces we’d recommend can be found here, here & here.

Overall, this changes absolutely nothing about my SoFi view and bull case and offers credibility to the idea that some traditional financial analysts do not understand this company. The Bank of America and Oppenheimer notes on pristine fundamentals but a stock that had run too far too fast were entirely valid. The stock needed to take a breather and it has. This note and the Wedbush research are less valid in our view.

5. Amazon (AMZN) -- Gen AI & Prime

a) Generative AI

Amazon is investing $100 million in a new “AWS Generative AI Innovation Center.” The program is designed to connect AWS AI/ML experts directly with clients to educate them on new and future Gen AI use cases. The tool will not be directly monetized, but instead used to erode some up-selling friction for its higher margin AI-based workloads. These experts will effectively hold the hands of clients in their journeys to build custom products and models using Amazon’s Gen AI capabilities. Its foundational model (Bedrock), and chip sets (Inferentia and Tranium) will surely be central pieces of this endeavor while Twilio and Ryanair are among the first users.

This news comes as yet another firm upgraded Amazon due to a presumed bottoming in AWS growth and a re-assessment of its AI positioning. We counted 6 upgrades like this one in the past month; maybe the sell side reads the newsletter. Azure and ChatGPT surely won the first prize here, but there will be countless more down the road. Amazon will win its fair share of these prizes like it has done within cloud computing.

Our friends at The Transcript shared a great quote from AWS’s CEO this week on this matter:

"You ask yourself the question -- where are the different runners three steps into a 10K race? Does it really matter? The point is, you’re three steps in, and it’s a 10K race.” -- AWS CEO Adam Selipsky

And as macro begins to brighten, its SMB niche should show further upside vs. Microsoft’s more durable enterprise bread and butter which hasn’t been as impacted by a chaotic backdrop. This relative tailwind should erode the “Amazon can’t compete in AI” narrative further as growth rates could converge.

b) Prime and the Federal Trade Commission (FTC)

Find yourself someone who loves you as much as the FTC and Chair Lina Khan love to sue mega cap tech. This week, the FTC accused Amazon of subtly “tricking” customers into signing up for a Prime subscription and subsequently making cancellation difficult. It claims Amazon is using Dark Pattern techniques to “deceive” users into enrolling and auto-renewing by making purchasing without a subscription somewhat more confusing of a process. Dark Patterns are interface formats designed to push users towards an undesired action. To be candid, this lawsuit read like a FinTwit short piece. It ignored all of the value that Prime provides and used a few extra clicks in a cancellation process as its centerpiece of evidence against the firm. Amazon called these claims “false on the facts and the law.” We think this headline will turn out to be irrelevant.

6. Uber Technologies (UBER) -- Drizly B2B

Uber’s Drizly (alcohol delivery) debuted an updated set of “business-focused offerings” this past week. These offerings include more readily available and actionable customer service and are geared to make Drizly a better enterprise partner for corporate events like golf outings. Like every other product launch for Uber, this is yet another value-add tool that can be bundled into its Uber One subscription. This isn’t as consumer facing as its other products in the bundle, but still could be utility-building for some users.

Broken record alert: With Uber’s far healthier balance sheet and margins vs. competition, it has earned the flexibility to debut more products. These products, along with shorter wait times and broader availability for core services, enhance retention, lower churn, boost lifetime value and create a higher quality book of business. That’s the evolution Uber is working through… and with 25% of its bookings now via Uber One, it’s clearly working. A company cannot pursue product expansion when its core business is struggling or its liquidity is lacking. Uber no longer has either of those restrictive issues to deal with as new leadership has gracefully turned this bloated, lost model into a developing cash flow machine.

7. Alphabet (GOOGL) & Apple (AAPL) -- India & Regulation

a) India

Over the last several months, Apple has announced the movement of some product manufacturing from China to other parts of the world. It is leaning more heavily on India for several products and shifting some MacBook production to Vietnam as well. Geopolitical tensions are stable but still quite heated, and mega cap tech is taking note.

This week, rumors swirled that Google is now looking to shift some of its Pixel phone supply to India and joins both Apple and Samsung in doing so. As we discussed last week, India’s Government is business friendly with incentive programs in place to motivate this shifting. This movement comes as Prime Minister Modi visited the White House this week. India’s population is very young, still growing at a nice pace and is well behind Western Europe and UCAN in its technological evolution. This is a perfect backdrop for tech players to pursue. Maybe that’s why Apple is also reportedly planning to bring its Apple Card to the nation.

b) Regulatory Irony

Alphabet filed a complaint with the FTC this week against Microsoft Azure. The complaint sounded a bit odd to us as it was based on Microsoft using its Office 365 bundle to skew cloud contract bids in its favor. This bundling is how Microsoft has morphed into a multi-trillion dollar company and has done so for decades; it’s hard to see this headline turning into anything meaningful.

The irony of this news was that it coincided with another ad tech lawsuit. Gannett became the latest player in open internet programmatic advertising to file a lawsuit against Alphabet. The basis of this lawsuit closely follows the theme of other filings and the Department of Justice’s current investigation. It complains about Google’s total control over both the supply side and the demand side of its programmatic advertising environment. It uses this conflict-fostering control to force buyers to accept opaque and subjective reporting metrics. It leverages the market power to allegedly award auctions to partners and friends vs. always giving it to the highest bidder. The Trade Desk has been an aggressively open critic of these practices as it leads to significant inefficiency and deadweight loss within the supply chain. Players like Google and others predatorily take advantage of this by commanding more of the pie than the value they provide justifies.

c) Ads and Shopping

In other advertising-related news, Alphabet debuted new tools to help further automate campaign operation. “Demand Gen” is one of these tools and was built to contemplate all available factors and covariance to design the most profitable campaigns on behalf of stakeholders. It works on Google, Gmail, YouTube and all other Alphabet properties that run ads. The added ease of use is expected to lower the barrier for some less capable advertisers using Alphabet for their campaigns.

To try and ease rampant claims of a lack of transparency, Alphabet debuted a few other tools. These products will serve as a more open archive for tracking placements and performance. Finally, it is currently split testing some conversion projects to ideally raise return metrics for buyers and CPMs for itself.

In terms of shopping, YouTube will launch its first shopping channel in South Korea this month. Korea is arguably ahead of the rest of the world in terms of the maturity of commerce within live streaming. There are well-entrenched players already in the nation like Naver, but Alphabet wants its piece of the opportunity.

8. Lemonade (LMND) -- Reinsurance Renewal

The News:

Lemonade closed on a renewal of its reinsurance program this week. According to leadership the contract was signed “in good time and on good terms.” While that’s an abstract claim, the deal was led by “tier-one carriers” and “oversubscribed on all dimensions” which does hint at a healthy appetite to share Lemonade’s book of risk.

The new structure comes with a 55% quota share protection program which is identical to the old expiring arrangement. Quota share protection refers to the portion of premiums being shed and transferred from the insurer to the reinsurer to help spread out risk and lock in a portion of revenue. Similarly, Lemonade’s variable ceded commission rate will likely hover around that 55% proportion and will be very similar to the rate under its old agreement. The renewal now includes Metromile’s business.

“It says a great deal when some of the world’s largest and most respected reinsurers choose to stake their capital on the performance of our business.” -- Co-CEO/Co-founder Daniel Schreiber

Why This Matters:

Lemonade’s business is maturing and scaling from a single product in a few states to a wide range of insurance products in all 50 states. As this plays out and revenues diversify, its ability to absorb and tolerate risk rises commensurately. It’s easier to deal with a storm in New York when the majority of your business doesn’t take place within the state. Lemonade has started to reach that point and so has gradually lowered its share protection proportion from 75% at the IPO to 55% now. This means greater potential losses and greater potential revenues for the firm. Reinsurer willingness to participate in this evolution on favorable terms points to the quality of its underwriting.

Lemonade trusts that its underwriting models have been effectively seasoned to justify this added risk retention. These models, for example, can now underwrite customers at an address level vs. previously being at a zip code level. You can imagine this added granularity helps when, for example, you have a neighborhood with some houses on a steep slope and some on flatter ground. Premiums should reflect that difference.

Today’s 55% quota protection proportion is, in leadership’s mind, ideal for allowing the firm to thread an important needle. It keeps Lemonade asset light and nimble enough to focus on growth along with constant underwriting and service model upgrades. It also allows them to more meaningfully share the upside of their underwriting improvements with these reinsurance vendors. Investors have been told to expect this protection proportion to continue falling over the long term.

Other Items to Note:

Lemonade reiterated its Q2 and 2023 guidance as part of the release.

Formed a new risk-bearing entity called Lemonade Re in the Cayman Islands. This will be used to hold some of Lemonade’s incremental retained risk.

Created a captive cell in Bermuda to retain its windstorm risk. A captive cell is a siphoned-off piece of a parent insurance company to cover and operate a specific product or risk bucket. It’s formed and compartmentalized with its own asset and liability format.

9. Tesla (TSLA) -- Charging Network

One by one, competing auto manufacturers are lining up to integrate with Tesla’s charging network (part of its services revenue worth 10% of total revenue). First and foremost, this should mean materially more charging revenue. Goldman Sachs (thank you to my friend @stocktalkweekly on Twitter for sharing this research) saw this network being worth $25 billion in annual sales before all of these integration announcements came. This trend raises that demand ceiling.

More Perks:

The trend serves as yet another vote of confidence for Tesla leading this market for years to come… and well after legacy manufacturers have transitioned to electric.

Should boost EV adoption as charging stations become far more readily available for competing brands. That added adoption should benefit all players including Tesla. If more customers are choosing between EVs instead of gas-powered models for their next car, that benefits the leader.

It could also lead to solar cross-selling as new customers enter the ecosystem.

Opens Tesla up to billions in more grants and subsidies from the National EV Infrastructure Program as it aids sustainable transportation adoption.

10. Match Group (MTCH) -- Where it Needs to Be

A Twitter account (handle is @modestproposal1) shared some great dating app data this week from an Evercore survey on usage. The results of the survey were encouraging. Match’s Tinder leads the Gen Z category with 71%. Bumble is at 50% and Match’s Hinge app has 47%. With Millennials, Tinder leads with 60%. Bumble has 43% and Hinge 38%. For Gen X, Match’s Plenty of Fish leads at 36% with Tinder at 35% and competitor eHarmony at 35% as well.

This supports a crystal clear picture: Match dominates online dating. Tinder is the clear number one and has seen its revenue trends turn positive as of April and May (after some struggles). Hinge is the most exciting growth story in the space as it races to the top of app charts across the globe. Bumble is the most threatening competitor, but Match enjoys 50%+ global share of this $10 billion and growing industry. It does not need to take more share to succeed (though we think it will). If you believe online dating isn’t saturated (as we don’t), there’s a lot to like here as we’ve been arguing for a while. The fact that it isn’t saturated seems utterly obvious to us, but some disagree and time will tell.

Match is briskly accelerating back to 10%+ growth as Tinder shows clear signs of improving execution under new management and Hinge thrives. Impairment charges from the old team’s poor Hyperconnect M&A decision should be mainly behind it. The Asia recovery, where it dominates, is entirely ahead of it. EBIT and EPS is set to compound at 17% from 2023-2025, it sports a FCF yield of 7% and will buy back about 8% of its shares as part of the current program. At 16x this year’s earnings and 13x 2024, the company is finally executing and the stock is cheap. Good combo.

11. Final Company Headlines:

Lululemon is finding it difficult to sell Mirror. In our view, it should liquidate the asset for whatever it can and move on. There’s no need to spend more time and money on this dud. Just liquidate it.

Mastercard is partnering with Alipay in China to create more seamless payment experiences for travelers as its economy opens back up.

Visa named Chris Suh as its new CFO. Suh was previously the CFO at EA and was the VP and CFO of Microsoft’s Cloud and AI group before that.

Shopify is testing new AI automation tools for customer support functions.

Microsoft’s Xbox is raising the prices of its game pass and consoles. Microsoft continues to battle with regulators to try and close its acquisition of Activision Blizzard. Best of luck.

12. Macro

Housing Data:

Building permits for May came in strong at 1.491 million vs. 1.425 million expected and 1.147 million last month.

Housing starts for May were quite strong at 1.631 million vs. 1.4 million expected and 1.34 million last month. This represents 21.7% M/M growth vs. the -2.9% growth analysts had forecasted.

Existing Home sales for May were 4.3 million vs. 4.25 million expected and 4.29 million last month.

Employment Data:

Initial Jobless Claims of 264,000 vs. 260,000 expected and 264,000 last report.

Output Data:

The Manufacturing Purchasing Managers Index (PMI) for June was 46.3 vs. 48.5 expected and 48.4 last month.

The S&P PMI for June was 53 vs. 54.3 last month.

The Services PMI for June was 54.1 vs. 54 expected and 54.9 last month.

Powell Speaks on Capitol Hill:

Powell repeated much of what he said during the rate decision presser last week. He told us the Fed’s base case remains 2 more small rate hikes. We don’t see that as likely. Data continues to point to a slowing economy, cooling real-time inflation and the start of a weakening employment market to drive better supply/demand balance. If they’re data dependent, this should prevent them from continuing to hike. If they do keep hiking, however, that won’t change my process. Strong companies will succeed regardless of if the Fed Funds rate ends up 25 bps higher than we think it will. These strong companies aren’t nearly fragile enough for success to be dictated by this and the potential difference in rate of cash flow discounting is minuscule at this point.

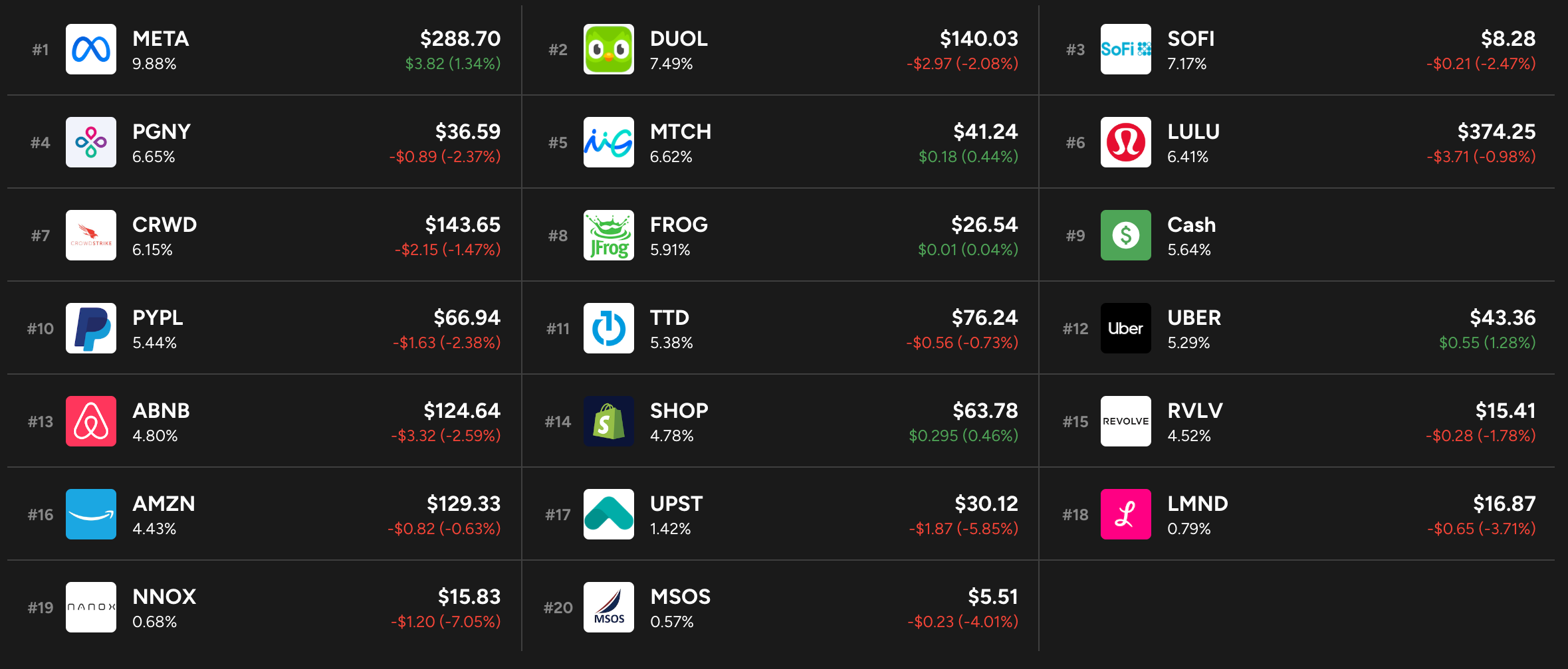

13. Portfolio

No transactions this week.

Hey Brad! I'm George Kailas CEO of Prospero.Ai our weekly letter (linked below) is approaching 20K subs and I think our audiences would enjoy each others content. Would love to talk about collaborating on analysis or recommending each others pages. Feel free to email me @ George@prospero.ai thanks!

https://prosperoai.substack.com/