Other reviews from this season to read:

- Nu

- Mercado Libre & Datadog

- AMD & Uber

- Axon

- SoFi

- Amazon

- On Holding

- AppLovin & Cloudflare

- Duolingo

- Meta

- Starbucks

- Lemonade

- Robinhood

- Hims & The Trade Desk

- Alphabet

- Sea Limited

- Shopify & Coupang

- ServiceNow

- Apple

- Spotify

- Palantir

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

I also sent a piece on SoFi CEO Anthony Noto's investor conference interview earlier in the week.

Next week, readers will get reviews on Zscaler, Snowflake and more companies.

Table of Contents

1. Cava (CAVA) – Earnings Review.

a. Key Points

- Notably impressive comparable store sales (CSS) growth led by traffic.

- Salmon has now launched.

- Left room for oil inflation-related margin headwinds in new guidance.

- New stores are performing well.

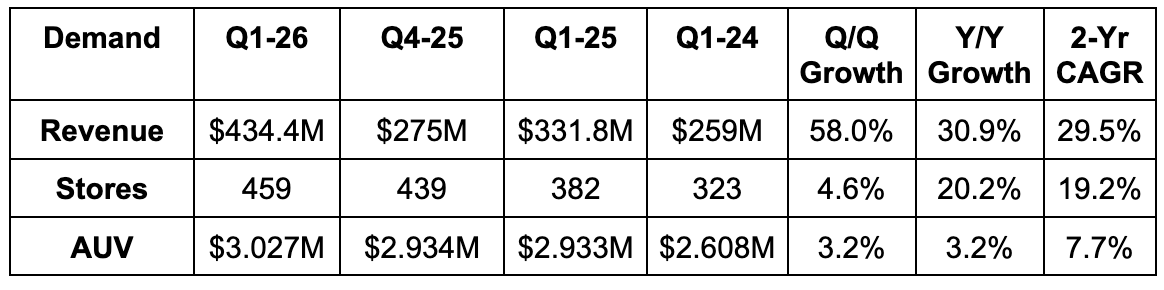

b. Demand

- Beat revenue estimate by 4.8%.

- 9.7% comparable store sales (CSS) growth beat 6% growth estimate.

- 459 stores was ahead of the 456 store estimate.

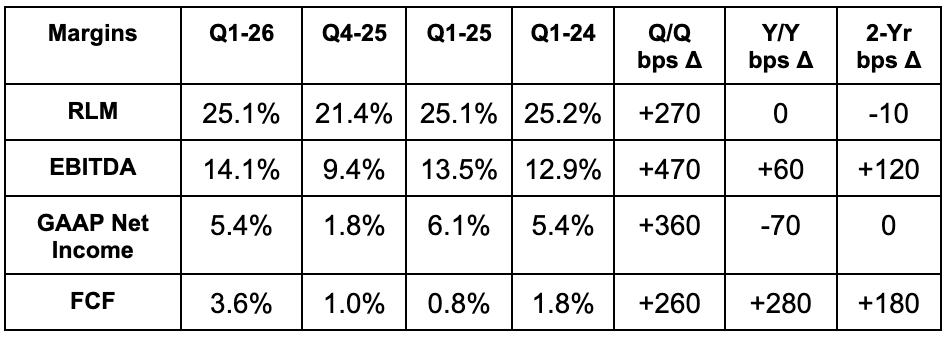

c. Profits & Margins

- Missed 25.3% restaurant-level margin (RLM) estimate by 20 basis points (bps; 1 basis point = 0.01%).

- Beat EBITDA estimate by 7.7%.

- Beat $0.17 EPS estimate by $0.03. This fell modestly Y/Y due to a lower Y/Y tax benefit. This impact is excluded in the margin table below.

For restaurant-level margin, tailwinds included more fixed cost leverage from higher AUV and favorable food mix. Headwinds included mix-shift to third-party delivery and ongoing wage investments (including their new Assistant General Manager (AGM) initiative). 3rd-party delivery rising as a percent of total revenue is why other operating expenses were 13.3% of revenue vs. 12.5% Y/Y. Corporate-level expenses were 11.8% of revenue vs. 12.5% Y/Y mainly due to larger economies of scale.

d. Balance Sheet

- $296M cash & equivalents.

- Share count roughly flat Y/Y.

- No traditional debt.

- Untapped $150M credit revolver with the opportunity to boost if needed (it isn’t).

e. Annual Guidance Updates & Valuation

- Raised comp store growth guide from 4% to 5.5%, beating 5% estimate.

- Slightly raised restaurant margin guide, slightly missing expectations.

- Raised EBITDA guide by 3.3%, missing expectations by 0.5%.

- Raised new store guidance from 75 to 76.

Cava’s updated annual guidance continues to assume CSS growth trends unfold less favorably than they currently are. So far during Q2, CSS growth has been on par with the strong Q1 result, with some help from easier Y/Y comps. Specifically, they expect CSS growth to fall to roughly 5% for the rest of the year in their guidance, despite seeing stronger activity than that.

Leadership was asked why the large CSS growth raise did not coincide with a larger margin raise for the year. This was due to baking a 30 basis point headwind into their outlook to account for energy inflation and "ongoing geopolitical uncertainty." Higher gas prices hurt quick-service traffic and Cava’s input costs include materials like polyethylene for their containers.

All of this sounds like they're positioning the company for another beat and raise quarter, barring a sharp worsening in the macroeconomic environment.

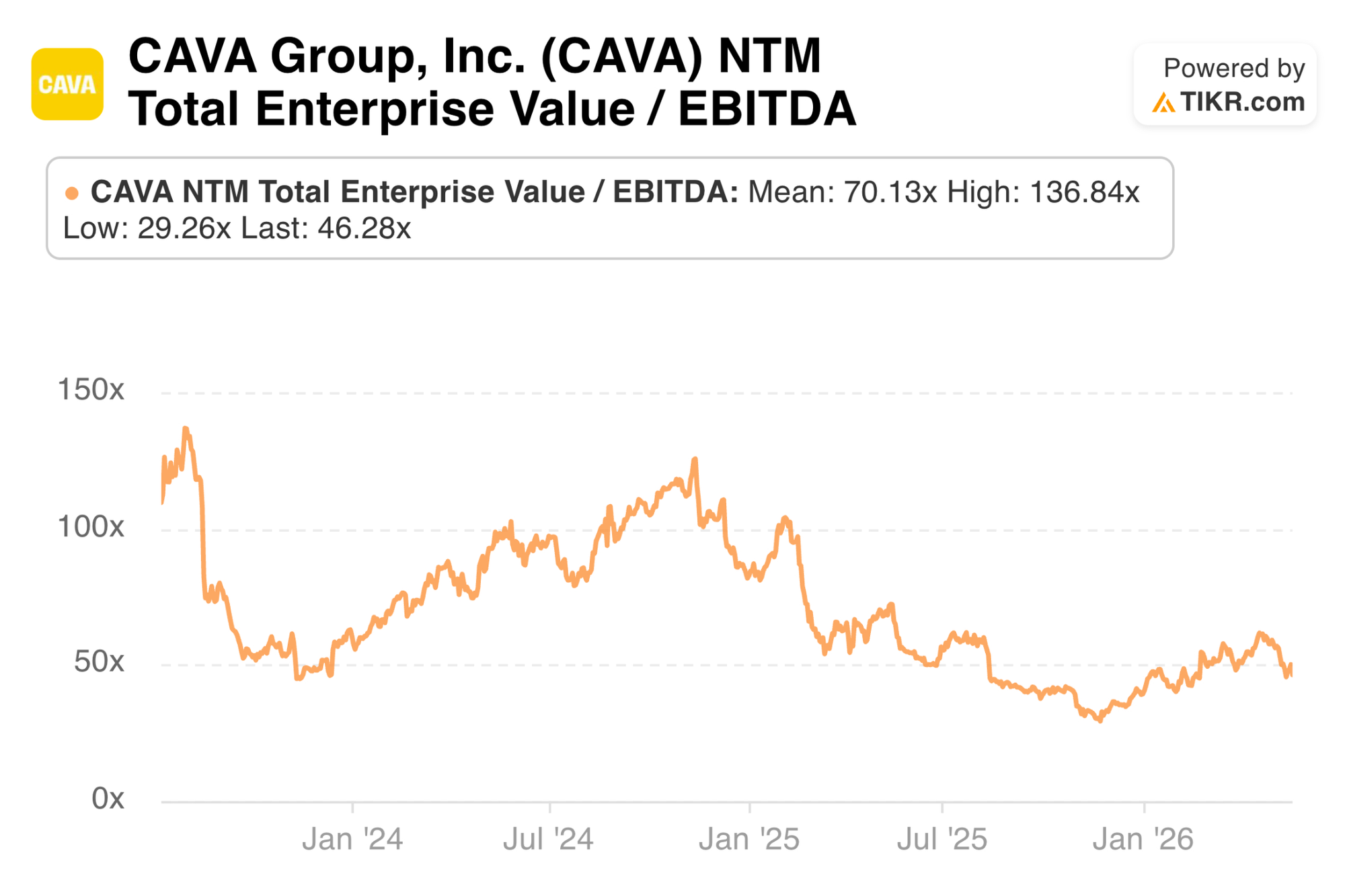

Cava trades for 136x forward EPS and 46x forward EBITDA. EPS is expected to grow by 1% this year and by 33% next year. EBITDA is expected to grow by 24% this year and by 26% next year.

f. Call & Release

Why They’re Outperforming Peers:

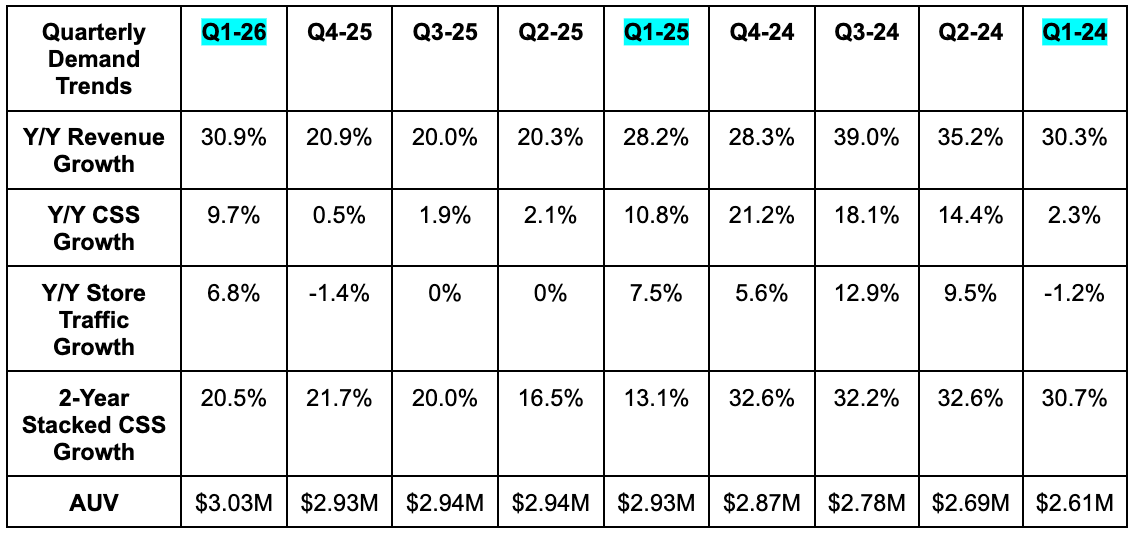

Cava is clearly taking market share from other quick service lunch options around the country. Chipotle is barely maintaining positive comp store sales growth, while others like Sweetgreen and Wingstop posted deeply negative results for Q1. The excuse themes across the category have been energy inflation leading to lower discretionary restaurant spend and a highly promotional environment. Cava didn’t make those excuses and also didn’t cite brief and partial government shutdowns during the quarter despite their store base over-indexing in the D.C. area. They acknowledged higher gas prices and that the macroeconomic environment wasn't overly rosy, but think their food, value, and service are structural tailwinds that are helping it win anyway. Things like rapid store growth and brand awareness rising from 62% to 66% Y/Y also helped. But this strength is being carried by the most encouraging thing possible: Healthy same-store traffic. The nearly 10% Y/Y CSS growth wasn't because they're hiking prices through the moon. They're not. There has been no change to their long-term oriented mindset in this regard.

CSS growth was instead powered by nearly 7% Y/Y traffic growth, despite lapping 7.5% traffic growth last year. This was not a byproduct of easy comps or a one-off in any way. It was their brand, their go-to-market and their model outcompeting everyone else and earning this strong result amid a shaky backdrop. Strength was equally healthy across every single geography and every single income cohort Cava serves.

And while the blend of great value, food, and service surely is the main ingredient powering Cava’s success, variety helps a ton too. Cava offers exponentially more ingredient combinations than other leading bowl chains, like Sweetgreen and Chipotle. They give customers more flexibility to seek value through more affordable options, or to dress up their lunch with premium add-ons for those seeking more of a splurge. And vitally, they do so in an orderly fashion, avoiding too much labor complexity or slowing down throughput. Many in the sector right now are complaining about a "K-shaped" economy (the wealthy doing better than everyone else). Cava is taking better care of both the upper and lower echelons, and these are the results.

Going back to sustainable value for a moment, a superior approach to pricing is also helping Cava stand out from the pack in 2026. Over the last several years, they've hiked their average prices well under the CPI, unlike some competitors. They have sought to maintain compelling value and have practiced a consistent motivation to use supply chain efficiencies, operational automation, and economies of scale, to pass some value onto the consumer. They could probably have higher margins right now if they wanted to. They are just not focused on short-term financial optimization. They're focused on building a generational quick-service company. This is partially why they’re not discounting in pursuit of more traffic. The strong performance was not promotion-powered, but instead driven by full-price demand.

Any way you try to unpack the traffic growth number to gauge whether or not there were some one-offs, or temporary benefits, or non-structural factors that helped… The answer is “no”. This was structural and broad-based strength. Salmon didn’t hit the menu until Q2. The white sweet potato promotion they ran during the quarter is similar to what they always do. Nothing ephemeral propped this up. This is the same thorough, data-driven, process-obsessed team formula that has worked since long before their IPO.

More on the Menu:

The popular sweet potato limited time offer (LTO) was one of many pieces helping the strong Q1 demand. It drove higher frequency among loyal eaters and a noticeable uptick in new customer adoption as well. While many other companies flood their customer bases with a steady diet of LTO's, Cava is sticking to the long-term plan. It’s refraining from participating in this same approach to avoid diluting the special feel of each event. That’s partially why all of their LTO’s seem to do so well (there are fewer of them). Another reason for that is their careful stage-gate approach to food testing. Like everything else, they do not launch anything to the broader public until they have the obvious data to support the decision.

Looking ahead, their new salmon protein option was recently introduced to the full store base, with attach rates in line with company expectations. It sounds like they’re overall pleased here, as they talked about keeping it on the menu until at least Q4 compared to Q3 previously. It sounds like this could become a permanent option if things keep trending positively.

They have a stable flow of new food and drink items in the pipeline, with a garlic shrimp concept currently testing in a couple markets.

New Stores & Geographic Expansion:

Cava entered Cincinnati, St. Louis and Columbus during the quarter and will soon make its Minneapolis debut as well.

Leadership remains highly encouraged by the early performance of these 2026 stores. They're doing as well or, in some cases, even better than the strong 2025 vintage, with new restaurant productivity already over 100%, way ahead of schedule. All in all, revenue and profit contributions from these stores "continue to exceed expectations” and reach $3M in AUV several quarters before Cava used to think they could. And again, strength is nationwide and with zero geographic weak spots. They “have not found a market that doesn’t love Cava.”

Perhaps even more encouragingly, their 2024 and 2025 openings continue to exceed expectations after their first years in operation. These locations keep positively contributing to overall CSS growth, showing the concept's appeal can be highly sustainable.

In recent quarters, we've spoken about a "honeymoon effect," where their new stores perform so much better than they're supposed to, that it creates a CSS growth headwind for these stores in year two. That's not holding back results anymore, and that's a testament to robust multi-year success.

Personal Guest Relationships at Scale & Operational Excellence:

The revamped loyalty program is performing quite well alongside effective marketing campaigns with college hoops stars like the University of Michigan's Yaxel Lendeborg (Go Blue).

Taking a step back for a moment, Cava spent years vertically integrating its tech stack and re-forming it into malleable “micro-services” that can be easily and rapidly updated separately, while working perfectly together. This foundation is how it can build such a great loyalty program on its own while most others use 3rd-party services. It’s how their batting average of food introductions is so notably high and how they ensure store and service quality are equally high (and quickly fixed if not).

It’s also how they can build (in partnership with ResultStack) a new operating platform (called Cava Core) as a “unified foundation for how we manage and use data.” This should make them more thoughtful and surgical in inventory management, marketing localization, throughput optimization and every other important variable determining the company’s future. For many competitors, I’d tell them to let some other vendor build this for you instead of trying to do so much of it on your own. But Cava is different and, again, I think the highly-rated app firmly supports that notion.

Cava Core paves the way for its new “real-time commerce platform” called Cava Current. This should make its product display and promotional placements a lot more effective by making them significantly more targeted. Going back to Yaxel Lendeborg for a moment, he is beloved by many in Southeast Michigan. Knowing this, Cava could use the data and commerce platform to geofence Yaxel promotions in towns close to the University of Michigan like Canton and Novi. Simply put, this will allow them to move faster and in ways more relevant and impactful for their own business.

Pursuit of Great Talent:

- The “early indicators” for its new assistant general manager (AGM) role were called “promising.” As a reminder, this program is meant to create a larger and more consistent base of “role-ready leaders.” Stores with AGMs are outperforming stores without them.

- Priorities under new-ish COO Doug Thompson will include building their base of talent, improving store opening processes and bolstering Cava’s already strong hospitality.

- They continue to test their catering program in Houston and think there’s a lot of unmet demand. They just want to ensure they roll this out in a way that doesn’t sacrifice service quality for other ordering channels. It’s a highly intentional process just like everything else Cava does.