A lot of this week's content has already been sent. A review of SoFi CEO Anthony Noto's Interview with JP Morgan can be found here. Nvidia and Cava earnings reviews can be found here.

Next week, earnings coverage will include Zscaler, Salesforce, Marvell, Snowflake and MongoDB.

Other reviews from this season to read:

- Nu

- Mercado Libre & Datadog

- AMD & Uber

- Axon

- SoFi

- Amazon

- On Holding

- AppLovin & Cloudflare

- Duolingo

- Meta

- Starbucks

- Lemonade

- Robinhood

- Hims & The Trade Desk

- Alphabet

- Sea Limited

- Shopify & Coupang

- ServiceNow

- Apple

- Spotify

- Palantir

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

Table of Contents

1. More Software Coverage

Intuit and Workday are not two names in the normal coverage network. But these aren’t normal times. I’ve included them because periods of sector-wide indiscriminate selling make collecting as much real information amid the incessant noise even more important. So, while these are not two names I have any plans to own or cover in more detail on a consistent basis, I think right now it’s necessary.

a. Workday (WDAY)

Results:

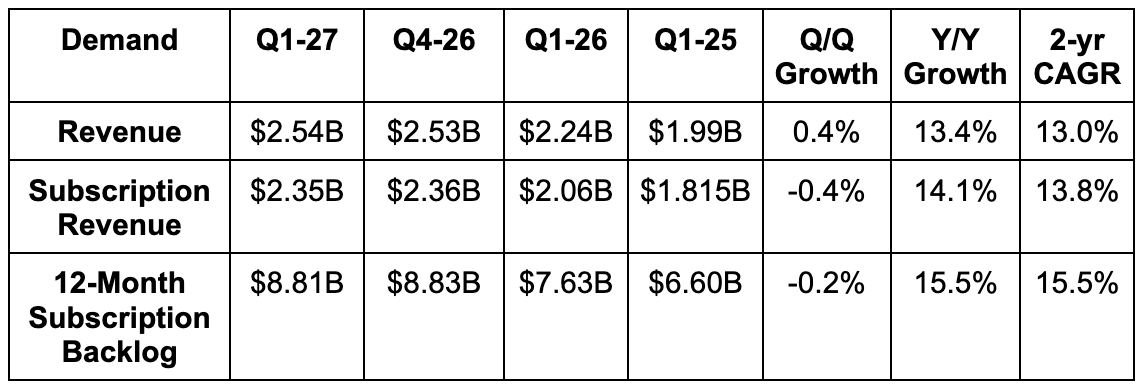

- Beat revenue estimate by 1%.

- Slightly beat subscription revenue estimate & beat guidance by 0.6%.

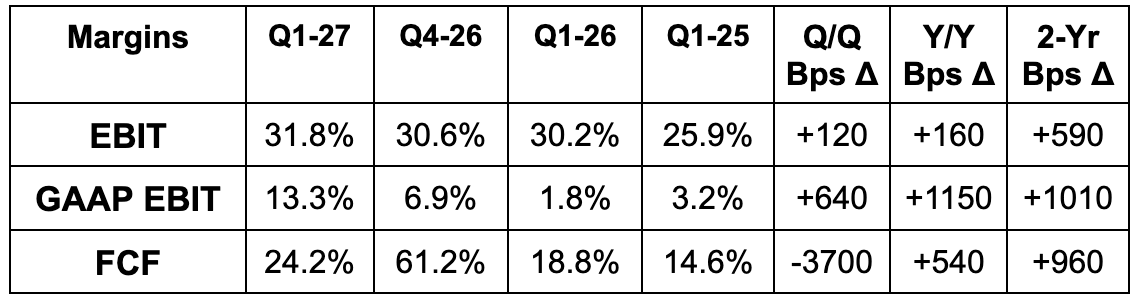

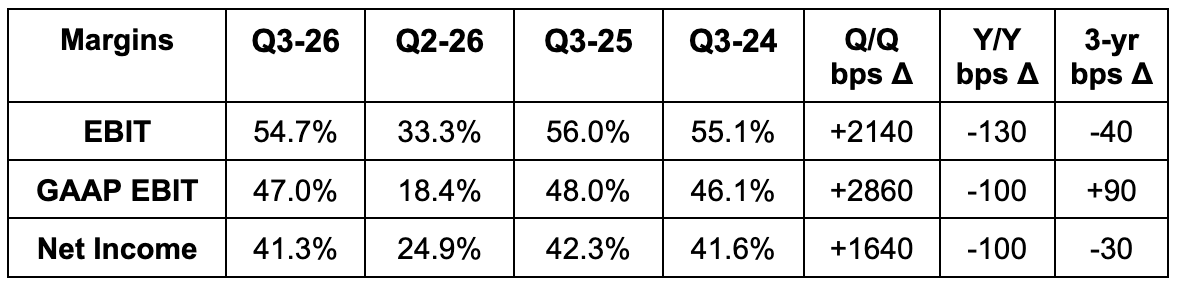

- Beat EBIT estimate by 5.2% & beat 30.5% EBIT margin guidance.

- Beat FCF estimate by 23%; beat $2.52 EPS estimate by $0.14.

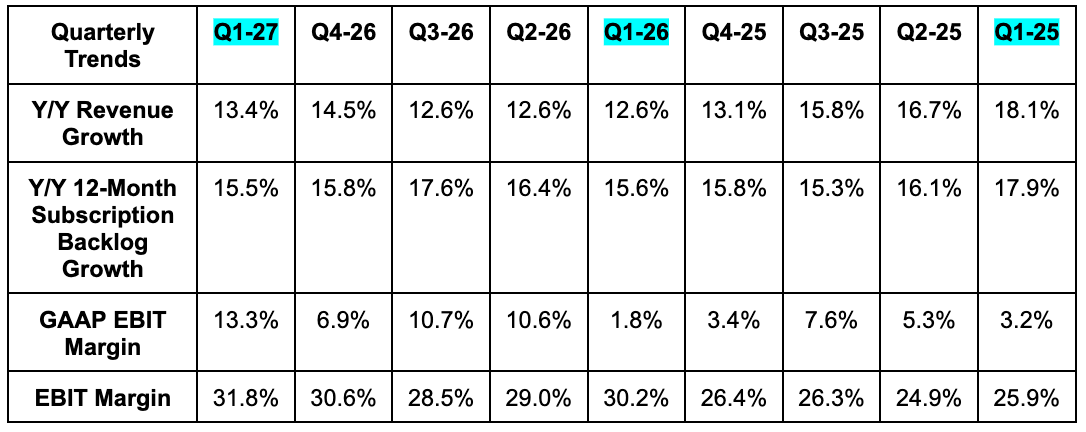

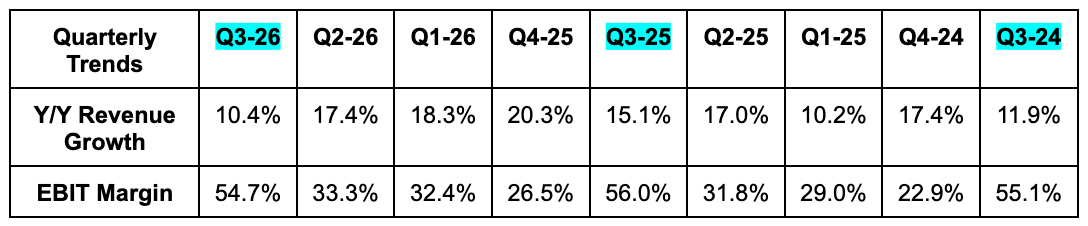

This marks WDAY’s best Q1 for net new Annual Contract Value (ACV) in 5 years. They think this quarter “signals an inflection point following a slower FY 2026.” Momentum spans the globe as well, with EMEA ACV up 50% Y/Y for Q1.

Balance Sheet:

- $4.3B in cash & equivalents.

- $3B total debt.

- Diluted share count shrank by 6% Y/Y.

Annual Guidance & Valuation:

- Reiterated subscription revenue guidance which roughly met estimates.

- Raised 30% EBIT margin guidance to 30.5%, beating 30.2% margin estimates. The improvement in margin guidance was credited to cost optimization.

Investor Material Notes:

Returning co-founder and CEO Aneel Bhursi is pushing very hard to accelerate product innovation and fortify Workday’s positioning in the age of AI. That’s his primary goal, with another important and related focus on more existing customer cross-selling. The two concepts go hand-in-hand.

Largely thanks to their Sana acquisition, which provides an AI-powered front door and a slew of agents, WDAY now features 20 agents with customers doubling Q/Q to 4,000+. This is also the technological backbone for WDAY’s enterprise search and agentic learning tools, as well as a software deployment agent that vastly speeds up the creation cycle. They hope to leverage this capability for “$0 software deployment” for their customers down the road. They acquired Sana for reasons similar to why ServiceNow bought Moveworks – a re-vamped and agentic-focused way for users (human and machine) to leverage its platform.

For more on AI demand, their annual contract value (ACV) from AI tools rose 200% Y/Y and is now closing in on $500M. 25% of total ACV landed during the quarter was from AI, and new consumption-based model offerings should align better with evolving customer interests to keep this moving in the right direction. That’s about 5% of total vs. about 9% for others like ServiceNow. I will say that human resources is among the most polarizing software pieces in terms of gauging AI displacement risk. If we no longer need as many people, that will inherently limit demand for WDAY’s existing offering and makes it absolutely imperative to successfully execute an agentic transition.

In terms of an AI moat, their arguments sound a lot like other scaled software platforms. They expect to unleash their decades of data, governance, guardrails and edge case know-how to augment and cultivate value from agents, rather than being supplanted by them. Broken record alert: agents boast unbelievably amazing potential. But that probabilistic potential must be guided and directed by deterministic help. WDAY’s dominant market presence and evolving product suite make them a great candidate to provide that help.

Quick Thoughts:

The company seems to be on better footing following the leadership transition and is starting to enjoy real progress with AI-based monetization. While it wasn’t a blowout quarter, it’s great to see stable Y/Y backlog growth and great to see that investments to beef up the product suite aren’t stopping them from boosting EBIT margin guidance. This was an overall positive datapoint for software reliance. Not a blowout quarter. But solid.

b. Intuit (INTU)

Results:

- Slightly beat revenue estimate & slightly beat guidance.

- Within the consumer group, Turbotax revenue rose 7% Y/Y from $4.1B to $4.4B and Credit Karma revenue rose 15% Y/Y to $631M.

- Consumer revenue is very lumpy around tax season.

- Beat EBIT estimate by 0.9%.

- Beat $12.57 EPS estimate by $0.23 & beat guidance by $0.32.

- Beat $10.59 GAAP EPS estimate by $0.33 & beat guidance by $0.50.

Balance Sheet:

- $6.8B cash & equivalents.

- $6.2B debt

- Share count fell by 2.1% Y/Y.

- Dividends grew by 14% Y/Y.

Guidance & Valuation:

- Raised revenue growth guidance from 12.5% to 13.5%, beating 12.8% growth estimate.

- Raised EBIT guidance by 1.8%, beating estimate by 1.4%.

- Raised EPS growth guidance from 14.5% to 18%, beating 15.3% growth estimate.

- Raised GAAP EPS growth guidance from 14% to 16%, beating 15.7% growth estimate.

- They also announced a 17% layoff in efforts to become a faster moving and more focused company. This will lead to restructuring charges mainly next quarter, which will weigh a bit on GAAP margins.

Investor Material Notes:

For segment guidance, INTU raised global business solution growth from 14.5% to 16% for the year. It also raised consumer segment growth guidance from 8.5% to 10%. At the same time, this was powered by a large Credit Karma raise. TurboTax growth guidance was cut from 8% Y/Y to 7% Y/Y, which was the main source of investor disappointment. There’s growing evidence that TurboTax is losing market share in the lower-income cohorts because they’re not competing effectively enough on price. Mailchimp is going through some churn issues tied to rightsizing growth investments in that business to prioritize cash flow generation. But that was expected. Again, TurboTax is really the issue. Every other important piece of the business, including their TurboTax Live products that offer more hands-on help, is rapidly growing and Intuit has a mountain of data to train agents more effectively than others can.

Markets right now are seeking out any sign of forward-looking weakness offering credibility to the idea that AI is actually having a materially negative impact. TurboTax is a highly important segment for them, so while the team will blame pricing strategy on the weakness, investors in this environment will automatically assume it means the company is at risk due to alternate AI options.

Quick Thoughts:

I talked to a former Executive Vice President and the GM of their Small and Medium Business segment about the quarter this week. I don’t know this company very well so I was glad to get a sense of the landscape. That person left the company on their own, so shouldn’t have much negative bias against it. In their mind, these issues are self-inflicted and not because of AI. They just don’t think this company is executing or innovating quickly enough to keep up.

While I respect that opinion, and while this isn’t where I’m looking to find software exposure right now, it does feel like this week’s reaction was a tad extreme. This trades for just over 10x FCF compared to 30x just two years ago. It’s not like low-double digit compounding at this scale is bad by any means. I do not see this modest beat-and-raise report as a yellow or red flag for the sector overall. It’s a subtle positive if anything, considering most of the enterprise-facing businesses are performing well. I see Intuit as a company dealing with some internal segment-level issues and showing signs of being completely healthy everywhere else.

c. More on Software

While earnings reports across the enterprise software sector have been relatively healthy throughout the season, there are some patterns emerging that I'd like to discuss. Over the last year, we've all heard disaster forecasts about the impact that AI's proliferation can have on seat-based licensing business models. If hiring slows down, then per-person licensing demand naturally slows down with it. Furthermore, many of these companies have not oriented their valuable backend context in ways that are easily accessible for agents to participate in that value creation opportunity either. ServiceNow and Salesforce certainly have, with their headless pivots, and I expect many more to follow suit over time. But I'm candidly surprised that the sense of urgency and pace of evolution has not been even faster. These companies should consider that change vital to preserving durable growth tailwinds in the years to come. Turning agentic traffic into large businesses is the only way to far more than offset any seat-based pressures.

And I think we are seeing a divergence in earnings data this season, split somewhat neatly into these two buckets. Consumption-based business models like Datadog, Palantir and even Twilio have shown strong signs of accelerating, while seat-based companies like Workday, ServiceNow and others have posted largely in-line results. Not bad. But not the kind of tangible acceleration and upside we’re seeing from the other cohort. There have been exceptions like Atlassian, but not that many.

Seat-based companies are rapidly shifting to consumption-based, but there’s some cannibalization taking place that could hold back growth for a few more quarters. The companies that successfully pivot should then see meaningful accelerations, and I think investors will need to be more patient to see them than on the consumption side of things.

We're also seeing divergence across app layer software companies and infrastructure layer software companies. But I believe these two pieces of the overall sector are converging. Companies like ServiceNow are positioning their apps as repositories of data, coaching, and experience that agents can learn from, to move from probabilistic guessing to deterministic reliability at enterprise scale. These apps are being unlocked to leverage the sustainably valuable part of them, rather than relying on a slick interface that can be easily copied to drive differentiation. This is why I think app layer platforms that have the most of this data will weather the AI storm and be fine, while smaller point solutions with smaller economies of scale will struggle.