Okta, UiPath, and SentinelOne are not part of the core coverage network. Still, with software sentiment so volatile and the future of this sector so polarizing right now, I think it's important to collect as much earnings data as we can. Salesforce is part of the core coverage network, and I will get a detailed review for that report published soon. For now, here are brief snapshots of that report and the other three.

Other detailed earnings reviews to read from this season include:

- MongoDB

- Zscaler

- Snowflake

- Nu

- Mercado Libre & Datadog

- AMD & Uber

- Axon

- SoFi

- Amazon

- On Holding

- AppLovin & Cloudflare

- Duolingo

- Meta

- Starbucks

- Lemonade

- Robinhood

- Hims & The Trade Desk

- Alphabet

- Sea Limited

- Shopify & Coupang

- ServiceNow

- Apple

- Spotify

- Palantir

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

a. Salesforce (CRM)

The detailed earnings review was published and can be found here.

Results:

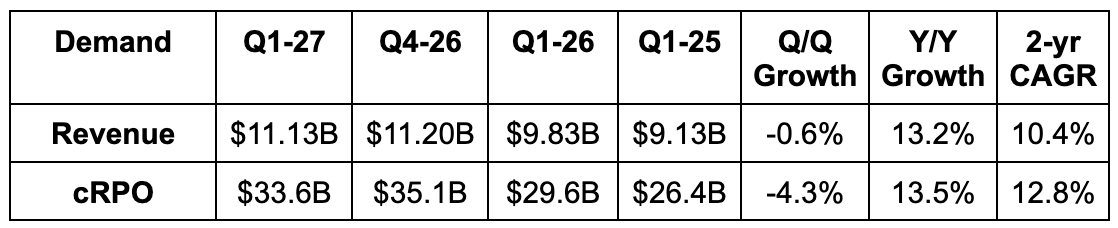

- Beat revenue estimates by 0.7% & beat guidance by 0.6%.

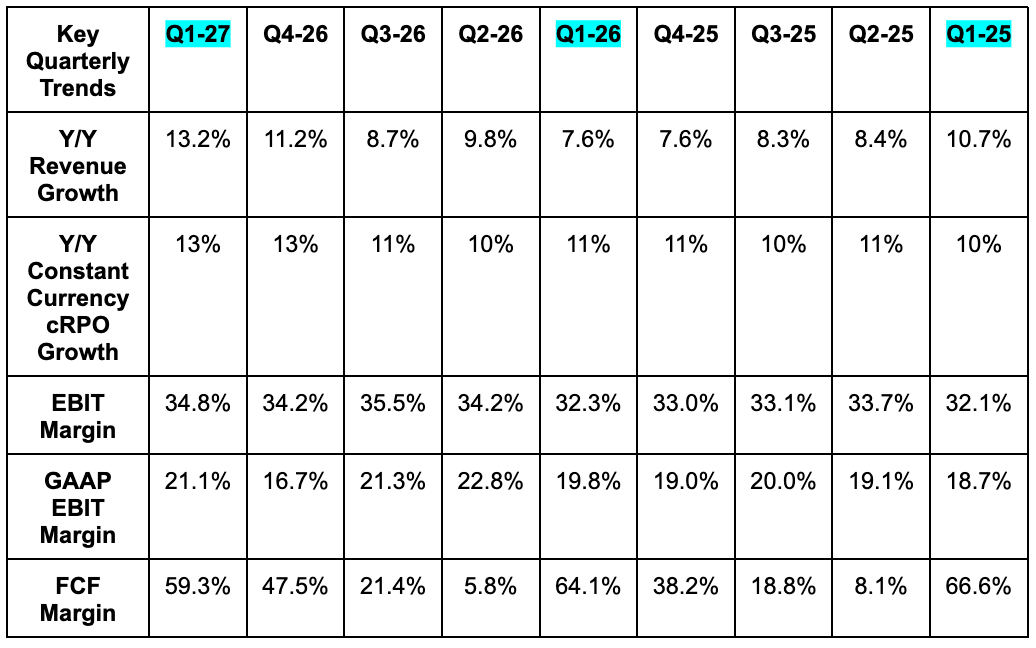

- 12% constant currency (CC) growth beat 10.5% CC growth guidance. 8.9% organic revenue growth beat 8.5% organic growth guidance.

- Beat subscription & support revenue estimates by 0.7%.

- Slightly missed current remaining performance obligation (cRPO) estimates. Met 13% constant currency (CC) cRPO growth guidance.

- Missed RPO estimates by 1.5%.

Balance Sheet:

- $11.8B cash & equivalents.

- $39.3B debt vs. $10.4B Y/Y.

- Diluted share count shrank by 10% Y/Y. With the help of debt issuance, they bought back $27B in stock in a single quarter. For context, the market cap is currently $144B. Massive.

Guidance & Valuation:

- Slightly raised annual revenue guidance, which slightly missed estimates.

- Reiterated annual 10.5% CC growth guidance.

- Raised annual 7.5% organic growth guidance to 8.0%.

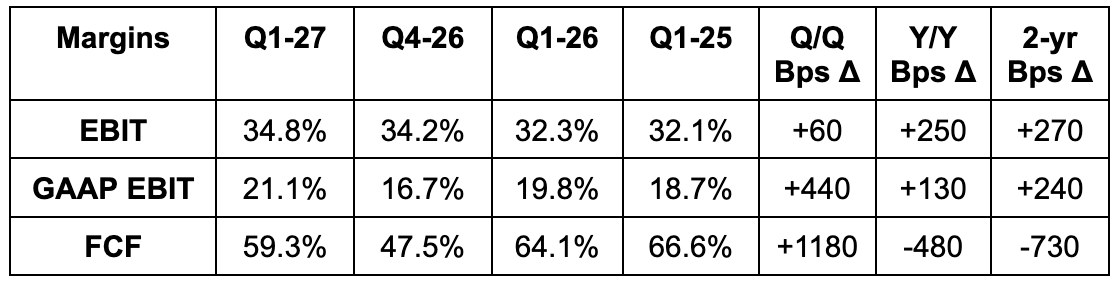

- Slightly raised annual EBIT guidance, which slightly missed estimates. EBIT margin guidance was reiterated, with the small boost to EBIT dollar guidance coming from the revenue beat.

- Lowered 9.5% FCF growth guidance to 4.5% FCF growth.

- Raised annual $7.89 GAAP EPS guidance by $0.06.

- Raised annual $13.15 EPS guidance by $0.94, which beat by $0.87.

- For Q2, revenue guidance was a tad light, CC cRPO growth guidance was in-line and EPS guidance was slightly ahead.

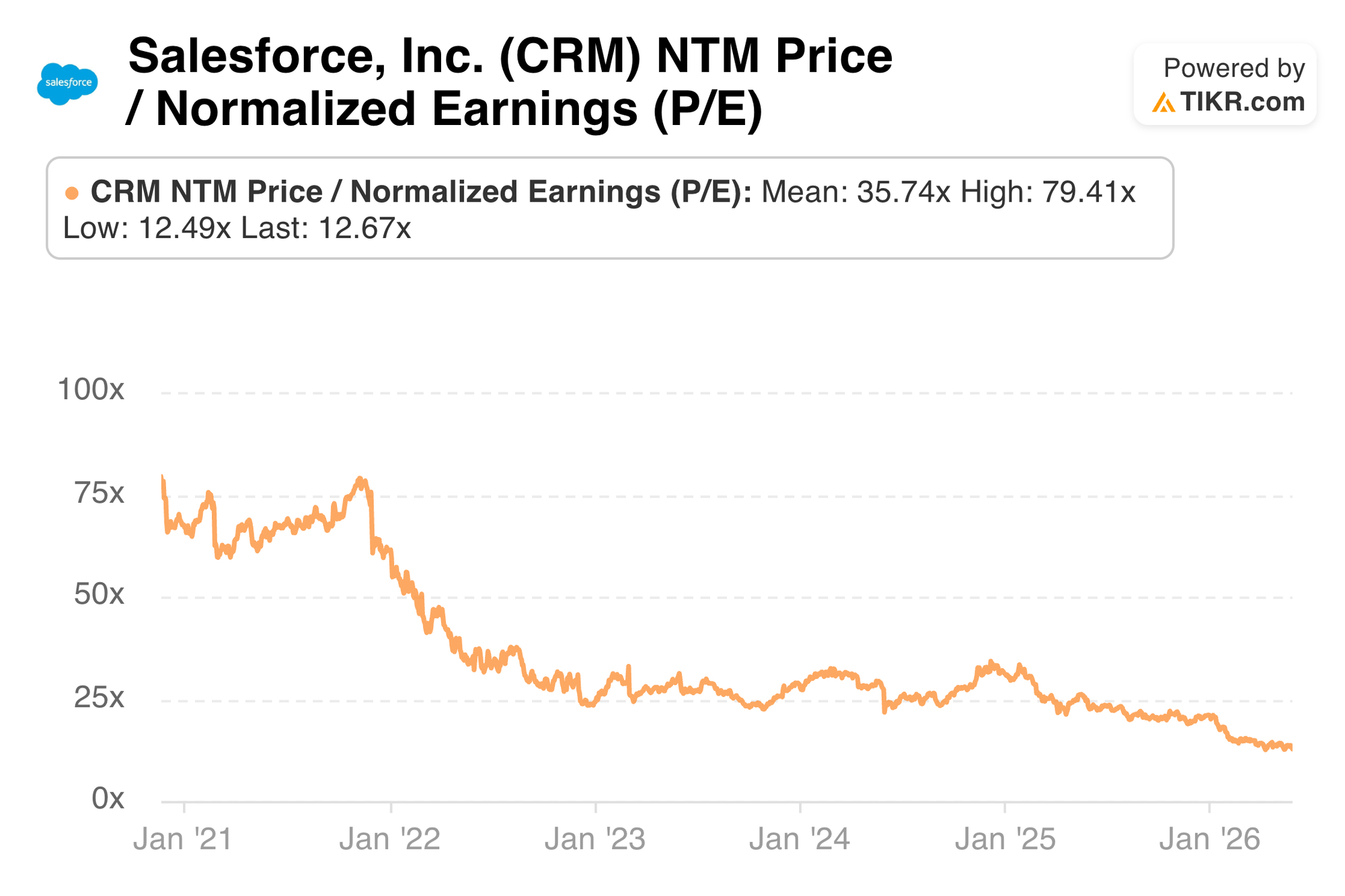

Salesforce trades for 10x forward FCF and 13x forward EPS. FCF is expected to grow by 4% this year and by 10% next year. EPS is expected to grow by 13% this year and by 9% next year.

b. Okta (OKTA)

Results:

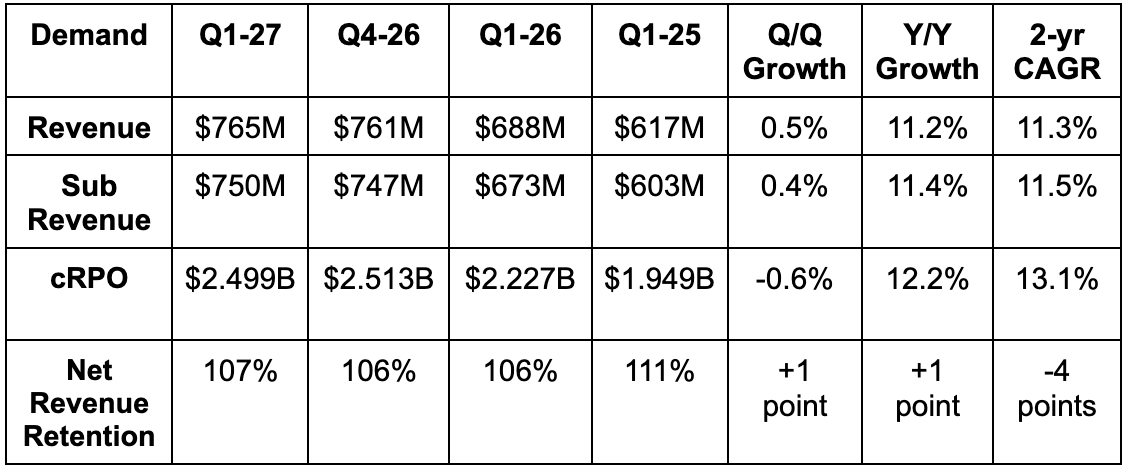

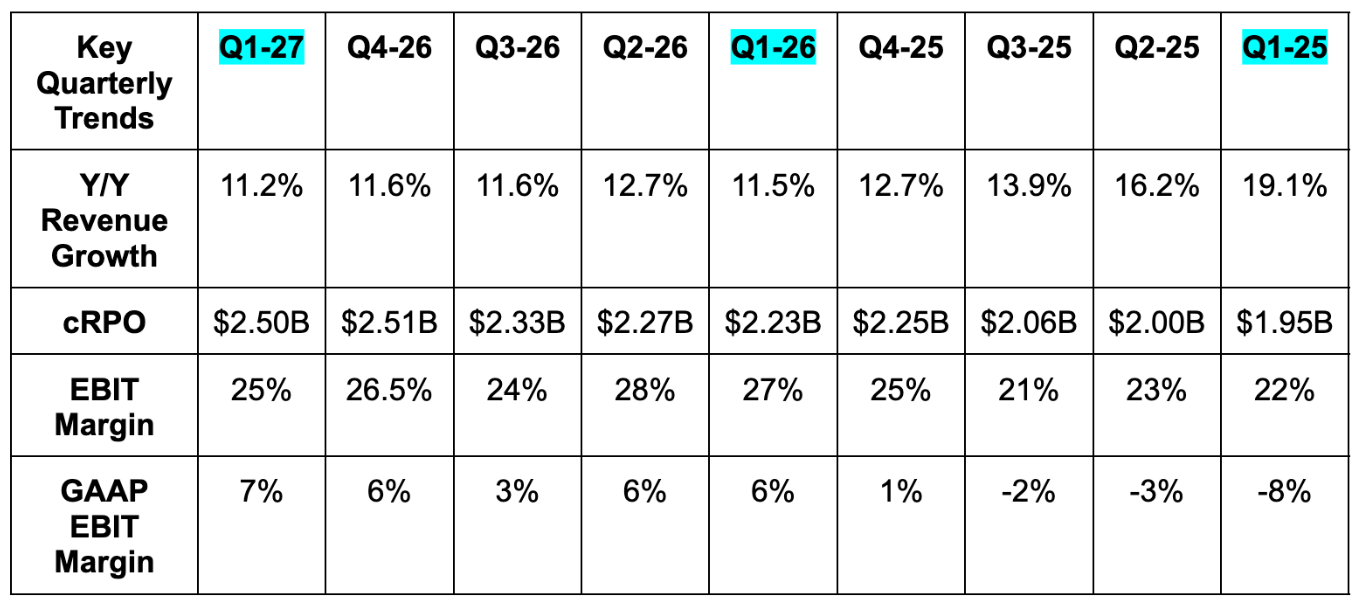

- Okta beat revenue estimates by 1.7% & beat guidance by 1.9%.

- Current Remaining Performance Obligations (cRPO) beat guidance by $54M or 2.2%.

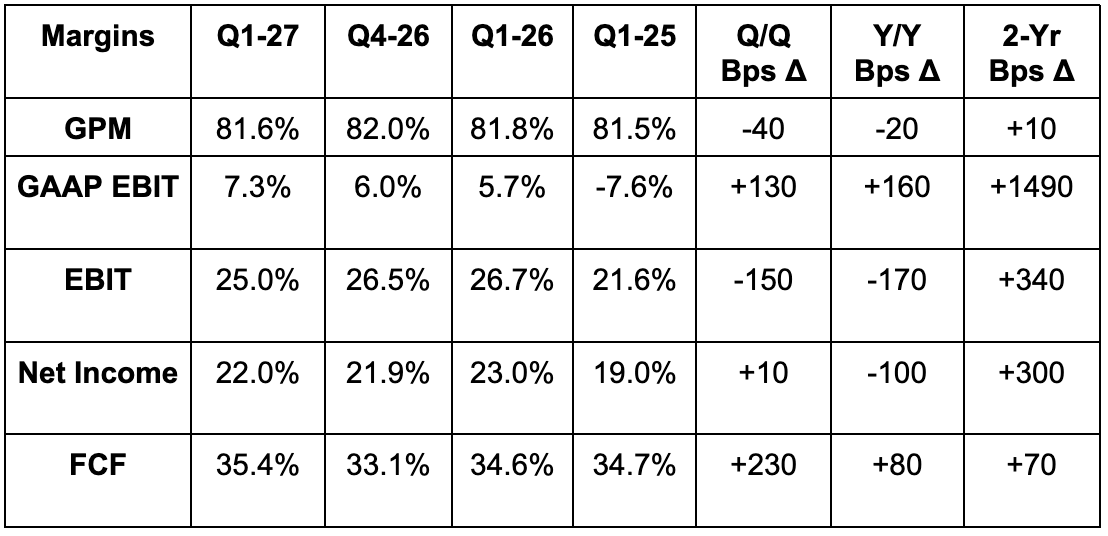

- Met 81.6% GPM estimate.

- Beat EBIT estimates by 6.4% & beat guidance by 7.3%.

- Beat $0.85 EPS estimates & identical guidance by $0.06 each.

- Beat FCF estimates & identical guidance by 6.3% each.

Balance Sheet:

- $2.6B in cash & equivalents.

- $350M in convertible senior notes.

- No traditional debt.

- Diluted share count rose by 0.5%.

Guidance & Valuation:

- Raised annual revenue guidance by 0.5%, which slightly beat estimates.

- Raised annual EBIT guidance by 1.4%, which beat estimates by 1%.

- Raised annual $3.78 EPS guidance by $0.05, which beat estimates by $0.04.

- Raised annual FCF estimate by 0.6%, which slightly missed estimates.

- Next quarter guidance was slightly ahead for revenue and EBIT. It was 2.6% ahead for FCF and in line for EPS.

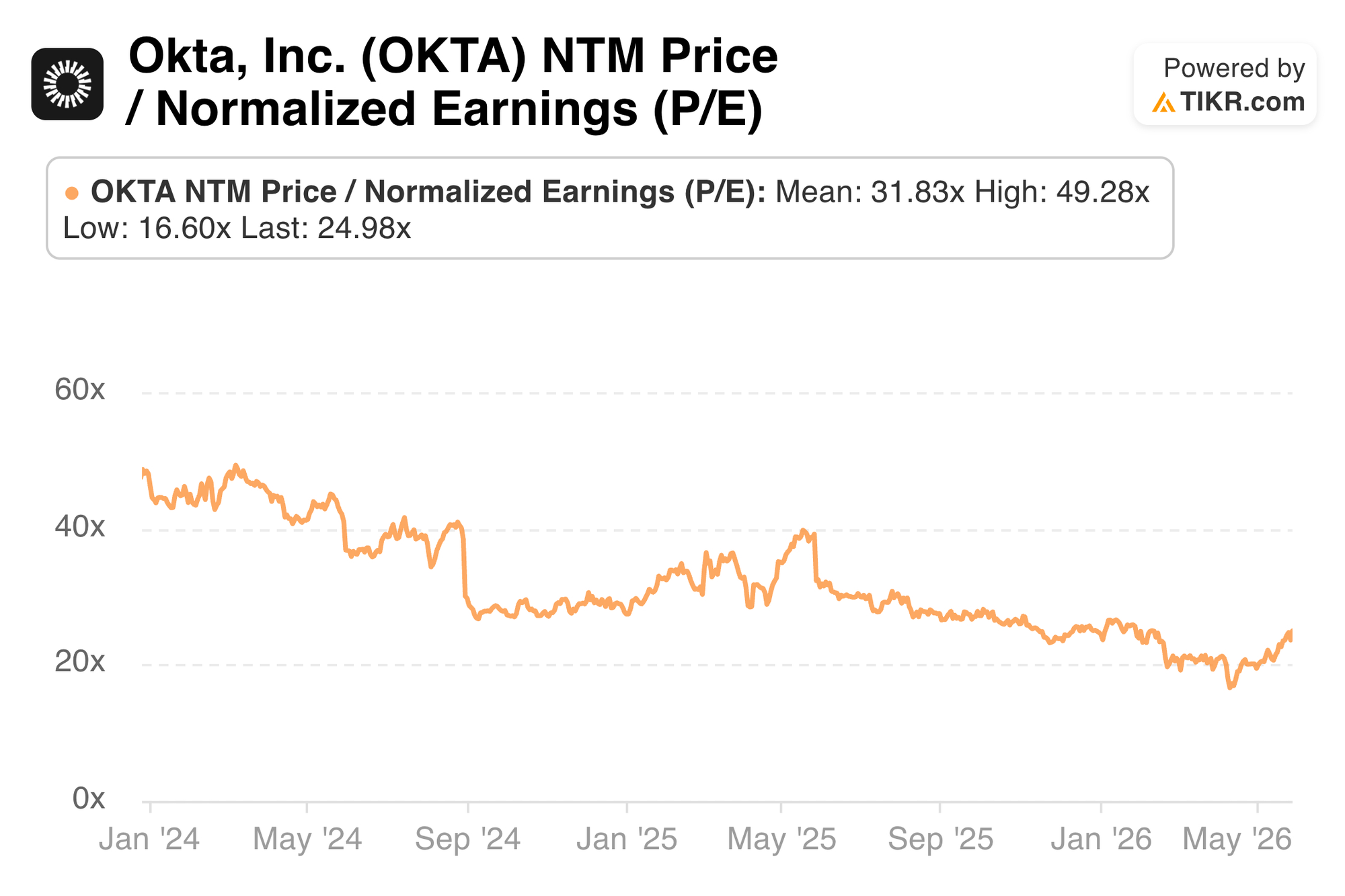

Okta trades for 25x forward EPS and 18x forward FCF. EPS is expected to grow by 8.5% this year and by 11.8% next year. FCF is expected to grow by 1.2% this year and by 14.1% next year.

c. SentinelOne

Results:

- Met ARR estimates.

- Slightly missed revenue estimate & slightly missed guidance.

- Beat $5.3M EBIT estimate by $5.2M & beat guidance by $5.5M.

- Beat $0.02 EPS estimate by $0.02 & beat guidance by $0.025.

Balance Sheet:

- $650M in cash & equivalents.

- $155M long-term investments.

- No debt.

- 0.8% Y/Y diluted share count growth.

Guidance & Valuation:

- Reiterated annual revenue guidance, which slightly missed estimates.

- Raised annual EBIT guidance by 4.3%, which beat estimates by 4.1%.

- Raised $0.34 EPS guidance by a penny, which met estimates.

- Q2 revenue guidance missed estimates by 0.7% and Q2 profit guidance met expectations.

SentinelOne trades for 53x forward FCF & EPS. FCF is expected to grow by 122% this year and by 66% next year. EPS is expected to grow by 69% this year and by 41% next year. It’s very cheap. But that’s because of ongoing growth deceleration concerns that merely grew larger from this report.

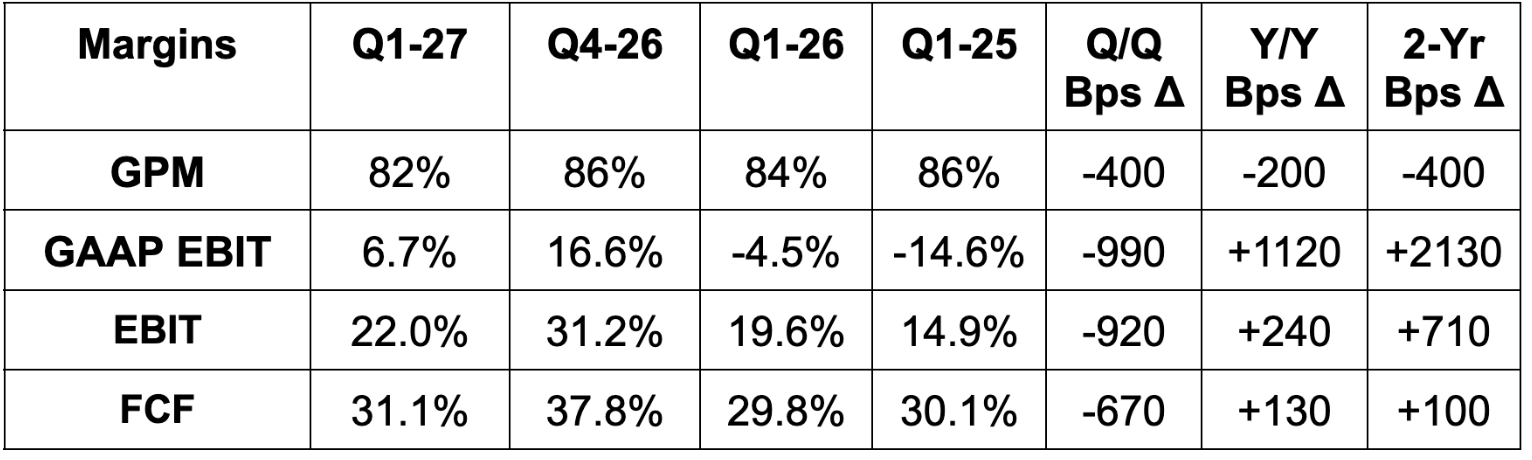

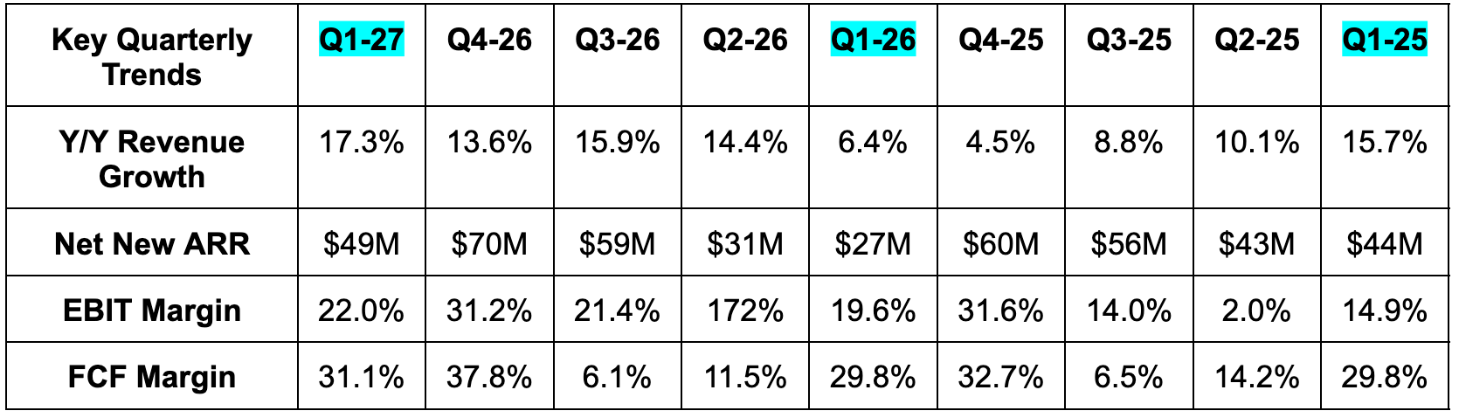

d. UiPath

Results:

- Revenue beat estimate by 5.3% & beat guidance by 5.3%.

- Beat $43.5M net new ARR estimate by $5.5M.

- Beat EBIT estimate by 15.7% & beat guidance by 15.7%.

- Beat $0.03 GAAP EPS estimate by $0.01.

Balance Sheet:

- $1.3B cash & equivalents.

- $108M non-current marketable securities.

- No debt.

- Share count shrank by 3.8% Y/Y.

Guidance & Valuation:

- Slightly raised annual revenue guidance, which slightly beat estimates.

- Raised annual net new ARR guidance by $70M. Slightly raised annual ARR guidance, which slightly beat estimates.

- Raised annual EBIT guidance by 3.6%, which beat estimates by 3.5%.

- Q2 revenue and EBIT guidance were both slightly ahead of estimates.

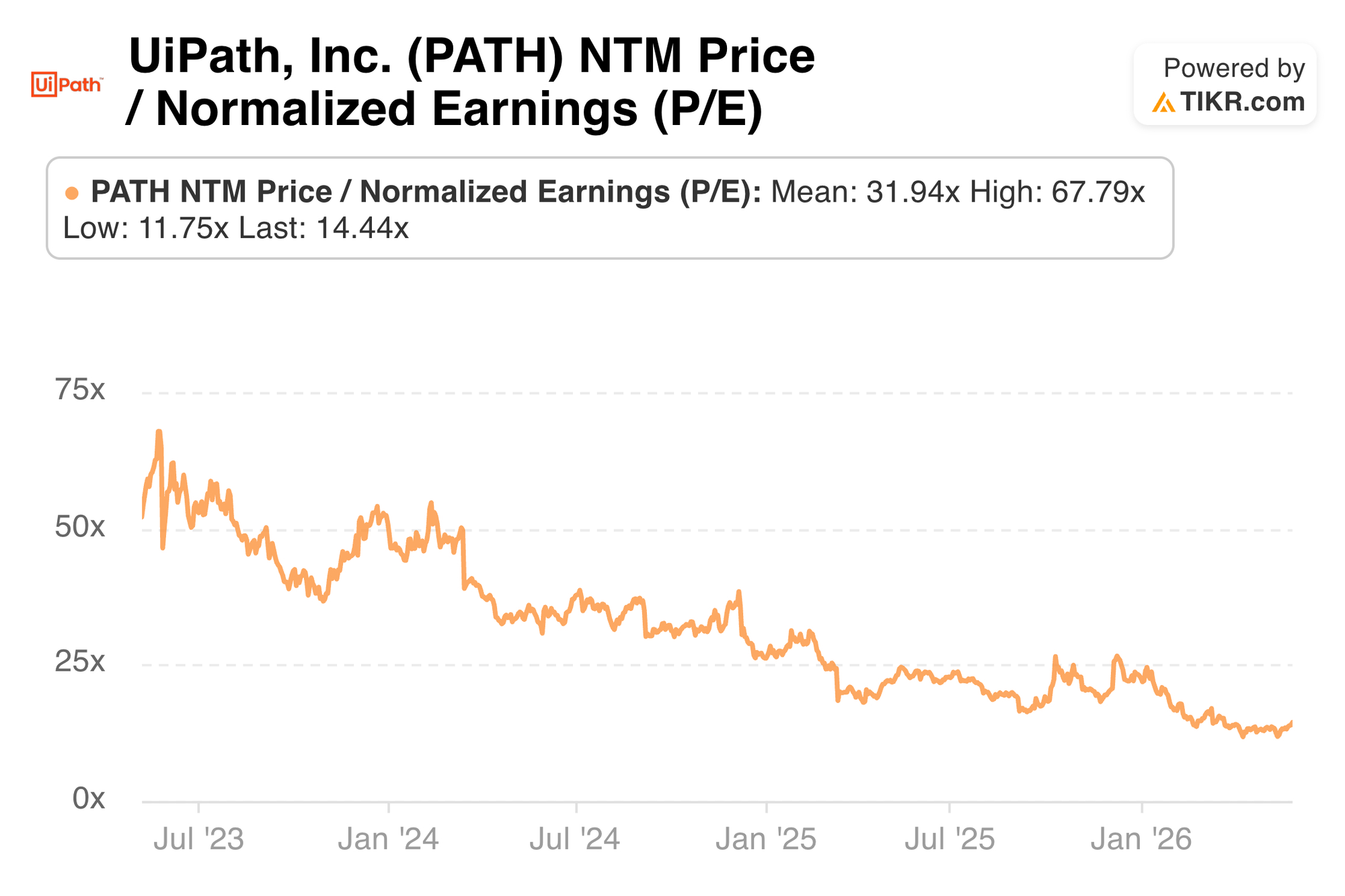

PATH trades for 14x forward EPS and FCF. EPS is expected to grow by 11% this year and by 12% next year. FCF is expected to grow by 21% this year and by 14% next year.

e. Quick Thoughts

The general theme of consumption-based software models (especially in data) thriving and seat-based business models performing about as expected continues. MongoDB results (review already sent) looked great on the consumption side, while all of these reports look roughly as expected. I will say SentinelOne continues to disappoint and I think that has more to do with leadership and go-to-market than anything else. Their products are good enough to be doing a lot better than they are. Salesforce had a decent quarter. The buyback is arguably the most exciting thing about the investment, but if they can deliver a bottoming in overall growth rates at their dirt cheap multiple, there could be a lot to like. I'd like to see more evidence of this growth engine outside of M&A not being in permanent decline. I think this earnings season has made it clear to me that I want almost all of my software exposure to come from the data infrastructure side of the sector.